EUR & ECB crib sheet: Lifting the euro is a hard task

A 25bp rate hike and openness to a 50bp move in September may fall slightly short of market expectations and add some pressure to the euro this week. The European Central Bank is unhappy with a weak euro, but its ability to offer sustainable support to the currency may continue to prove limited

What to expect on Thursday

As discussed in our July ECB preview, we expect policymakers in Frankfurt to deliver the previously announced 25bp rate hike on Thursday and leave the door open for a 50bp increase in September. The overnight index swaps market is pricing in 30bp for this week and nearly 200bp of tightening by June 2023. We suspect that the Bank's message may fall slightly below market expectations, and trigger some dovish re-pricing across the EUR curve.

The deployment of the anti-fragmentation tool will be all the more interesting as the recent Italian political crisis (which we analysed in detail here) has increased the chances of a sharp re-widening of Italian sovereign spreads. Here, the details about the conditionality to access the anti-spread tool will be key and may drive part of the market's reaction.

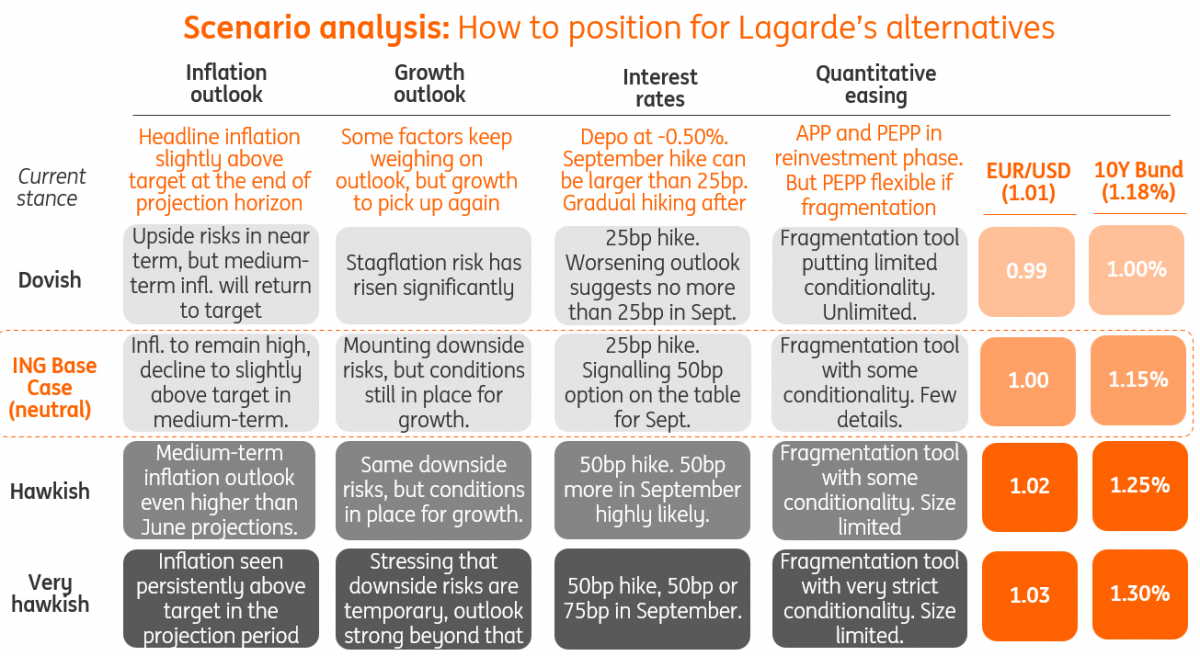

We identify four different scenarios (with the second being our base case) ahead of this week’s ECB policy announcement, and we include our estimated impact on EUR/USD and German 10Y yields.

Fighting a weak euro is not easy

There is no doubt that the ECB is unhappy with the recent weakness of the euro – not only against the dollar, but on a trade-weighted basis. Recent hawkish surprises by the ECB have, however, failed to offer sustained support to the euro, and we suspect that a larger-than-expected move (a 50bp rate hike) or more hawkish-than-expected forward-looking language may fail to generate enough lift to the euro.

This is especially due to the mounting downside risks in the eurozone, mostly related to the threat of a gas supply crunch in the coming months (or during winter) and more recently about Italy falling back into political uncertainty.

Our base case for EUR/USD is that it can re-test parity this week – with the ECB potentially being a trigger – and that it may only come back to levels above 1.0300 once the dollar loses some momentum (which would require some stabilisation in risk sentiment) and markets feel somewhat comfortable with the magnitude of the economic downturn priced into European assets.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article