French economy shrank nearly a fifth in the first half of 2020

- 31 July 2020

- France

Today’s figures show that there was a heavy price to pay for the severe lockdown imposed on the French economy, which contracted more than its US and German counterparts in 2Q20. On a positive note, the figures also suggest that the French economy made a speedy comeback in the course of 2Q20, from 65% of its normal activity level to nearly 90%

| -19% |

French economic contraction in the first half of the year |

A more severe lockdown led to a more severe recession...

French GDP data showed the severe impact of the lockdown on the French economy. With a (revised downwards) contraction of 5.7% in 1Q20 and a 13.8% in 2Q20, GDP contracted by almost one fifth (19%) in the first half of the year. This result is much worse than the just-released figures of the US (-11% in 1H20) and Germany (-12% in 1H20) where lockdowns were less severe.

All components contributed to the historic drop in the second quarter but the net export contribution is particularly negative (-2.3pp) with exports dropping by 25.5% on the back of nearly paralysed intra-eurozone trade. Corporate investment resisted the lockdown better than other investment components: they were down by 16% quarter-on-quarter after 10.6% in 1Q20, while household investment fell by 20%, as most building sites had to stop. Household consumption was the most negative contributor to growth, with a drop of 11% QoQ in 2Q20.

...but the catch-up was speedy at the end of 2Q20

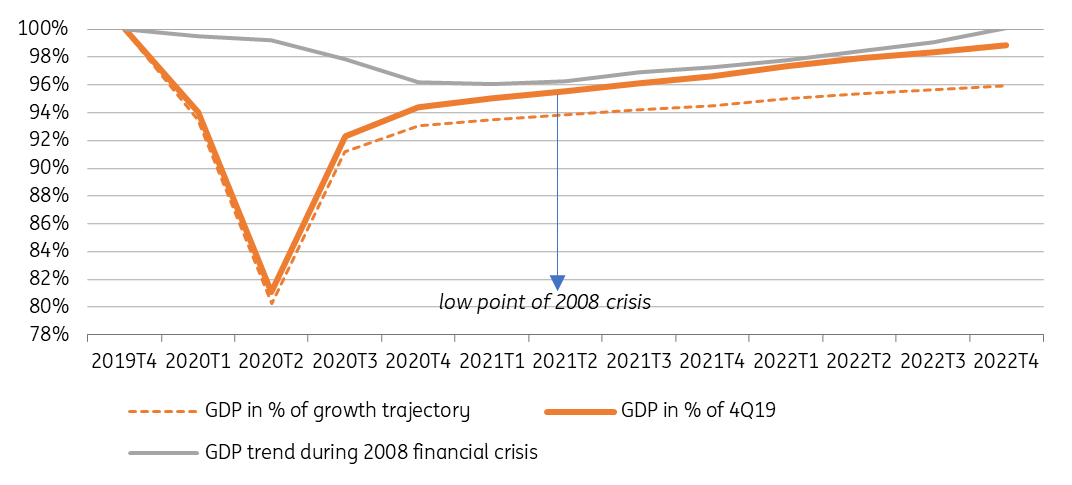

All in all, today’s figures suggest that the French economy was running at 80% of capacity on average during 2Q20, coming from a low point of 65% during the lockdown period. As the first four weeks of the quarter were still affected by severe lockdown measures, it means that the French economy has rebounded more than expected in June and is probably closer to 90% in July. If these levels are maintained, a V-shaped recovery is on the cards for the third quarter. However, regaining the last 10% will probably be more difficult after the summer, especially if social distancing remains the norm and local lockdowns necessary. It will take years to recoup the lost GDP. The recently announced €100 billion recovery plan (partly financed through the EU Next Generation recovery plan) should give a push to GDP in the next two years. This is why we stick to our a current scenario of a 9.5% GDP contraction in 2020 followed by a strong 6% rebound in 2021.

A V is not enough

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more