EUR/USD: Real interest rates still important

- 30 March

- FX

With so much news from the Gulf and energy markets dominating, it would be easy to disregard the impact of interest rate differentials on major FX pairs, like EUR/USD. Yet now, more than ever, the relative stance of central banks against this inflation shock will be relevant for FX pricing – particularly through the prism of relative real interest rates

Policy rates versus inflation expectations

Most analysts would have argued, and we did, that EUR/USD should trade lower from this month’s Middle East energy shock. The focus has been very much on a 2022 playbook, where Europe’s exposure to imported fossil fuels delivers a big terms-of-trade shock to the eurozone, while US energy independence is rewarded.

In this fast-moving environment, the relative monetary stance of central banks can easily be overlooked. Or indeed, one can argue that this month’s sharper re-pricing of tighter ECB relative to Fed monetary policy, in terms of nominal interest rates, might have been providing EUR/USD some support in an otherwise very offered environment.

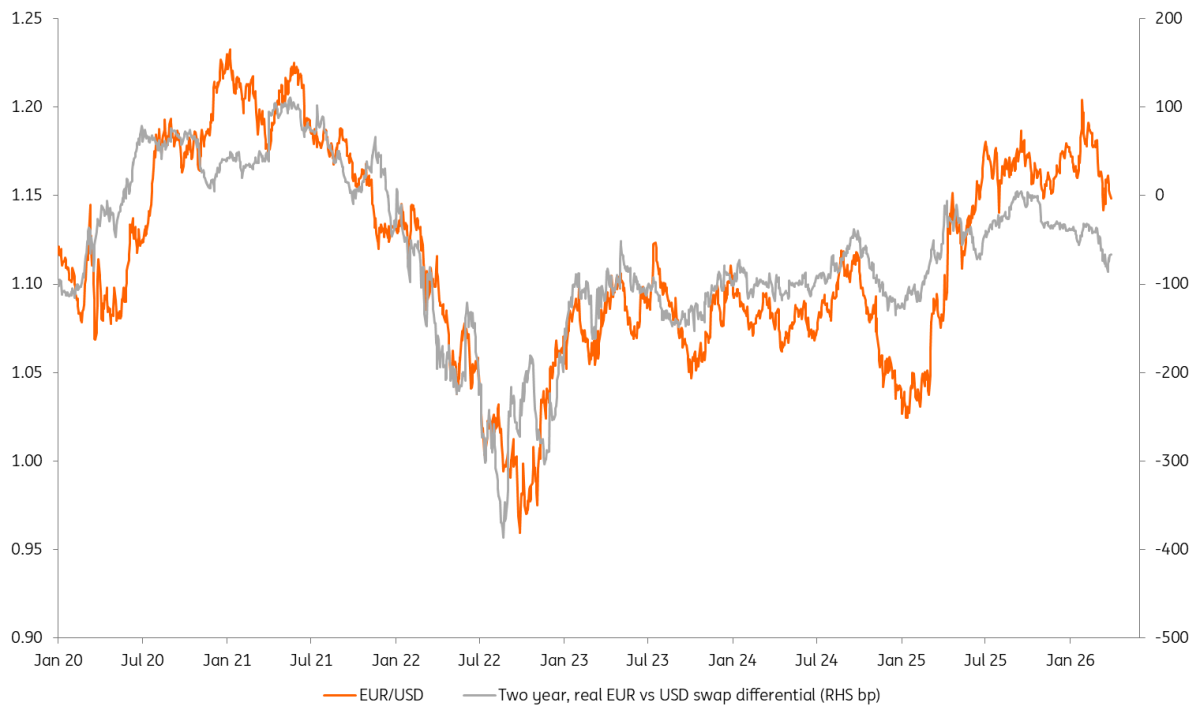

However, when looking at real interest rate differentials, the story is a little different. Using inflation expectations derived from the zero-coupon inflation swaps for both the dollar and the euro, we can adjust nominal swap rates to create a real interest rate differential – see chart below. The chart delivers a timely reminder that it was not just the terms of trade story hitting EUR/USD hard in 2022, but also the relative setting of real interest rates.

