Federal Reserve keeps policy unchanged, signals just one rate cut before year-end

The Fed left interest rates unchanged at 5.25-5.5%. Their updated forecasts leave 2024 growth and unemployment unchanged, but inflation projections are higher than previously thought as they signal they are on track to cut the policy rate only once this year. We think they will start in September with a high chance they end up cutting rates by more

Fed suggests they may cut just once this year, but the data ultimately determines the outcome

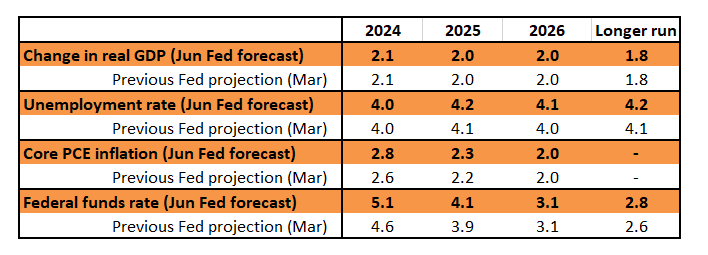

The Federal Reserve left monetary policy unchanged in a unanimous decision, as widely expected, but their updated projections signals just one rate cut before year-end versus the three they suggested in March. They are now projecting four rate cuts in 2025 versus the three they had previously, but this means the policy rate is expected to end next year 25bp higher than in their March forecasts.

The tone of the statement is a little more dovish, saying "there has been modest further progress" on getting inflation to target having previously said there had been "a lack of further progress". It is also important to point out that the dot plot is pretty evenly split between one and two cuts for this year – 4 members think no change this year, 7 think one cut, but 8 think there will be two. Previously in March it was 2 members opting for no change this year, 2 for one cut, 5 for 50bp of cuts, 9 for 75bp and 1 for 100bp.

Fed Chair Powell also sounded a touch more dovish than the projections implied, stating that the Fed welcomed today’s softer inflation print and that the FOMC “hope for more like it” – he did state that members were given the opportunity to change their forecasts in light of today’s inflation number, but this didn’t materially have an impact on the outcomes . Moreover, policy will be driven by the data, adding that these projections aren’t “a plan” and that they “can adjust”. For example, if the jobs market were to weaken the Fed is “ready to respond”. Nonetheless, he warns that “if the economy remains solid and inflation persists we’re prepared to maintain” rates at their current level.

Federal Reserve summary of economic projections – median forecast of individual FOMC member

In other forecasts the Fed retained a rather upbeat growth forecast of 2.1% for 4Q YoY GDP whereas the market consensus is 1.7% and left their unemployment rate forecast unchanged at 4% despite last Friday’s jobs report telling us we are already there. The core PCE deflator is now projected to end the year at 2.8% versus 2.6% previously. They have also raised their long run Fed funds forecast to 2.8% from 2.6%.

We think the risk is the Fed end up doing more policy easing over the next 18 months than they are signalling with the Fed funds target rate settling at 4% in 1H 2025. Over the long run their 2.8% neutral Fed funds rate, we think, is too low in an environment of ongoing loose fiscal policy irrespective of who wins the Presidential election, demographic change and the ongoing deglobalisation trends.

We still look for rate cuts from September

The Fed believes monetary policy is restrictive at 5.25-5.50% in an environment where they view the neutral interest rate as being around 2.8%. They don’t want to cause a recession if they don’t have to and if the data allows them to start making monetary policy slightly less restrictive, we think they will take that opportunity. For officials to be comfortable taking that course of action, we think they need to see three things:

More evidence of inflation pressures easing. If we can get two or three more 0.2% core inflation prints in quick succession that will be a necessary, but not a sufficient factor that leads to a rate cut.

More evidence of labour market slack. The unemployment rate has gone from 3.4% to 4.0%. If that moves convincingly above 4% with more evidence of a cooling of wages this too will help swing the argument in favour of rate cuts.

