Why the new growth chapter for EU manufacturing is set to be a slow burn

US protectionist policies have sabotaged new prospects of growth for European manufacturing. German investment plans and EU-wide increases in defence spending could provide a gradual boost, but we think significant growth is probably going to be a story for 2026

Growth phase postponed as trade uncertainty hits new peak

Just as a new growth phase seemed to be inching closer, European manufacturing is now facing a new era of trade turmoil. A longstanding decline in industrial production across the region emerged in the first quarter of 2023 – but just as we've started to see it bottoming out, US President Donald Trump's tariffs have taken the sector by storm.

Rising levels of trade uncertainty are now intensifying the pressure on both low confidence levels and a limited willingness toward investment, and this is bad news for goods-producing sectors like manufacturing. 20% reciprocal tariffs have been postponed for 90 days, but 25% tariffs on steel, aluminium, cars and auto parts remain in place for now. Most other EU-manufactured goods are now subject to a 10% tariff.

Still, February saw production in both the EU-27 and the eurozone rising to the highest level since August last year on the back of American frontloading. Improved purchasing power could translate into stronger consumer spending after a weak first quarter, but that more positive picture is now being clouded by tariff tensions and the weakening economic environment, both of which are seriously weighing on confidence.

EU industrial production appeared to be bottoming out in the first quarter

Eurozone manufacturing is lagging behind the rest of the world

Is long-term structural growth in industrial production now only reserved for emerging economies?

European industry has lagged behind that of the US over the past two years. At the start of the year, industrial production in the EU and the eurozone was around 5% lower than two years ago, while it has remained stable in the US. The war in Ukraine and the subsequent energy crisis have clearly left their mark. As a global industrial powerhouse, China also recorded 13% production growth in that same period.

Is structural growth in industrial production reserved only for emerging economies in the long run? They've seen industrial production double in the last 20 years; production in developed economies has only stagnated.

Eurozone industry loses ground to rest of the world

Production level manufacturing industry, Jan-23 = 100, 3 months moving average

Tariffs will put a hold to growing US demand for EU goods

As long as tariffs remain in place and uncertainty about further and higher levies lingers, the US will probably no longer be a growth market for European goods. It’s almost impossible to fully quantify the full impact of the tariff tsunami. Focusing on the direct and indirect trade impact, 20% tariffs could shave off 0.3 percentage points of eurozone GDP growth over the next two years. Eurozone exports to the US increased materially before tariff announcements were made, and the most immediate effect will be the reversal of frontloading as the first tariffs take effect. This will bring extra downward pressure on industrial production in the second quarter.

The tariff impact will deal quite a blow to the more exposed manufacturing industries, desperate to reverse stagnating trends. The US is the largest export market for European products, with a share of 20% of extra-EU trade. This is 22% for Germany and Italy, and 46% for Ireland. France and the Netherlands are less exposed, with a 16% US share, as is Spain with 13%.

Pharma most exposed to US tariffs, but machines, vehicles, and chemicals also greatly affected

