Eurozone: Backroom politics to the forefront

Last year was a good year for eurozone integration. But aside from the vaccination chaos, the potential political fallout looks much less spectacular this year. However, we think behind the scenes; some important next steps will be taken about the future of the eurozone in 2021

Desperate times called for historical measures

2020 turned out to be another testing year for the eurozone. Doubts about national governments’ fiscal firepower to tackle the pandemic, enhanced by comments by ECB president Christine Lagarde that it wasn’t the central bank's job to keep spreads narrow and she had no intention of her own whatever-it-takes moment, brought back euro crisis memories.

It took a while, but in all fairness, national fiscal stimulus, cheap funding for countries in need, the ECB’s pandemic emergency purchase programme and finally the Recovery and Resilience Fund (RRF) marked an unprecedented policy reaction, both in terms of size and swiftness.

The most relevant and novel measures included:

- Creation of the recovery and resilience fund - a fund that disburses grants and loans for which the EU directly borrows from the markets. (672.5 bn euro)

- National fiscal stimulus worth on average 3.8% for the EU and even 11% of GDP for Germany.

- The unconditional use of the European stability mechanism loan facility for health-related purposes up to around 2% of GDP for eurozone economies.

- The SURE programme, which allows governments to borrow for short-time work scheme funding (100bn euro).

- The creation of the pandemic emergency purchase programme, in which the ECB allows itself to deviate temporarily from capital key, which is not a political decision and therefore beyond the scope of this note.

To remind you of what a difference a year makes, cast your minds back to October 2019 when the French president Emmanuel Macron called for a eurozone budget that was just 17 billion euro for all 19 eurozone members, spread out over seven years and not meant for stabilisation. A meagre sum that it could hardly count as a symbolic victory.

This year is unlikely to be as spectacular as 2020, at least not when it comes to new measures. However, behind the scenes, 2021 could be an important year to set the future course of the eurozone

After teething problems, the European response to the crisis led to positive reactions from the market with spreads between government bond yields narrowing and a strengthening of the euro exchange rate - a clear message of European solidarity and pricing out any break-up risk. Investors have been comforted by the EU's ‘leave no country behind’ policy, even if most measures have been explained as exceptional cases and one-offs. Investors seem to be taking the view that every permanent crisis-fighting tool starts with a ‘one-off’.

However, this year is unlikely to be as spectacular as 2020, at least not when it comes to new measures but behind (and in front) the scenes, 2021 could be an important year to set the future course of the eurozone.

Just think of discussions on debt cancellation, fiscal rules review, implementing the recovery fund and national elections.

The debt cancellation debate

The pandemic has not only put a lot of strain on the health system and the economy at large, it has also increased already bloated debt levels in Europe.

Public debt in the eurozone has grown by about 15 percentage points since 2019 and is now hovering around 100% of GDP, with some countries clearly above that level. At the same time, the eurozone needs to invest to counter the structural growth decline and realise its green and digital agenda.

An opinion piece in Le Monde co-signed by more than 100 economists across Europe calls for the write-off (or transformation in a 0% interest rate perpetual) of the almost 25% public debt held by the ECB. While they bravely state that “In full compliance with the law and contrary to what some heads of institutions – including the ECB – claim, cancellation is not explicitly prohibited by European treaties.”, as cancelling the debt would effectively be monetary financing of public debt, which is not allowed according to ECB treaties, something that Lagarde was quick to point out.

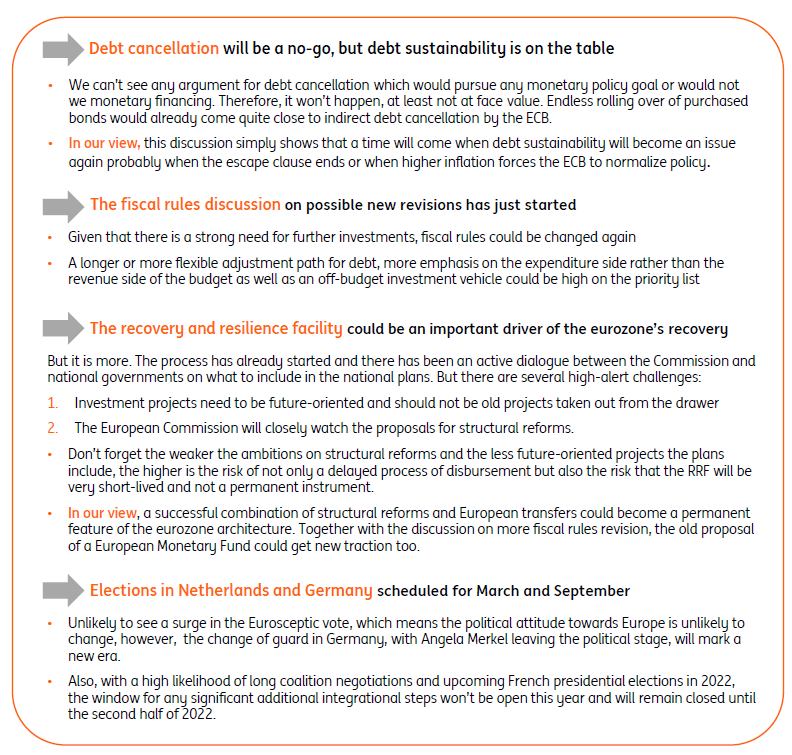

Debt cancellation will therefore be a no-go, but debt sustainability is on the table