Softening consumer spending. It's the primary growth engine in the US and there was some evidence of that softening in 1Q GDP revisions and weak April spending data, but the Fed needs to see more. Flat real household disposable income growth, the exhaustion of pandemic-era accrued savings for millions of households and rising loan delinquencies suggest financial stress is materialising for many lower-income families, and this will indeed see a cooling in spending.

If we get all three of these, we believe the Fed will indeed seek to move monetary policy from “restrictive” to “slightly less restrictive” with 25bp rate cuts at the September, November and December FOMC meetings.

Treasuries are on a rate-cut-build path unless negated by data/events

Post the more subdued 0.2% MOM core consumer price inflation reading, Treasuries have been re-cobbling together the string of weaker observations seen in the past few weeks, and downsizing the importance of the firmer ones. We’re back to the build of a rate-cut bias, as had been seen in the couple of weeks prior to the firm payrolls report. The 10yr is back in the 4.3% area, and the 2yr at 4.7%. The target for both would be 4% should a rate-cut theme really build. The only real issue is timing, especially with the Fed dots now down to just one for 2024.

If the stars align and the Fed does cut by September, the twist is there is not a whole lot of room for the 10yr to stay below 4% for too long. If the Fed just gets to 4%, that would imply no term premium in the 10yr, and completely flat curve. Include the large fiscal deficit to the equation and we’d ultimately need to see a material term premium, in the area of 100-150bp. That easily brings a 5% yield back into the conversation. But, 4% first, provided the data behaves and allows for the build in the rate-cut discount, in particular for 2024 delivery.

Meanwhile, liquidity conditions remain ample but on a tightening trend. The past couple of months saw volumes going back to the Fed stalling the area of US$ 400bn. Extrapolate that, and bank reserves will shrink, which will tighten liquidity conditions in a wider sense. The Fed continues to voice broadly agnostic stance on all of this. This is mostly as the Fed is pre-positioned given the tapering in quantitative easing is already in place. As an aside, liquidity in Treasuries has deteriorated, adding another layer of issues that can spike volatility ahead.

Dollar edges higher on FOMC, but soft CPI effect dominates

The potentially hawkish headlines of a Fed scaling back its 2024 median easing plans to one from three rate cuts on another day could have provided quite a lot of support to the dollar. Yet the dollar’s initial reaction to the new economic projections was very muted. The dollar rallied a little further during Chair Powell’s press conference but has still barely retraced one-third of the sell-off triggered by today’s soft May CPI release.

In a way, Chair Powell seemed not quite as dovish as prior press conferences. When teed up to answer a question about the possibility of a September rate cut, he artfully avoided answering it. For dollar bears like ourselves it was slightly disappointing that Chair Powell was not offering a little more confidence about the opportunity to cut rates. But perhaps the main messages from the Fed today were higher inflation forecasts and the delayed Fed easing cycle.

Yet today’s soft US May CPI figure has probably set the near-term tone for the dollar. The market will be examining tomorrow’s May PPI data for clues about the May core PCE inflation data released on 28 June, where another 0.2% MoM reading presumably would add to the Fed’s confidence in easing.

And just as the ‘divergence’ narrative grabbed the headlines in April – and pushed the dollar to the highs of the year – it seems investors are now warming more to the convergence story. After all we have already started to see rate cuts in the eurozone, Canada, Switzerland and Sweden and it looks like US price data will allow the Fed to follow suit later this year. Notably, two-year EUR:USD swap differentials, which were at 160bp in favour of the dollar in April, have now narrowed inside of 130bp.

Softer US price data is seeing the high beta G10 currencies in Australasia and Scandinavia outperform. Assuming US price data continues in the same direction as today, these FX trends should continue. But it seems clear that given French political risk, EUR/USD will not lead in any further dollar data-driven decline. And indeed we are seeing and continue to favour downside breakouts in some high profile euro cross rates such as EUR/AUD.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article