Double-digit eurozone inflation is within touching distance

Supply shocks continue to plague the eurozone economy, causing inflation to show few signs of abating in the short run. Current natural gas prices make an inflation peak in double digits realistic, and there’s little the European Central Bank can do about it

With the US inflation rate easing substantially in July, there have been optimistic notes about a peak in inflation being reached. Month-on-month, inflation was actually 0%, which has encouraged people to think that the worst may be behind them and that a soft landing is possible. We don’t want to pre-empt our colleague James Knightley’s analysis on whether or not US inflation has peaked, but we are very convinced that eurozone inflation is still far off such a turning point. Differences between US and eurozone inflation are still significant. While the US has seen headline inflation fall, it has continued to increase in the eurozone. Month-on-month, July saw stagnation in inflation in the US, while in the eurozone it was still 0.6%. This is only one difference. In this note, we break down the most recent inflation developments in the eurozone and look ahead at why double-digit inflation is a realistic prospect for the months ahead.

Eurozone inflation is just under 9% at the moment

Monthly developments in eurozone inflation are moderate, but remain well above target

In times when inflation is extremely volatile, it’s useful to look at the month-on-month developments instead of year-on-year as we usually do. Eurostat does not provide seasonally-adjusted data to allow for monthly comparisons, so we use our own seasonal factors to estimate the most recent developments.

Inflation declined month-on-month in June and July, well down from the March peak when the war in Ukraine started. At 0.6% month-on-month, this still amounts to an annualised rate of 7.2% though, clearly an unacceptable level. Monthly core inflation also remains elevated and does not yet show a declining trend. It is currently at 0.3% month-on-month, which is 4.2% annualised.

It comes as no surprise that the surge in gas prices has once again dominated the increase in monthly inflation. The surge in market prices has caused consumer gas and electricity prices to surge by 3.9% in July, which was to a large degree offset by a -3.6% drop in fuel prices as lower oil prices have made prices at the pump somewhat more friendly. Food prices continue to be a problem, although inflation for unprocessed food has been abating. Processed food prices still increased by 1.3% in July.

Inflation continued to rise due to broad-based monthly contributions in July

The continuing high monthly core inflation rate was mainly due to goods inflation accelerating to 0.8% on the month. This is in contrast to the US, where goods inflation is abating. So, despite dropping goods consumption, price increases still accelerate. Inflation for clothing and goods for recreation was still moderate, but vehicles, furniture, and household equipment all experienced strong price rises again. Services inflation has been moderating but ticked up a bit in July as prices related to tourism and public transport surged by around 1% on the month. Overall, services inflation has moderated in recent months.

At current monthly rates, inflation is set to remain high for a while to come and a peak above 9% is most likely, with a chance of double-digit inflation becoming stronger.

Global supply-side inflation pressures are fading, but specific European ones remain critical

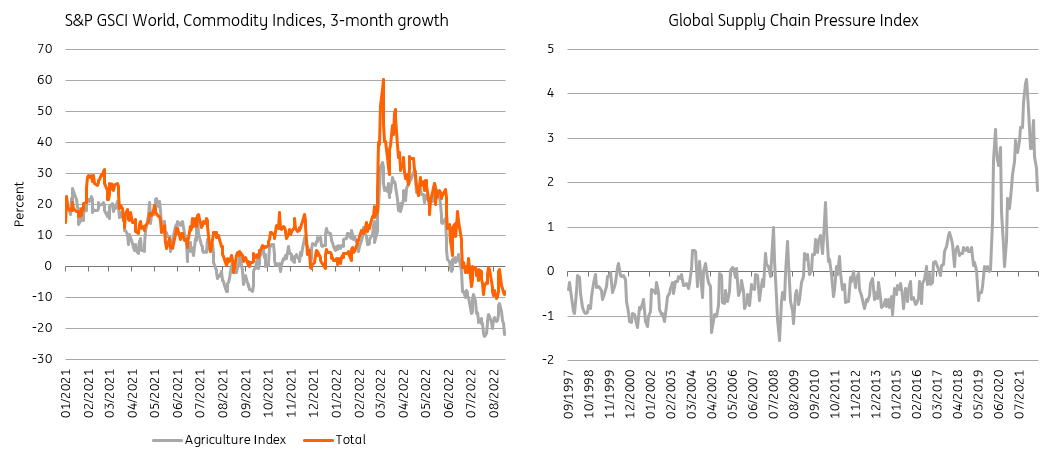

Relief on the inflation front is partially coming from cooling supply-side pressures. There has been a marked turnaround in a few factors that have driven up prices over the past two years. Supply chain problems have been fading, which is causing prices for transport and inputs to decline again. Think of container prices, which are now almost 50% below their peak from September last year. Survey data suggest that the number of eurozone businesses experiencing problems from a lack of equipment is declining. Critically, there has also been a relief in global agriculture prices, which have dropped to levels seen pre-war. Oil prices have also been sliding, which has had a favourable impact on global fuel prices.