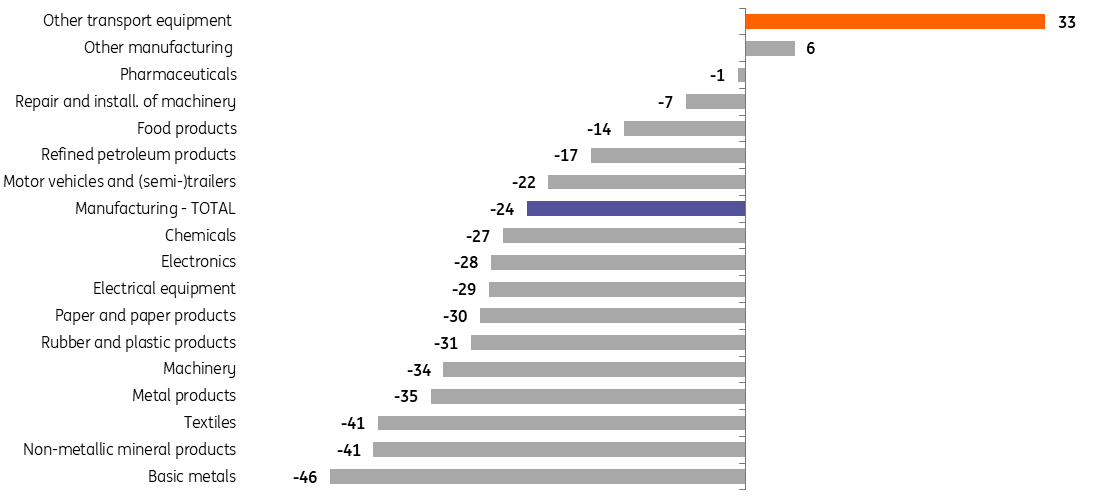

While the pharmaceutical sector was among the best-performing European industries in 2024, the outlook for this year is much less rosy. Trump specifically mentioned pharmaceuticals (along with semiconductors) as products being excluded from general tariffs, but they'll soon be subject to specific tariffs. Should this come to pass, producers of pharmaceuticals and other medicinal products will be hard hit. They accounted for 23% of more than €530bn that the EU exported to the US in 2024. This is slightly less than the 26% accounted for by machinery and equipment; the US share of total EU exports is a whopping 38% for pharmaceuticals, compared to an average of around 20% for machinery and other large product groups, such as road vehicles and chemicals.

There are also significant differences in trade exposure among member countries and sectors. Ireland and Germany are the most exposed to US tariffs on pharmaceuticals. Other nations with strong chemical and pharmaceutical sectors, such as Ireland and Belgium, or those with robust machinery and transport sectors like Slovakia and Germany, have the highest trade exposure. Ireland and Belgium's overall exports to the US are particularly high at 10.1% and 5.6% of their GDP respectively, compared to the overall EU export exposure of 2.9% of GDP.

Machinery, equipment, and pharmaceuticals make up nearly half of EU exports to the US

Shares of product categories in EU exports to US, 2024

Trade resilience results in both positives and negatives

On a more positive note, international trade has often shown resilience. In contrast to the direct effect of less trade with the US, there is a good chance that European exporters could be successful in shifting part of their trade from the US to other countries.

The EU is actively pursuing new trade agreements and partnerships with countries such as Mexico, Chile, Switzerland, Malaysia and the Mercosur states. In the longer term, this could provide some counterbalance to the new trade obstacles, and in turn, we could see the longer-lasting effects proving limited.

The large tariff differences will also make Europe a relatively cheap alternative to China for American importers. Despite the limited overlap between European and Chinese exports to the US, this could boost goods exports to the US, as the EU appears competitive in some product groups that match. But the escalation of the trade war between the US and China will also have a negative effect on EU manufacturing as China seeks markets outside the US for its state-supported exports. The outcome of these developments is difficult to predict, if only because of the constantly changing trading conditions.

Mood among producers cleared up slightly but remains subdued

Despite all the unrest, the mood among European producers has improved a bit since December. Production in particular seems to be holding up better than expected, though this is partly due to the elimination of backlogs.

General uncertainty over market conditions won't fade quickly

In April, the manufacturing output PMI rose to the highest level in almost three years (51.2), measured shortly after the 90-day reprieve of the reciprocal US tariffs. Announcements of substantially higher European defence spending and large German government investments were positive for sentiment, although the foundation is shaky as new orders continue to contract. European policymakers seem committed to taking action and supporting the manufacturing industry, but the general uncertainty over market conditions will not fade anytime soon.

In April, producer confidence was by far the lowest in Germany according to Eurostat. Confidence was 19ppt below its 10-year average. Among the largest manufacturing countries in the EU, confidence was relatively high in Spain, France, Poland and the Netherlands, with a negative deviation of 3.4 or less. Manufacturers in these countries have been relatively optimistic for some time due to growth in subsectors like pharma in Spain, France and the Netherlands, and chemicals, electronics and other transport equipment in Poland.

