Eurozone wage growth is set to peak soon

Slowing inflation, a cooling labour market, and lower expected corporate revenues make a peak in wage growth before the middle of next year likely. While the European Central Bank waits for clarity, this should open the door to earlier rate cuts than currently expected

The ECB has frequently emphasised that it wants to have a clear view of how wage growth develops in the first half of 2024 before giving the all-clear on rate hikes and possibly even deciding on a first rate cut. In this note, we look at how wage growth is likely to develop in the coming year. We approach it through the lens of labour shortages, expectations of wage negotiation outcomes, and corporate ability to increase wages further.

The job market is cooling off (a bit)

The eurozone labour market has performed remarkably well in recent years. Job growth has been stronger than GDP growth in recent quarters and unemployment has fallen to the lowest level in decades. This has resulted in widespread labour shortages, which has boosted wage pressures.

Even though unemployment has not yet ticked up, signs of cooling are starting to show. Vacancy rates have been falling from their record highs across eurozone economies in recent quarters and surveys indicate that hiring intentions have slowed substantially in 2023. It looks like employment growth is still positive for business services, but for manufacturing, there are good indications that employment growth will turn negative before the end of the year.

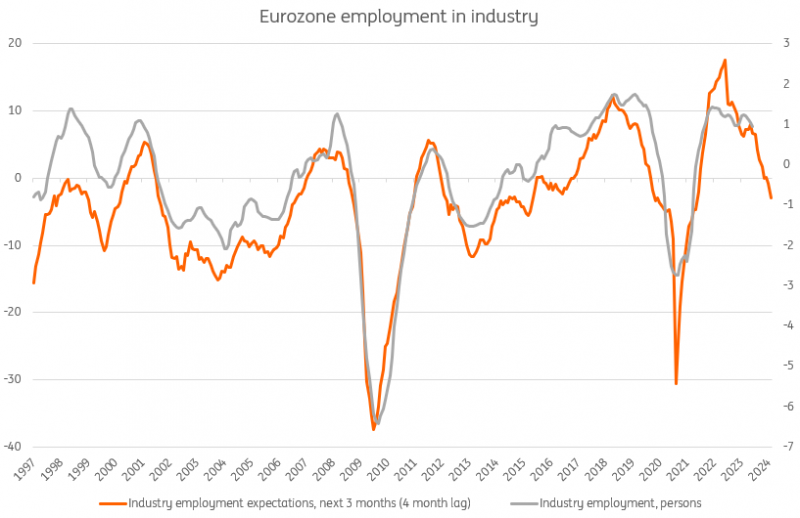

Industry employment is set to shrink from here on

Even if the services sector keeps overall employment growth positive in the short run, it is industry which usually provides the benchmark for negotiated wage agreements. If employment in industry starts to drop, this will likely have a broader impact on union demands for wages in 2024.

Negotiated wage growth moves slowly and some increases are still in the pipeline

Historically, inflation remains one of the most important drivers of wage growth in the eurozone as negotiated wage growth uses the cost of living as a key input. The rapid decline of inflation over the course of 2023 would therefore historically have a moderating impact on wage growth moving forward. As this coincides with a cooling labour market, it means more moderation in wage growth is to be expected. Using a simple model with historical relations, we would expect wage growth to trend in the low 3% range in 2024, down from the latest reading of 4.4% annual growth. This is not the time to be relying on historical relationships though.

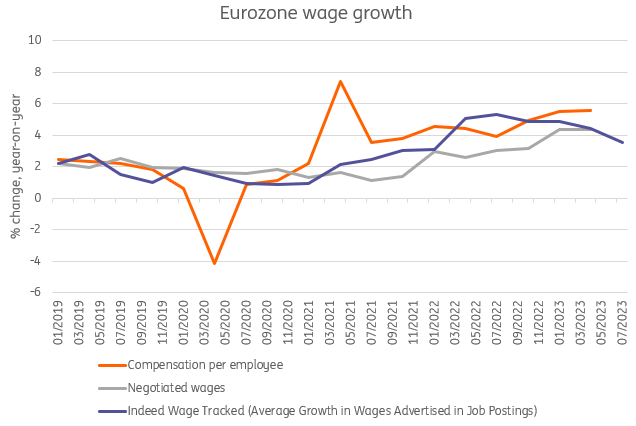

In fact, there are good reasons why wage growth will most likely turn out to be higher. Negotiated wages move slowly and are still adjusting somewhat for the high inflation of last year. Given the high inflation and resulting large negative real wage shock of last year, unions could try to go for yet another round of high wage demands. Also, unions might try to offset the end of one-off inflation compensation schemes with higher wage demands in 2024 and 2025. The ECB monitors the latest concluded negotiated wage agreements, which gives a decent sense of where overall wage growth will move in the first half of 2024. This seems to be hovering around 5% at the moment, somewhat above current levels. We don’t expect further acceleration on the back of market developments, but it doesn't look like a decline in negotiated wage growth is imminent either.

