France: Business climate edges up but short-term outlook looks grim

The business climate in France improved slightly in January thanks to a good performance in industry and wholesale trade. Services and retail trade continue to suffer from the current health restrictions. The outlook for the first quarter is more uncertain than ever

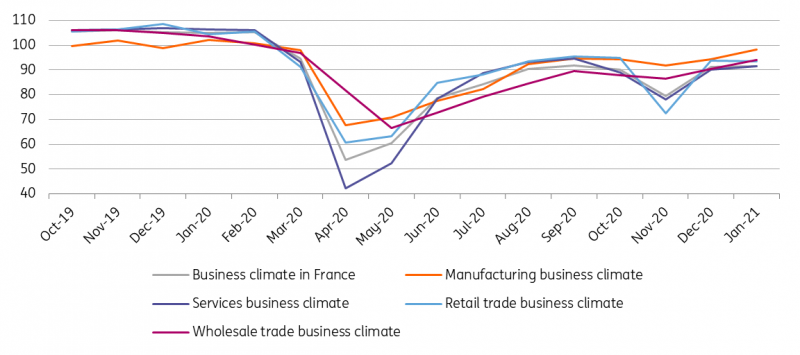

Industry and wholesale trade drive business climate up

The business climate indicator in France improved slightly in January compared to December, with the index rising from 91 to 92. This slight increase is due to an improvement of the business climate in industry (the index having risen from 94 to 98 in one month) and in wholesale trade (from 86 to 94 in two months). In both sectors, the business climate reached its highest level since March, a sign of an almost uninterrupted recovery of the economic situation since the April lockdown. The November lockdown, which mainly affected the service and retail sectors, had almost no impact on the steady improvement in business sentiment in industry and wholesale trade. However, the business climate indices for these two sectors are still below their long-term average and pre-crisis levels. In view of the restrictive measures currently in place in France (curfew, closure of bars, restaurants, cultural and sports venues and ski lifts), these sectors will probably continue to perform better than services and retail trade in the coming months. They therefore remain the driving forces behind the French economy at the present time.

It should be noted, moreover, that with specific regard to the industrial sector, the quarterly surveys reveal that the rate of production capacity utilisation, a good indicator of the imbalance between supply and demand, increased slightly between October and January to reach 79%. On this indicator too, the progression has been constant since the beginning of the pandemic and the November lockdown has not had a negative impact. Nevertheless, the situation has deteriorated compared to the pre-crisis level (83).

In the services sector and in retail trade, the business climate indices hardly fluctuated in January compared to December. This stagnation should be compared with the level of health restrictions affecting these two sectors, which remained stable in January compared with December, after the strong improvement in December caused by the end of the lockdown. For the coming months, given the health situation, we fear the business climate will not improve much in these sectors. It could even deteriorate significantly if new restrictions were to be introduced (such as a closure of non-essential shops or a closure of schools).

Finally, it should be noted that the employment climate improved very slightly in January, from 86 to 87, but remains far below its pre-crisis level (105).

Business climate in France

Outlook for the future

More than ever, the health situation continues to completely dominate the economic outlook. And in this context, the next two weeks will be crucial. The evolution of the pandemic is not reassuring and the new British variant is increasing pessimism. Across the country, hospital officials are beginning to publicly consider the possibility of a third lockdown to curb a situation that could be out of control by mid-February, similar to what happened in England and Ireland in December. If the government prefers to wait and see how the situation develops, it may be forced to take drastic decisions quickly. Therefore, we believe that a new lockdown in the first quarter, with a further closure of businesses considered non-essential, cannot be excluded. If it were to occur, it would imply that quarterly GDP growth would probably fall into negative territory in 1Q. Indeed, January may have a level of activity broadly similar to that of December. A further lockdown would likely cause economic activity to fall to the level observed in November. And it is unlikely that the level of activity that prevailed in October will be reached at some point during the quarter.

If a third lockdown can be avoided, health restrictions will nevertheless weigh heavily on economic activity in 1Q. While a very dynamic rebound in activity was observed after the first lockdown, such a rebound cannot be envisaged for the second lockdown. Indeed, the restrictions, including the closure of bars and restaurants, sports and cultural venues as well as the 6pm curfew, are weighing on household consumption and on the activity of certain sectors. With the non-reopening of ski lifts for the February holidays, the whole ski season seems compromised. Some sources close to the government also suggest that the closure of restaurants could be extended until the beginning of April, and that of bars and cafés until June. In the end, it seems that we can count on strong restrictions throughout the first quarter of 2021. Therefore, even without further lockdowns, quarterly growth in 1Q compared to 4Q 2020 will not be very dynamic, and could approach 0%.

In the current context, it seems that it will take until the second quarter for economic activity in France to really rebound. Once the vaccine is sufficiently deployed, restrictions are lifted, European tourism is allowed again and fears of further restrictions are dispelled, the economy should rebound strongly. We expect dynamic growth in the second half of 2021, as well as in 2022. In this context, the government's objective of 6% growth in 2021 seems difficult to achieve. Achieving growth of 4.5% over the year would already be a great success. The rest of the recovery will take place in 2022 and it will probably take half of 2023 to see economic activity return to its pre-crisis level.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article