Tariff tensions halt cautious return of optimism among EU producers

Industrial confidence indicator

High stocks, low orders and uncertainty weigh on production levels

Poorly filled order books and high inventories are still depressing activity for the time being. The trade war makes any significant production growth for the first half of this year highly doubtful – that is, unless frontloading takes place again ahead of a potential tariff increase to 20% in July.

But given the current trade chaos, July seems a distant future for now. The picture may change somewhat in the second half of the year, if the trade storm subsides and European producers and consumers can look ahead with more confidence. We probably have to wait until 2026 for a substantial increase in industrial production due to government investments in infrastructure and defence. In the meantime, uncertainty over trade barriers remains a major disruptive factor for confidence and investment.

EU manufacturers still rate stocks as too high, while orders are low

Assessment of order-books and current level of stocks of finished products by manufacturers, EU-27

High-tech production remained stable in 2024, while mid-tech shrank considerably

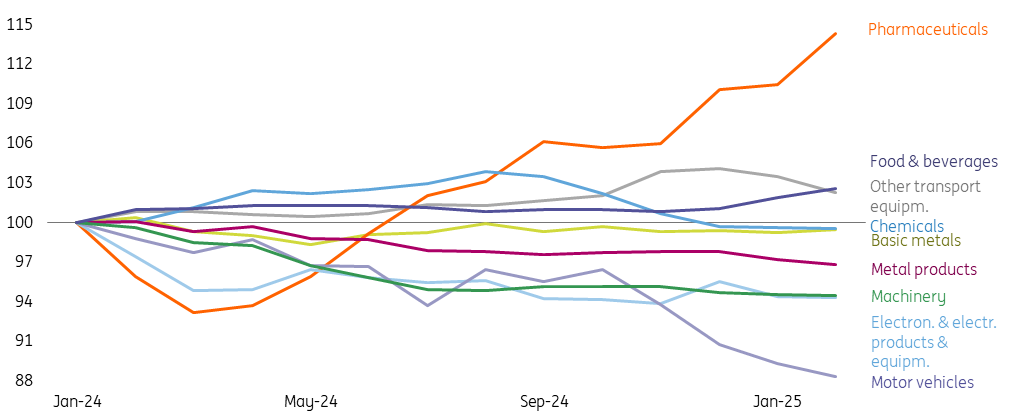

Differences between industries and countries remain substantial. In February, the output of high-tech industries – pharma, electronics and air and spacecraft – was slightly above the level of two years earlier (+0.3%), while mid-tech industries – electrical products, machinery and transport equipment – produced 9% less. By climbing the technological production ladder, China now competes fiercely with European mid-tech, in addition to the basic industry. Motor vehicles, machinery and electrical equipment were hit hard in 2024. As buyers of semi-finished products, they took the metalworkers and plastics processors with them in their fall.

Pharma and food the only growing subsectors at the start of 2025

Production level manufacturing industry, Jan-24 = 100, 3 months moving average

Spain and Poland remain stable as Germany and Italy lag behind

The intra-sectoral differences also result in a noticeable divergence in industrial production development between countries. In the space of two years, Spain and Poland have managed to maintain quite stable production levels, while Germany, Italy and the Netherlands have experienced a steady decline. Among the large EU industrial countries, Poland has been growing structurally faster than the European average due to the catching-up effect.

Polish and Spanish production has managed to stay afloat in the past two years due to a relatively large food industry – a sector which is less sensitive to the economic cycle. The machinery industry in these countries is also relatively small, as is the case in France, another recent industrial outperformer. As a result, the pressure on production there has been less pronounced than in other countries.

