Federal Reserve: Setting the scene for a September cut

The Fed kept monetary policy unchanged, but offered enough for the market to keep faith with the 18 September FOMC meeting rate-cut call. Inflation is looking better behaved, the jobs market is softening and consumer spending is cooling, and with the policy rate well above neutral we look for 75bp of cuts this year with the potential for more in 2025

Press release signals the jobs market is a growing priority

The Federal Reserve has left monetary policy unchanged as universally expected, but the press release does show some subtle shifts in thinking. Previously it talked of the data showing "modest further progress" towards their inflation goal, but the word "modest" has now been removed. We take this as a sign that the slowing in the May and June core inflation prints have provided officials with greater comfort that inflation is finally on the right trajectory to target. Nonetheless, they do repeat that "the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent".

There is an acknowledgement that jobs gains are moderating. They have switched from saying only that the committee "remains highly attentive to inflation risks" to acknowledge that in the wake of rising unemployment they are "attentive to the risks to both sides of its dual mandate". Remember the Fed not only targets 2% inflation, but also maximum employment.

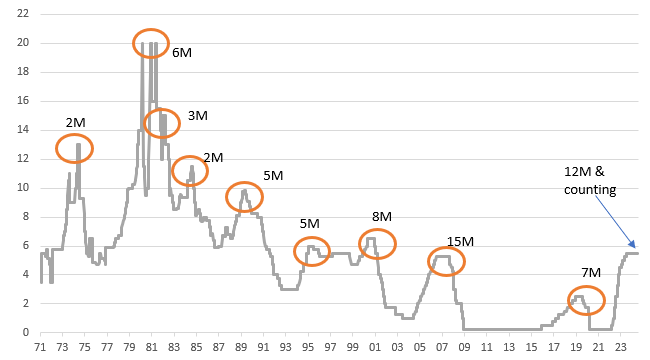

Fed funds rate and duration between the last rate hike and the first rate cut in a cycle

Chair Powell indicates a willingness to cut, but more data needed

As has typically been the case, Fed Chair Powell provided a slighty more dovish spin, signalling a willingness to cut, but emphasised that the data needs to be there to back it up – when questioned he stated the restrictiveness of policy is clear to see. He suggested if inflation data continues to moderate and the employment data cools further then they “could” be in a position to cut interest rates in September. Powell, mentioned that we are now seeing a "normalising" economy with lower inflation being seen in both goods and services, which is very good news. Moreover, within the press conference there was greater focus on jobs than has typically been the case, but again it is down to the data.

That said, the market appears to be a little disappointed that the Fed wasn’t more explicit on the potential for a rate cut, but we still have the Jackson Hole Conference at the end of August. That has been used in the past as a venue for signalling action and we believe it will be used again to do this if the data continues to move in the direction we expect.

On track for a September rate cut

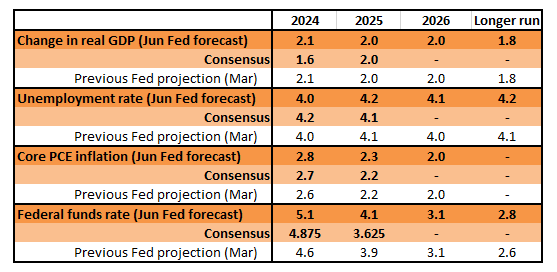

At their June forecast update the Fed signalled an expectation that growth and the jobs market would remain more robust than private forecasters thought likely and inflation would remain stickier. The result was that they signalled their central projection was for just one rate cut this year, versus the three they had suggested in March. However, the unemployment rate has already moved above their end year forecast (4.1% versus 4%) and with the labour demand series looking softer we would argue the risks are that it moves even higher. At the same time, the Fed’s fourth quarter 2024 GDP growth forecast of 2.1% year-on-year is now well above the 1.6% consensus figure from Bloomberg while inflation is just a little higher than the consensus at 2.8% versus 2.7%.