Needless to say that the German constitutional court, which was already very critical of the public sector purchase programme, would go berserk if the ECB ever thought of public debt cancellation. Also, the European Court of Justice pointed out that bond purchases were only allowed for monetary policy purposes. So, it is hard to see that anyone could argue that cancelling the debt would benefit monetary policy.

It’s all cosmetics

But even if the idea would come to fruition, it would not change that much. For starters, the central bank is actually owned by the government and within the monetary union, governments receive dividends from their national banks, which in turn receive their share of the ECB’s profits. If the ECB exchanges interest-bearing debt on the asset side of its balance sheet with a zero-coupon perpetual, then, of course, the central bank’s profits will decline in the future, especially when short term interest rates on the liability side of its balance sheet increase.

This will result in lower dividends for the governments in the future, so, this debt cancelling would pretty much amount to a cosmetic operation without necessarily changing public finances very much. Also, don’t forget that the ECB has announced to roll over its bond holdings, reinvesting maturing bonds. If the ECB was to continue with this approach, it would already be very close to debt cancellation (though the ECB will have to make sure that its bloated balance sheet serves a monetary purpose). On top of that, the weighted-average interest rate on Eurozone debt is currently negative. Even for Italy, an important part of the yield curve is below 0% - in other words, currently, member states can borrow to finance the necessary investments while decreasing debt service costs.

Even if currently a common belief is that government debt could increase endlessly as long as interest rates are low and deficit-funded investments increase growth, a time will come when debt sustainability will become an issue again probably when the escape clause ends or when higher inflation forces the ECB to normalise monetary policy.

Debt cancellation will therefore be a no-go, but debt sustainability is on the table.

Stability and Growth pact - the elephant in the room

In our view, the discussion on debt cancellation and debt sustainability has to be seen in the broader context of fiscal rules.

Not only is the ECB conducting a review of its policy strategy, the European Commission last year announced yet another review of the eurozone’s fiscal rules. Also, European governments will have to decide on possibly extending the so-called escape clause, at least until 2022 or perhaps even longer.

The escape clause was triggered last year which means countries temporarily don't have to adhere to the budget rules as the economy is in a severe downturn. In November 2020, the European Commission indicated that the clause will remain active in 2021 too.

However, given that we think Eurozone GDP is unlikely to return to pre-crisis levels before the end of 2022, in our view, it might be unwise to significantly tighten budgetary policy before. As the escape clause has to be approved by the Council and budget proposals have to be handed in by October, a heated discussion is likely to ensue as diverging opinions will grow as the crisis nears an end.

Here, the memories from the financial crisis should help European governments. After the financial crisis, member states were too quick to bring public finances back on track and the austerity proved to be counterproductive as weakest member states saw their debt-to-GDP ratios rise on the back of tightening fiscal policy.

Countries with stronger austerity efforts saw debt rise more quickly in the euro crisis

Fiscal rules and the stability and growth pact has already been reviewed and changed many times. The last time was after the financial crisis when the so-called fiscal compact was introduced, trying to tighten the rules and introducing constitutional debt brakes. The IMF's Article IV report also recommends it would be an opportune time for fiscal rules reform.

There are still weaknesses in the eurozone’s fiscal rule. e.g. the debt sustainability criteria forces countries to diminish their debt at a speed which is determined by their actual debt ratio and the 60% debt-to-GDP threshold. However, with debt ratios rising significantly, this recommendation would actually lead to overly restrictive fiscal policies. A discussion about what sustainable public finances actually entail will have to be held and the answer might be different for each country.

In the past, issues like a possible expenditure-based rule or a golden rule allowing for more public investment over the cycle or more focus on reducing government debt have been discussed but there has never been a clear conclusion or preference for either a pure rules-based system or discretionary fiscal policy. A very practical problem has always been how to define investments or any such exemptions from the rules. While in theory, the principle of adjusting the fiscal rules to allow for more investments sounds very attractive, the experiences of the last twenty years (France, Germany or Greece) have illustrated how difficult any such definition or exemption can be in practice.