Over the past two years, the overcapacity resulting from economic stagnation, increasing competition from China and reduced export demand from China have weakened demand for European machinery. The machine industry is strongly overrepresented in the two EU countries with the largest manufacturing industry, Germany and Italy, both of which have seen the largest production decline. Germany also has a large car industry and Italy a large textile and clothing industry, two sectors which have also been deeply impacted by the events of the last couple of years.

Large differences in production development between EU countries

Production level manufacturing industry, Jan-23 = 100, 3 months moving average

Overcapacity of energy-intensive industries set to worsen

For energy-intensive industries, difficult conditions remain a long-term issue. European energy prices remain elevated; they're at least four to six times higher than in the US for gas and two to three times higher for electricity. The proposed measures on affordable energy from the European Commission could yield results in both the short and long term, but obstacles still exist that could limit their overall impact, and immediate energy supply boosts are hard to enforce.

A growing number of chemical and steelworks plants have been shut down across Europe recently. Overcapacity adds to the deteriorating competitiveness of European basic industries. Global petrochemical capacity rose by some 50% in five years, with China continuing to drive capacity additions. Global overcapacity in steel has increased to a level that exceeds the total steel production of OECD countries, and US tariffs will likely further deteriorate the situation for EU basic industries due to an increased supply of chemicals and steel directed to the European Single Market in an environment of high energy prices and weak demand. As a result, an increasing number of basic industrial companies are shifting investments away from European soil.

Gas price in EU structurally much higher than in US

Ratio between gas price Europe (Dutch TTF) and US (Henry Hub), in MMBTU

Production of investment goods and semi-finished products remain under pressure in 2025

In addition to the direct negative demand effect of US import tariffs, increased uncertainty surrounding trade barriers is causing companies to be more cautious about investments. The resulting weakness of the global economy is yet another indirect effect of this, and in turn, the demand for European investment goods will come under further pressure despite lower long-term interest rates.

China is now a serious contender against traditional European mid-tech strongholds

Manufacturers of machinery, electrical equipment and motor vehicles have seen the largest decline in production in 2024. European car sales were down approximately 18% relative to 2019. The reduced replacement of company cars during the pandemic and rapidly growing competition from new Chinese brands will prove major tests for European carmakers. And they are not the only ones being tested; the order books of EU producers of machines and electronic and electrical products are at levels only comparable to deep recession periods. Rapid technological advances and large-scale government investments make China a serious contender in traditional European mid-tech strongholds.

Manufacturers of metal and plastic semi-finished products do not see the prospects improving much for the time being. When stocks are no longer sufficient, they can expect a positive bullwhip effect in a rising market. The substantial increase in production that this entails isn't yet clear, and isn't expected to occur until 2026 at the earliest. Meanwhile, the European building material industry is beginning to rebound after experiencing a significant decline. We think this recovery will persist as the EU housing market steadily improves, given that US import tariffs have a minimal impact on most European building material suppliers.

EU exports to China lagged far behind EU imports from China in the last decennium

EU-27 exports to and imports from China per year, 2014 = 100

Investments to support production growth from 2026 onwards

Aside from potentially lower policy rates, two key factors could offset some of the impact of the trade war on the economy and manufacturing.

Firstly, long-awaited additional German investments that aim for stronger defence and infrastructure improvements – including transport, (clean) energy and digitisation – could support EU manufacturing demand from 2026 onwards.

Secondly, the European Commission’s plan to ‘rearm’ Europe and to unlock extra defence spending is set to boost industrial growth, though it remains uncertain as to whether the €800bn mentioned by the Commission will be fulfilled. According to the plan, this could potentially unlock €650bn if countries allocate an extra 1.5% of GDP to defence, raising average EU defence spending to 3.5% of GDP. In addition to the planned €150 billion in joint European defence loans, the European Commission is also considering shifting the existing €392 billion in the 'cohesion fund' for regional development to strengthening the defence capabilities of member states.

