Fed’s wait and see stance could persist through to September

Another hold from the Federal Reserve with an acknowledgement that uncertainty has increased with more upside risk for both inflation and unemployment. This suggests little inclination to move until they are confident of the direction the data is heading, meaning rate cuts could be delayed, but risk being sharper when they come

Fed leaves rates unchanged, but highlights elevated uncertainty

The Federal Reserve has left monetary policy unchanged with the Fed funds target rate range remaining at 4.25-4.50%. It was a unanimous decision with the accompanying press release stating that the economy continues to "expand at a solid pace", labour market conditions remain "solid" while inflation "remains somewhat elevated". All this phraseology is the same as last time.

The key modifications are that the Fed believes the "uncertainty about the economic outlook has increased further” and that the “risks of higher unemployment and higher inflation have risen". There is nothing particularly surprising in these comments with limited market reaction.

The 'wait and see' stance could continue for another couple of meetings

President Trump and Treasury Secretary Bessent will keep pressuring the Fed to cut interest rates, but those demands will continue to fall on deaf ears as officials try to gauge the inflationary impact from the Administration’s trade policies amidst ongoing labour market strength. Higher tariffs look set to lift prices while port operators and logistics firms are warning of a potential supply crunch that risks amplifying the near-term inflation threat. As such the Fed is in 'wait and see' mode, with Chair Jay Powell warning last month that “our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem”. This was repeated at today's press conference.

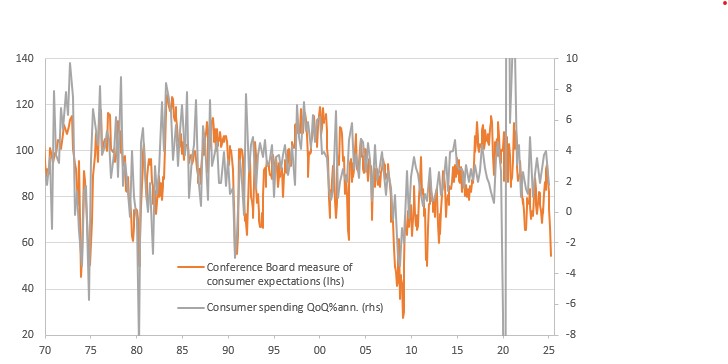

Consumer confidence readings point to the risk of a steep drop in spending

Fed cuts may come later, but end up being sharper

However, the scale of the slump in consumer and corporate sentiment to levels historically consistent with recession will be of concern to the Fed. Economic uncertainty and government spending curbs mean that trade deals and tax cuts need to be agreed quickly to prevent a stagflation infused downturn. Nonetheless, we expect that shelter-related disinflation, as already hinted at by the Cleveland Fed’s new tenant rent series, will give the Fed the room to respond with rate cuts later in the year. The market favours a July start point, but we see the risk for slippage and it may be that the Fed kicks things off with a 50bp cut in September, just as they did in 2024.

No material comment on the tapering process, and bonds trade both sides of the rate cut outlook

The main immediate impulse from the preliminary headlines was lower rates and a steeper curve, with most of the action coming in the real rates space. From that, there was a supposition that the Fed is primed to react to higher unemployment and hold its nose to rising price rise risks. That was quite the reaction, on some brief and in fact balanced snippets from the press release. That type of price reaction needed to be validated from the press conference. In fact the commentary at the press conference was not quite in sync with the early price action, and market rates edged back up again. Overall, the net outcome is slightly lower for market rates, and in our opinion there is an avenue for that to be extrapolated ahead on a theory that we see some macro pressures build. The 10yr yield can easily get down to the 4% area in such a scenario. But for now, the contemporaneous economy is just about firm enough to validate market rates staying about where they are for now.

Nothing new on the bond roll-off programme (quantitative tightening). Last time, the Fed lowered the cap on the roll-off of Treasuries to $5bn per month, which is effectively zero. In turn that means that the Fed continues to be a net buyer of Treasuries, as the roll-off ranges from $20bn to $60bn per month. No change to this policy. At the same time a $35bn cap remains on the MBS roll-off, but we’ve not been hitting that cap, which means that MBS bonds that mature do not get re-invested. Anything in excess of $35bn would be re-invested in Treasuries (which is in fact rare). Long term, the Fed would have an ambition to take the MBS bonds off its books completely, and ideally replace them with Treasuries. No (new) commentary on this today though. Clearly all this being left to another occasion, perhaps awaiting less impactful times. For now the slower tapering process continues, and can do so as bank reserves remain ample enough. One technical help here comes from the debt ceiling, as until this is raised or suspended, the US Treasury is spending down and in so doing, adding to bank reserves.

FX not focused on the Fed for the moment

The dollar is slightly offered after the FOMC announcement, but the FX impact has been quite contained on the whole. Short-term rate differentials have had very limited spillover into USD-crosses of late, and the dollar was probably hit more by the Fed's concerns for a rise in both unemployment and inflation rather than any hawkish/dovish takeaways today. After all, the run-in to this FOMC meeting had seen a nearly 20 hawkish repricing in the USD OIS curve, but an underwhelming dollar rebound.

The dollar continues to embed a sizeable risk premium relative to its usual market drivers (rates and equity differentials, global risk sentiment). In EUR/USD that translates into around 4% overvaluation in our estimates, but the path to make markets comfortable with a substantially smaller risk premium isn't going to be smooth. A constant flow of positive news on trade risk de-escalation is necessary, but probably not sufficient in the face of the damage markets think tariffs are already inflicting on the US economy.

We think there will be sustained support around the 1.1250-1.130 area in EUR/USD in the near term: that has proven to be the region where most dip-buyers emerge. The balance of risks is still skewed to the upside for the pair.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article