Federal Reserve preview: More, more more…

Analysts are split on whether the Fed will cut rates for the third consecutive FOMC meeting, but we are of the view the Fed will ease again. A decelerating economy and falling inflation expectations will likely result in further rate cuts over coming months

The economy is starting to struggle

The Federal Reserve have been keen to characterize the two rate cuts in July and September as “insurance” against external threats posed to the US economy (trade & weak global growth) rather than the start of a significant easing cycle. This narrative may have to change if, as we expect, they cut rates for the third consecutive time next week.

The data flow over the past five weeks has clearly signaled a deceleration in US economic activity. What started out as a manufacturing downturn resulting from weak external growth, the headwinds from a strong dollar and the uncertainty and barriers to trade caused by the US-China tariffs, is starting to spread to the services and consumer sectors.

Business surveys offer worrying signal for growth

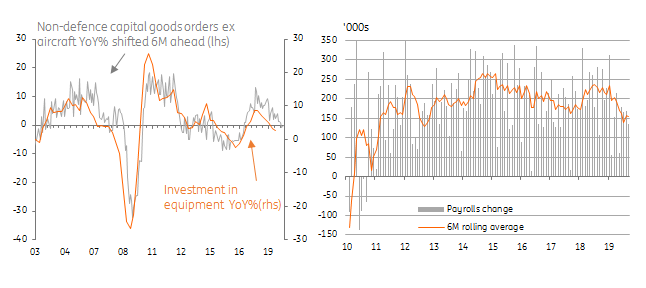

The ISM non-manufacturing index is heading lower, payrolls growth is slowing and retail sales fell sharply in September. With the outlook for corporate profits deteriorating and the durable goods orders report signaling a likely contraction in investment spending in both 4Q19 and 1Q20, it is difficult to see where the major positive growth drivers are right now.

The one area that is performing well is housing, buoyed by the plunge in mortgage rates and the fact that the unemployment rate remains low. However, the durability of this strength is questionable given the apparent slowdown in hiring and wage growth.

The outlook for investment and jobs is weakening

External risks may have moderated…

It is true to say that there has been a truce in US-China trade tensions. Trade talks went as well as could really have been hoped with a “phase one” agreement in the process of being finalized that involves China purchasing more US agricultural products in return of tariffs being held at current levels. We are less optimistic that we will see a true de-escalation that involves a roll back in tariffs in return for China acquiescing to US demands over intellectual property protection and technology transfer.

The threat of a disorderly Brexit at the end of the month also appears to have moderated, although it is probably best to describe the current situation in Westminster as “fluid”. Our assumption remains that the UK will be granted a short extension by the EU that allows the legislation to pass into law regarding the Withdrawal Agreement.

Equity markets have taken comfort from these developments. Nonetheless, external data remains weak with Chinese and European growth continuing to disappoint, but at least there is some talk about Germany softening its line on balanced budgets. There is a possibility that we could see some fiscal stimulus, although we acknowledge that it will take time to translate into real projects that contribute positively to economic growth. So while there are potential positives coming through from the external side, they are unlikely to translate into a stronger US growth story anytime soon.

…But downside inflation risks are a cause for concern

Inflation measures are certainly no barrier to a rate cut and are increasingly a factor why the Fed should cut rates further. Pipeline price pressures are easing with PPI having slipped lower despite higher tariffs while wage growth has slowed to 2.9% year-on-year having threatened to break above 3.5% at the beginning of the year. With the University of Michigan consumer sentiment report showing that long-term inflation expectations have dropped to all-time lows and market breakeven inflation rates using Treasury Inflation Protected Securities also on a downward trend there are potential warning signals surrounding the Fed’s ability to hit its medium-term inflation target.

Consumer and market inflation expectations are on the slide

A shift within the Fed? Probably not

At the September FOMC meeting there were clear divisions within the FOMC. Both Esther George and Eric Rosengren opposed the 25bp rate cut, favouring a no change outcome. However, James Bullard wanted a 50bp rate cut.

In recent speeches Esther George has continued to warn that lower interest rates “risks overheating the sectors of the economy that are already performing well”, although we would suggest that the recent data flow indicates there are few of these “hot spots” around these days. Likewise, Eric Rosengren will oppose another rate cut having said on October 11 that “my forecast for the economy does not envision additional easing being necessary”. James Bullard, meanwhile, continues to emphasise downside risks, encouraging “the committee to take action”.

Other Fed voters have been more equivocal in their views, but the general use of the word “risks” has been a key theme. Given the deteriorating growth story and the benign inflation backdrop we feel that a majority will once again come down in favour of a rate cut. Economists are mixed, but with the market currently pricing in 23bp of a 25bp rate cut for next Wednesday we believe the Fed will take action. Assuming the economy continues to soften in line with our view – we expect sub 2% 3Q19 GDP growth and sub 1.5% growth in 4Q – then the Fed will likely follow up with additional rate cuts in December and January.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article