The dominant story in 2022 was a huge swing in two-year USD real rates from -250bp to +200bp – much greater than the adjustment in expected ECB real interest rates that year. A Fed wanting to try and get in front of the inflation story with a higher real rate was a major driver of dollar strength that year.

EUR/USD versus two year real swap rate differentials

What’s the story for 2026?

Even though nominal yield spreads have narrowed in favour of EUR/USD this month, real interest spreads have moved in the opposite direction. Our major call this year is that central banks are not as behind the curve as they were at the start of 2022 and that we should not, especially from the Fed, be expecting a major hawkish reset of policy which would demand a much stronger dollar.

But the above does present a note of caution to the ECB. Should the ECB not deliver on rate hikes, even with energy-driven inflation expectations remaining at 2.75% through the EUR inflation swaps, then real rates could move further against the euro and leave EUR/USD more vulnerable.

Currently, our baseline set of market forecasts see EUR/USD holding around the 1.15 level over coming months on the back of energy flows restarting in the Gulf. But continued high or higher energy prices and an ECB not prepared to hike would leave EUR/USD at risk to the 1.12 area.

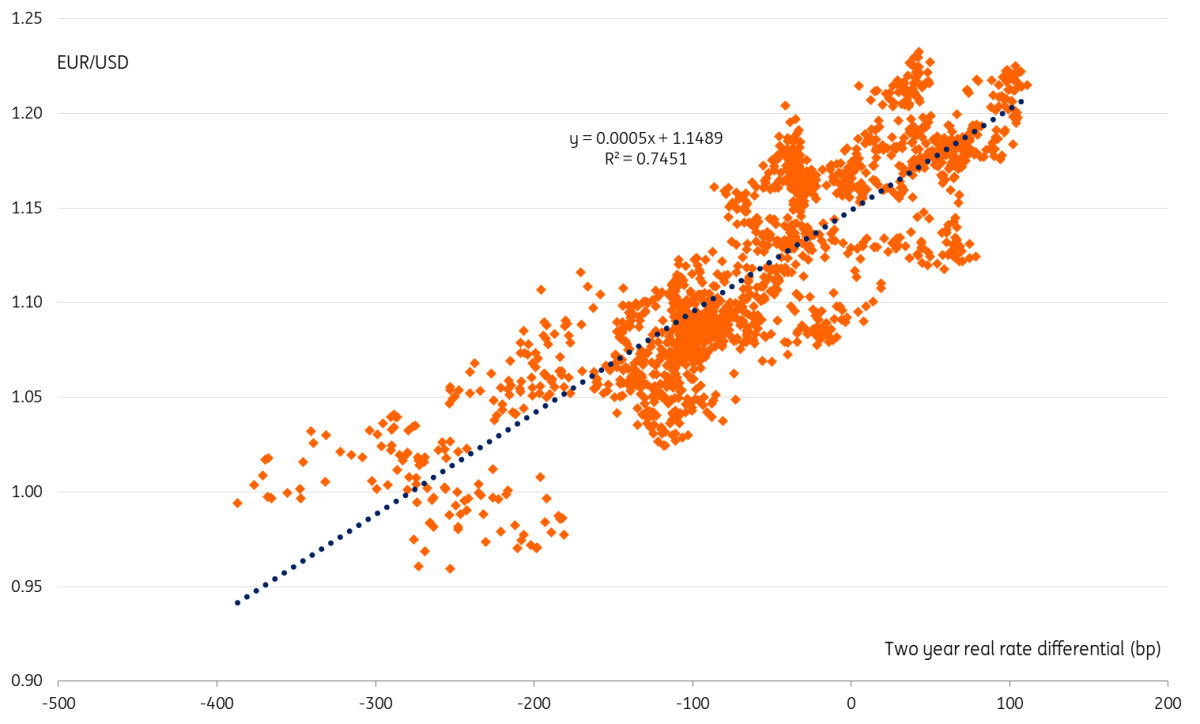

EUR/USD versus real rate spread scatter - a stable relationship

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more