Federal Reserve preview: More delays

The US Fed accepts monetary policy is restrictive, but lingering inflation and strong jobs numbers mean it will indicate it’s prepared to wait longer before seriously considering interest rate cuts. The “dot plot” will be key. Having signalled three 25bp cuts in 2024 back in March, it could potentially go to just one; we’re expecting two

No rate change, with 2024 cuts scaled back to two, possibly even one

The US Federal Reserve will keep interest rates unchanged at 5.25-5.5% on Wednesday and will indicate that September is the earliest opportunity to seriously consider an interest rate cut. The main focus will be their updated dot plot, which outlines the individual members’ views on the path for interest rates. In March, they signalled that three rate cuts for the year remained their central view, with three further cuts in 2025. There had been a sense they could have instead opted for just two rate cuts in 2024 in the wake of two consecutive 0.4%MoM core CPI prints and ongoing strong jobs numbers, but they decided to bide their time. It was close, with 2 members opting for no change this year, 2 for one cut, 5 for 50bp of cuts, 9 for 75bp and 1 for 100bp.

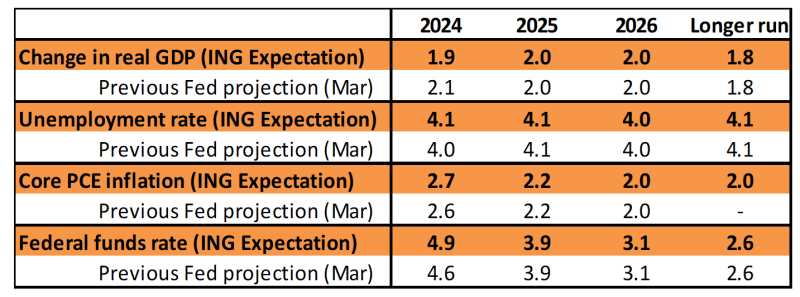

With inflation having remained sticky and the latest jobs numbers beating all expectations, we expect them to push their projections for rate cuts back next week, so they end up with two cuts in 2024 and four in 2025 instead of three and three. It is a close call and recognises that a Bloomberg survey showed 41% of respondents (including ING) look for two cuts in 2024, but there are also 41% who expect the Fed to signal one or none.

Lower growth and higher unemployment is why we don’t expect the Fed to go further

We don’t expect them to change their projections for the fourth-quarter core PCE deflator (2.6%) meaningfully, perhaps up to 2.7% or, at a stretch 2.8%, but there is a high chance they lower their 4Q GDP YoY growth projection (2.1%) closer to the 1.7% consensus forecast and raise their 4Q unemployment projection (currently 4%) to the consensus 4.1% or possibly 4.2% given we are already up at 4.0% and labour demand indicators are weakening.

The probability of lower GDP growth and higher unemployment is why we don’t expect the Fed to go further and reduce it to just one 25bp rate cut as their central view for 2024. Moreover, two rate cuts for 2024 would be closer to the market pricing, and they can emphasise it is the data that will determine the path forward for rates rather than implying they have a pre-determined take-off plan. Nonetheless, it is likely to be so close that one or two more hawkish members would have tipped the median to one cut. If that is the case, we expect Powell's press conference to signal this isn't set in stone, and if the data warrants it, they can do more - they won't want to be categorical about the outlook for rates.

ING expectations for what the Fed will predict in its new forecasts

May inflation to impact the tone of the press conference

Wednesday also sees the release of May US CPI inflation data, but with the forecasts submitted well beforehand, this report will not be reflected in the individual member projections. Instead, it is likely to influence the tone that Fed Chair Jerome Powell adopts in the press conference and the characterisation of the risks to the forecasts.

CPI has been running hotter than the Fed’s favoured measure of inflation, the core PCE deflator, for quite some time, reflecting the greater weighting of housing costs and insurance. We suspect it will come in at 0.3% MoM once again, which remains too hot, but so long as the core PCE deflator is 0.2%, we believe we remain on course for a Fed rate cut as soon as September.

We still look for rate cuts from September

The Fed believes monetary policy is restrictive at 5.25-5.50% in an environment where they view the neutral interest rate as being around 2.6%. They don’t want to cause a recession if they don’t have to and if the data allows them to start making monetary policy slightly less restrictive, we think they will take that opportunity, just as the Bank of Canada did on 5 June. For officials to be comfortable taking that course of action, we think they need to see three things:

More evidence of inflation pressures easing. If we can get two or three more 0.2% core inflation prints in quick succession that will be a necessary, but not a sufficient factor that leads to a rate cut.

More evidence of labour market slack. The unemployment rate has gone from 3.4% to 4.0%. If that moves convincingly above 4% with more evidence of a cooling of wages this too will help swing the argument in favour of rate cuts.

Softening consumer spending. It's the primary growth engine in the US and there was some evidence of that softening in 1Q GDP revisions and weak April spending data, but the Fed needs to see more. Flat real household disposable income growth, the exhaustion of pandemic-era accrued savings for millions of households and rising loan delinquencies suggest financial stress is materialising for many lower-income families, and this will indeed see a cooling in spending.

If we get all three of these, we believe the Fed will indeed seek to move monetary policy from “restrictive” to “slightly less restrictive” with 25bp rate cuts at the September FOMC meeting.

Rates are braced for a combination of interdependent factors

The Fed has been of the consistent opinion that the reverse repo facility is doing its job, which so far has meant the marketplace posting liquidity back at the Fed at their overnight facility at 5.35%. However, in the past couple of months, the volumes going back to the Fed have stalled in the area of $400bn. And this is despite the fact that quantitative tightening continues, albeit now at a slower pace. Extrapolate that, and bank reserves will begin to shrink, which will tighten liquidity conditions in a wider sense. The cleanest way to avert this is for the reverse repo balances to start falling again. We think this is what will happen, but we're interested in any opinion the Fed has on it.

In terms of yield direction, Treasuries had been beginning to build a rate-cut ambition for September. The fall in the 10yr yield from 4.5% to 4.3% pre-payrolls was a reflection of this, as had the decline in the 2yr yield to the 4.75% area. But post payrolls (which were reasonably firm), those yields are higher by some 10bp, and the markets' immediate rate-cutting ambition has been curbed. It swings the pendulum squarely back toward Treasuries needing a material fall in inflation to prompt a rate-cutting style rally.

Material rate cut expectations would see the next big figure for the 10yr yield at 4%. And for the 2yr it’s also got a target of 4% once the Fed gets going on cuts. But at the moment, it’s tough for Treasuries to build such a discount. In fact, given the payrolls data and the bulk of the recent inflation numbers, the risk is growing that we have rising yields going into the FOMC meeting, and Chair Powell will not be in a position to say much with any degree of credibility to negate this. If things don’t turn in a material fashion, we trend back towards 4.5% as a next tactical impulse, back to where we started, with 5% not a crazy level to worry about ahead.

Dot Plots unlikely to give the dollar a lift

Given that market pricing for this year’s Fed easing cycle has been running with fewer than two rate cuts since around mid-April, we doubt that an adjustment in the median Dot Plot to two from three rate cuts this year will provide the dollar with much of a boost. In fact, the dollar has ended the day lower on the last four consecutive FOMC meetings, largely because of the dovish-sounding press conference. And arguably, Chair Powell has slightly more dovish ammunition (think unemployment) at the upcoming meeting than he did on 1 May.

However, some European political uncertainty this month means that conditions are not right for a benign dollar sell-off, even if Chair Powell were once more to surprise on the dovish side. We again see EUR/USD continuing to trade around the 1.08 area into the French election on 30 June, but probably with downside risks.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article