Federal Reserve central forecast versus the latest consensus surveys

The Fed has been striving for a “soft landing” and if the data allows them to cut, and it is certainly moving in that direction relative to their forecasts, then we think they will seize the opportunity. We expect officials to start moving monetary policy from “restrictive” territory to “slightly less” restrictive policy from September with additional cuts in November and December. At present we are forecasting three more cuts next year, but with the Fed seemingly placing more emphasis on jobs market data in an environment of cooling inflation, the risks are skewed towards them implementing more cuts.

The 2yr and 10yr are still heading to 4% in anticipation of a first cut by September

The edge higher in yields post the FOMC statement is understandable. Into the meeting the 10yr and 2yr yields had driven lower in a significant fashion in previous weeks, practically to the point where a material dovish pivot was required to help ratify recent moves. Neither the FOMC statement nor Chair Powell have said anything to stand in the way of a September cut. In fact, they’ve moved further in that direction. But there are enough ifs and buts in the running commentary, which is probably smart; some taming in the rate cut enthusiasm was warranted. There is still a sense that the Fed is winding up slowly to cut, and the follow-through reaction should eventually see yields resume their falls, but likely at a more subdued rate.

The spread from the 2yr yield to the effective funds rate been hitting new lows in the -95bp area as we build to a first rate cut in the cycle ahead. The magic level is -100bp, as traditionally once we hit that level the market is fully primed for a first cut, and the beginning of a sequence of cuts. The 2yr yield is now in the 4.35% area, and tracking towards 4% as a call in the coming couple of months. The reason for a longer term call is the Fed was never expected to cut at this meeting, and seems more minded to cut at the 18 September meeting. The 10yr yield is also tracking towards 4%. Now in the 4.1% area, the inversion of the curve is under 20bp. As the 2yr yield and the 10yr yield head towards 4%, the curve completely flattens out in the next couple of months.

In terms of liquidity conditions, the Fed has already pre-positioned with a prior tapering of the quantitative tightening process. This continues in the background, and has not yet hit levels where particular concern for liquidity circumstances are warranted. That said, we find it noteworthy that balances going back to the Federal Reserve on the reverse repo facility have been sticky at just under the US$400bn area, a material change from the big falls seen through 2023 and into early 2024. We view this balance as a manifestation of excess liquidity, and ideally should shrink in line with the quantitative tightening process. If it doesn’t, then bank reserves, now at US$3.3tn will be pressured to fall. Should they get under US$3tn, then we’ve have a contradictory material tightening in liquidity conditions, just as the Fed starts to ease interest rate policy.

Dollar a little softer given September cut in play

After a month in which FX markets were dominated by the unwind of carry trade strategies and the stronger yen, today’s Fed meeting squarely puts the timing of the Fed easing cycle back on the agenda. The dollar initially found a little support on the changes in the FOMC statement perhaps being a little too subtle for the market’s liking. Yet during the press conference the dollar turned broadly lower as Chair Powell seemed to deliberately put a September cut ‘on the table’.

It looks like the prospect of Fed rate cut in September will keep the dollar on the soft side over coming months. Employment reports will take on extra focus now that the Fed has squarely switched back to focusing on its dual mandate. And the Jackson Hole Symposium is another threat to the dollar.

In theory, this bullish steepening of the US yield curve should see benign weakening in the dollar, while activity and commodity currencies should outperform. Yet the carry trade unwind of July has caused carnage for the activity currencies and perhaps some unfinished business in the USD/JPY correction may discourage investors from returning to activity currencies just yet.

US data now is probably the biggest threat to a further unwind of short yen positions and a lower USD/JPY. We have already seen a substantial correction in market positions and the USD/JPY market is now much better balanced than it was at the start of July. We cannot rule out a further correction here given the prospect of Fed easing, yet we would not be surprised if some investors were to consider dipping their toes back into the carry trade were USD/JPY to trade under 150 and USD/MXN over 19.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article