Global supply factors are improving the inflation outlook

Some specific European factors are set to keep supply-side inflation elevated though. The low gas supply and low water levels are keeping pressure on prices higher than elsewhere. Another peak in natural gas prices has been reached, which is currently almost 10 times as high as it was in early 2021. Importantly, it is also twice as high as it was in late June. With concerns about fill levels in the winter and expensive liquefied natural gas (LNG) imports used to fill storage, it is likely that prices will remain elevated throughout the year.

Energy prices are also impacted by the troublesome low water levels. This is causing problems in cooling nuclear plants and river transportation of coal supply. Furthermore, the low water levels are hampering manufacturing production in Germany as supplies are harder to transport. So while global factors are bringing relief at this point, specific European supply-side problems related to the drought and energy are set to keep pressure on prices in the months ahead. Let’s also not forget the recent announcement by the German government on a gas levy. This levy will push up retail gas prices much higher as early as October. Another spur in headline inflation is in the making. We cannot exclude that other European governments will follow the German example, which in turn would add to inflationary pressure in the winter.

Demand continues to play a backseat role to inflation in the eurozone

Supply-side factors remain dominant in eurozone inflation, which continues to make the European Central Bank's role in bringing inflation down limited. The eurozone economy still has an output gap, real wage growth is vastly negative at the moment, and household consumption has far from recovered to pre-pandemic levels. Even though the economy is still in recovery mode according to the latest GDP figures for the second quarter, a recession is looming. Consumers have been spending on services due to a post-lockdown effect, but retail sales have already been trending down since November and consumer confidence is at an all-time low in the eurozone. The squeeze in purchasing power that high inflation is causing is set to have a significant effect on spending in the months to come.

Wages are also still disappointing in terms of their recovery. While the first quarter saw a temporary spike in eurozone negotiated wage growth due to one off-payments in Germany, the second quarter will have likely seen a drop again. Wage growth in Italy remains stubbornly low, while other countries are seeing a cautious upward trend towards pre-pandemic levels at the moment. The question is how the large bargaining agreements in the coming months will play out, but most demands have remained modest. For now, there is not much that points to a wage-price spiral.

Inflation is set to turn a corner, but expectations are key

The eurozone is in for a tough second half of the year. The peak in inflation is hard to determine as energy prices are currently incredibly unpredictable and still have a dominant effect on headline inflation, and even on core as businesses have to price through higher energy costs to consumers at these prices. A peak above 9% headline year-on-year inflation is logical at this point, but a jump to above 10% is clearly not unimaginable given the high market gas prices. We already hinted at such a peak in our earlier note from March.

For the European Central Bank, it is not about current headline inflation but about future inflation and inflation expectations. The bank knows very well that it can do little to actively bring down inflation in the short run and we doubt that, contrary to the Fed, the ECB would be willing to push the eurozone economy into recession. In fact, it doesn’t have to as the eurozone economy is already heading that way. For inflation, this means that companies’ ability to pass through higher costs to consumers will drop quickly; in fact, it has already started to.

Inflation expectations have been on the rise, but businesses are becoming less eager to price through

The ECB currently has two main goals: anchoring inflation expectations and normalising monetary policy. As for inflation expectations, only business inflation expectations have come down somewhat. The US example, however, shows that even more aggressive rate hikes are less powerful in bringing down survey-based inflation expectations than global commodity prices. The latest drop in US inflation expectations seems to be the result of dropping gasoline prices and not so much of the latest Fed rate hikes. This leaves the ECB with at least normalising monetary policy.

Consequently, we still expect the ECB to take a less aggressive approach than the Fed and what markets are currently pricing in. We expect the ECB to hike rates by another 50bp at the September meeting and then pause until spring next year. A recession, a winter energy crisis, and an ongoing war simply argue against overly aggressive rate hikes.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article