Defence spending rises steeply

EU defence spending has already been on the rise in recent years. In just four years, it increased by more than 30% to 1.8% of GDP. There's limited upside here for manufacturing, as a relatively large share of the goods will be imported.

Since the Russian invasion of Ukraine, roughly 80% of the EU’s defence procurement has gone to non-EU firms. Europe-wide, imports of major arms have increased by 155% between the 2015-2019 and 2020-2024 periods. One reason for this is limited European production capacity. The market for military equipment is also fragmented, lacking unified European standards and procurements, relying instead on national ones.

An increased drive for action could lead to a faster build-up in production capacity

Harmonised EU defence strategies and collective investments have to be rolled out and procurement contracts have to be signed before defence output can really soar. The increased drive for action resulting from greater awareness of international threats and the lack of confidence in once steady continental partnerships could lead to a faster build-up of production capacity. The current long-term industrial overcapacity and collective willingness to invest can also serve as a catalyst here.

Scaling up defence production capacity comes with challenges

However, tight labour markets make rapidly scaling up EU defence production capacity a challenge, especially in Northern Europe. Potential new distortions in supply chains due to trade disturbances could also add yet another layer of complexity. The European defence industry is divided among industrial subsectors, like the manufacturing of metalworks (ammunition, weapons) and other transport equipment (fighter planes, naval vessels, submarines, tanks, among others). The latter has been one of the few growing EU industrial subsectors in recent years, second only to pharma. Next to higher defence spending, persistent aeroplane production growth (due to the large backlogs resulting from supply chain disruptions) was one of the main drivers here.

Making better use of dual-use technologies that can be used for both civilian and military applications could help ramp up manufacturing capacity at companies that previously focused exclusively on the civilian market. This could help solve the problem of low capacity utilisation caused by the long period of stagnation, effectively killing two birds with one stone.

A growing number of European manufacturers see business opportunities in military products. Dutch civilian manufacturer VDL wants to use its former car factory for the production of defence equipment, and German tank manufacturer Rheinmetall is interested in production facilities that Volkswagen may consider selling. French-German KNDS recently bought a wagon factory from Alstom to scale up the production of tanks. Italian company Leonardo is set to collaborate with the Turkish Baykar for the development of drones, an indispensable weapon in which many companies see growth opportunities.

The EU defence industry is largely concentrated in Germany, France and Italy, and the relatively small size of the largest EU defence companies could hamper rapid scaling up. None of them are among the top 10 players globally. Arms revenues of Airbus and Leonardo amounted to almost 13bn and 12.5bn in 2023, whereas the largest US defence company, Lockheed-Martin, earned over 60bn in arms; this figure stood at 30bn for the largest UK player, BAE Systems.

EU defence cluster partly adds to already well-filled order books in other transport equipment subsector

Assessment of order-book levels by manufacturers, EU-27

Substantial stimulus from defence growth, but not a gamechanger for manufacturing

In the longer term, the European defence industry could see a sharp increase in production. This would require a further increase in military spending and a scaling up of production capacity, so that 50% of purchases can be made within the EU.

NATO estimates that about two-thirds of additional eurozone defence spending last year went to equipment investment. Assuming that this share stays the same, total defence production in EU member states spending on defence equipment produced by member states could rise as much as five times by 2030. This could increase the share of defence output in industrial production from around 0.5% in 2024 to 2.5% in 2030. It may not be the game-changer that revitalises the European industry, but it would certainly contribute to a long-awaited reboot.

So, we might be starting to see some light at the end of the tunnel for European manufacturing – but we're still unclear as to when that end could feasibly be reached. What we do know is that 2025 will be a year of transition with great uncertainty. A large industrial rebound in 2025 seems unlikely, although the result of earlier investments could materialise, and the second half of the year will probably be better than the first. In the meantime, many changes for the better have been set in motion to make EU manufacturing ‘great again’ in 2026.

Weak growth in 2025, improvement in 2026

Realisation and forecast of industrial production growth (excl. construction)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article