An elegant way out of the constitutional debt brake could be a temporary off-budget investment initiative

In our view, there will be room for looser fiscal rules and in this regard, the latest developments in Germany are remarkable. Not only did the government decide on the largest fiscal stimulus package of all European countries by far, it also seems to have taken a more structural u-turn on fiscal policies. However, how difficult a significant shift of the next German government will be was illustrated by the recent discussion on the constitutional debt brake. A proposal by a close Merkel-ally to have a discussion on whether several years of triggering the escape clause should be preferred over changes to the debt brake was quickly closed. Still, we expect this discussion to resurface after the elections but admittedly, it is hard to see how any CDU-led government would officially give up on the debt brake. However, an elegant way out could be a temporary off-budget investment initiative.

At the European level, the discussion has only just started. Given that – similar to the German situation – there is a strong need for more investments, the fiscal rules could be changed again. A longer or more flexible adjustment path for debt, more emphasis on the expenditure side rather than the revenue side of the budget as well as an off-budget investment vehicle could be very high on the priority list.

Recovery and Resilience fund - one-off or start of a new era?

The most closely watched EU theme of 2021 will be the start of the recovery and resilience fund.

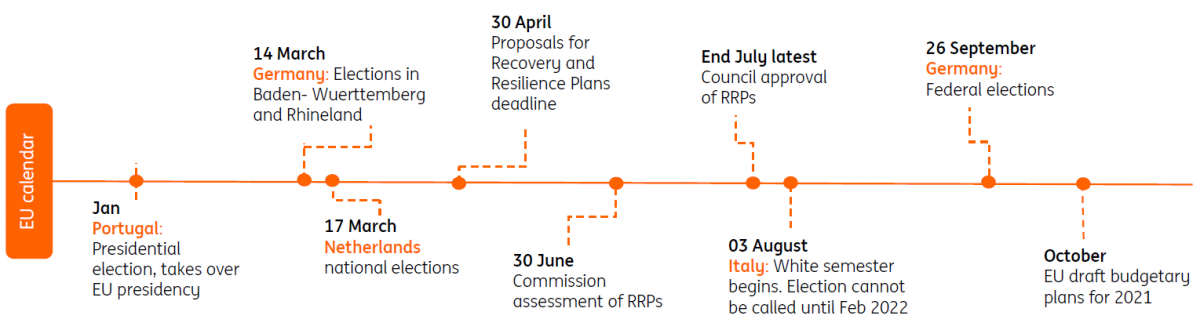

Proposals will be handed in by 30 April, so expect formal proposals to be rolling in from March. The recovery and resilience plans (RRP) will entail reforms and investment proposals that wrap up into coherent themes and show how much is requested in terms of investment and the reforms proposed. The plan will give a sense of how much stimulus will potentially flow to countries in the recovery phase of the crisis, but as the European structural funds' show, the take-up is often much lower than maximum reimbursements.

Expect the plans to have a heavy focus on digitisation and sustainability where each plan will have to have at least 37% of green initiatives and 20% digital investments, which make for a sizeable amount of total expenditure going into digital and green projects. This could prove to be a challenge for some countries and is likely to be the most politicized part of the RRF.

Expect the recovery and plans to have a heavy focus on digitisation and sustainability where each plan will have to have at least 37% of green initiatives and 20% digital investments and is likely to be the most politicized part

The Commission will assess the plans before 30 June and the European Council will approve before the end of July. At that point, we will find out if the Commission and EU leaders will just stamp the proposals or if there will be significant negotiation leading to delays in funding. This also sets the scene for the remaining three years as member states have the option to escalate progress concerns over other countries to the Council. This process has already started. There has already been a very active dialogue between the Commission and national governments on what to put into national plans and among the several high-alert challenges is not to include old investment projects from the bottom of the drawer as they need to fulfil the criteria of future-oriented projects.

Also, the European Commission will closely watch the proposals for structural reforms. The weaker the ambitions on structural reforms, the less future-oriented projects the plans include, the higher the risk becomes of not only a delayed process of disbursement but eventually minimising the chances of the RRF becoming a permanent instrument. If anything, the recent nomination of Mario Draghi as Italy’s prime minister, bodes well in this regard, as Italy will be closely watched by some of the more hawkish member states.

European politics in 2021

The political calendar is relatively empty for the eurozone this year now that Mario Draghi has formed a new Italian government, and we think elections in Italy will only take place at the end of the legislature in 2023.

However, both the Netherlands and Germany have elections scheduled for March and September, which we think are unlikely to see a surge in the Eurosceptic vote, meaning that the political attitude towards Europe is unlikely to change. However, the change of guard in Germany, with Angela Merkel leaving the political stage, will mark a new era.

Also, with the upcoming French presidential elections in 2022, the window for any significant steps toward further European integration is unlikely this year and will probably remain on the back burner until the second half of 2022.

European political calendar for 2021

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

17 February 2021

How green was my credit? This bundle contains 7 Articles