Outside of negotiated wage growth, wage growth for new hires also gives a sense of where wages are heading. The Indeed Wage Tracker provides an estimate for this, which is likely to move earlier than negotiated wages. Here, we see a cautious downward trend, which actually began in September of last year. That means that overall compensation growth per employee is set to come in somewhat below the negotiated wage developments as the market starts to turn.

Recent wage developments show the turn in wage growth for new hires

Will businesses allow their wage bill to rise much further?

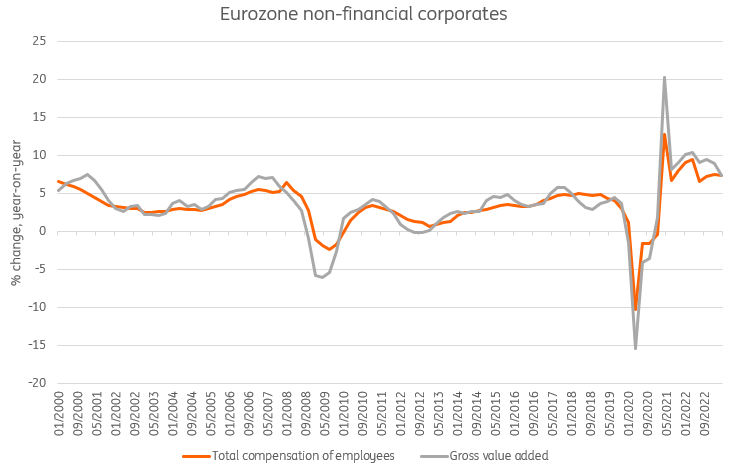

Looking at wages from the employers’ point of view also gives interesting insights into where wage growth might be headed in 2024. Historically, non-financial corporates have seen gross value added (a rough measure for revenues) increase more or less in line with the total compensation bill in the eurozone. See chart three. This indicates that when revenue growth slows, businesses slow down growth in total compensation paid. This can be done in two ways, either by shrinking headcount or by reducing average wage growth.

Compensation growth rarely exceeds gross value added growth for corporates

Compensation growth for non-financial corporates is slightly less volatile than growth in revenues, but overall there have been no examples of severe deviation between the two since the start of the time series in 2000. The pandemic threw numbers off – as happened everywhere – but recent quarters are already more in sync again. With inflation falling quickly and real economic activity currently stagnating, the compensation environment for corporates is changing quickly. Annual gross value added growth trended around 10% for most of 2022 but came down to 7.4% in the second quarter of 2023.

Whereas last year, strong price growth and decent volume increases allowed for very high overall compensation growth, 2024 will look very different. We expect nominal growth of corporate value added will drop to between 3% and 4% for 2024, which means that a significant squeeze for compensation growth will occur. As a result, employers might be forced to lay off employees and/or reduce average compensation per employee.

There is an element of chicken and egg here of course. Some would be quick to argue that higher wage growth would also increase pressure on businesses to continue to force through higher prices, which would increase revenues. This risk is clearly present as productivity growth is negative at the moment, which means that unit labour costs – the most common measure of wage cost pressures – can still increase enough to cause price pressures at lower levels of wages. We recognise this as an upside risk to the wage outlook. Still, the economic environment has become markedly weaker in recent quarters and businesses are reporting that it is harder to price through higher costs to the consumers. That makes continued slowing revenue growth a more likely prospect.

Wage growth is set to trend down again next year. Is the ECB behind the curve?

All in all, we deem it likely that wage growth will peak before next summer and start to trend down over the course of next year for a number of reasons. The only question is how fast wage growth slows, not whether it will. Given the ECB’s rather unsatisfying track record for forecasting inflation, it is not the time yet to publicly discuss the policy implications of such a plateauing of wage growth. This is why the ECB wants to wait for more evidence on how wage growth develops in 2024. The experience of the 1970s, when continued high wage growth allowed inflation to remain far too high for far too long, combined with the recent failures to forecast inflation, is keeping the ECB on high alert. For the time being, the ECB still prefers to err on the side of (too) tight monetary policy, rather than premature easing. However, if we are right and wage growth starts to turn soon, the ECB’s current stance would be too restrictive. Once the ECB officially gives the all-clear on wage growth, the door for rate cuts is wide open. Last week, ECB President Christine Lagarde said that rate cuts could not be on the ECB’s agenda for the next quarters. While this undermines our call for rate cuts next summer, we look back at comments made by Lagarde at the end of 2021. Back then, she didn’t expect ECB rate hikes in 2022.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article