How the EU’s new food and agri Vision could reignite the sustainability target debate

The EU Commission will soon lay out its ambitions on agriculture and food in a long-awaited Vision on the sector. It’s expected that some sustainability efforts will lose out to other priorities in the short term, which will affect food manufacturers – and could also reignite boardroom discussions on the feasibility of corporate sustainability targets

Farmers and food security at the top of the list

President of the European Commission Ursula von der Leyen has promised that her new Commission will publish its ‘Vision on Agriculture and Food’ in its first 100 days in office, expected on 19 February. In the lead here is Christophe Hansen, the Commissioner for Agriculture and Food, together with Raffaele Fitto, whose portfolio includes competitiveness of the food and farming sector and the regional economy.

This signals a shift from to the Farm to Fork Strategy from the previous Commission, which was part of the broader Green Deal led by Frans Timmermans. Some of the priorities of the Vision will also be different due to shifts in the (geo)political landscape. We expect the document to be more farmer-centric and to focus more heavily on maintaining food security in the short term than the Farm to Fork Strategy.

Four topics that food and beverage manufacturers will be looking out for

Since the Vision will set out the direction for EU agricultural and food policy in the upcoming years, it’s a very relevant document for food manufacturers. In this article we provide a preview on four relevant policy areas that will be featured in the Vision: 1) the position of farmers, 2) sustainability benchmarking, 3) measures to reduce greenhouse gas emissions, and 4) demand side policies.

We’ve based this preview on:

- The policy recommendations that the Commission has received so far, most importantly the final report from the Strategic Dialogue on Agriculture and Food.

- Comments made by members from the new Commission, for example during their hearings and the EU’s Agri Food Days, and the actions they’ve taken so far.

- Various conversations with industry experts.

For each of the four topics, we highlight why they’re relevant, what the Commission’s plans and options are and what those would imply for food manufacturers.

Improving the position of farmers in the value chain, a recurring theme

This is very much a recurring topic in EU politics, and politicians continue to emphasise the need for fairer incomes for farmers as well as a stronger position in the value chain. Given that food manufacturers are the main buyers of agricultural products, they may also be influenced by any policies related to farmer incomes and the position of farmers.

Improving farmers' positioning in negotiations is a key aim for the current Commission. Firstly, more support for cooperatives and producer organisations will ensure that farmers can unite themselves. Amendments to the Common Organisation of the Markets (CMO) regulation have also been proposed, including making it obligatory to use written contracts and introducing additional rules against unfair trading practices, such as late payments.

Policy proposals are not a silver bullet

We believe that additional steps taken by the Commission can help to shield farmers from excesses in the market – but these policy proposals are not a silver bullet. Most farmers remain price takers regardless of what’s happening with regulation.

Still, there are other good reasons for food manufacturers to be mindful of the position of farmers. The volatility in income that many farmers experience – combined with the increasing exposure to climate-related risks and the need to invest in making their farms future proof – does affect food processors. A lack of perspective for farmers could reduce supply and lead to higher prices, which is most worrying for companies that depend on a ‘local’ farm base (like meat, dairy and sugar processors). In many cases, food manufacturers are still able to circumvent supply shortages through keeping inventories or by resorting to alternative suppliers. But in the mid to long term, the ongoing decline in farm numbers highlights the need to invest in a reliable supplier base.

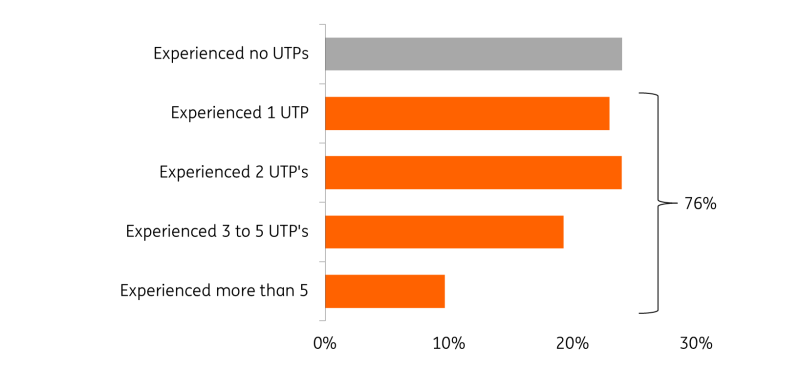

Three out of four EU farmers have experienced unfair trading practices

Percentage of respondents that have experienced UTPs during last year

EU-wide benchmarking of farmers: no reward, no support, no data

The current Common Agricultural Policy (CAP) that runs until 2027 contains a range of sustainability-linked incentives, but these require better monitoring at farm level to be effective. One issue raised by the Strategic Dialogue is that the lack of a standardised and harmonised methodology when it comes to assessing sustainability hampers progress on reaching sustainability objectives. It advises the launch of an EU-wide benchmarking system in agriculture, the harmonising of standards, setting baseline targets and implementing legislation which ensures enforcement across countries.

For food manufacturers, such a push would be beneficial; they often have a range of sustainability targets varying from reducing emissions to improving biodiversity, but encounter difficulties when collecting information from their suppliers.

Gathering the right data takes time and effort – and that limits how far the Commission can go with rolling out EU-wide benchmarks

We think it seems unlikely that the Commission will follow up on rolling out EU wide benchmarking, mainly because pushing for a benchmarking system for all farms in the EU is at odds with the Commission’s promise to simplify rules to reduce the administrative burden. But if they do, the only way to gain farmer support is by providing meaningful reward for their efforts since gathering the right data takes time and energy.

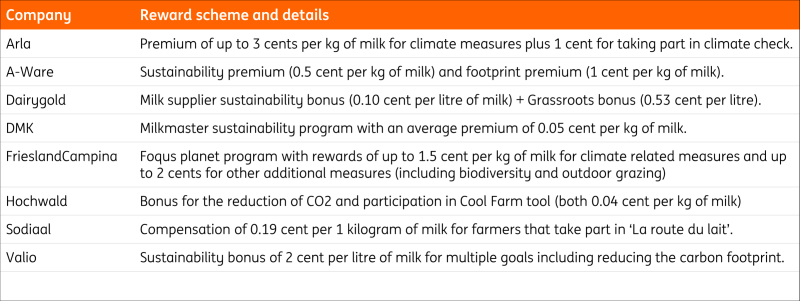

It's also useful for food manufacturers when more standardised farm level data on sustainable practices is available. That’s why some food companies, like large dairy producers, already have their own bespoke systems in place. In many cases, these company schemes feature a reward for farmers to take part. But there are also examples of public monitoring systems covering multiple subsectors, such as the French CAP2er. Any ideas being put forward in the Vision on sustainability benchmarking should provide direction on how existing schemes will be verified and recognised.

Sustainability related reward schemes are quite common among EU dairy companies

Pressure builds to pick up efforts to reduce emissions in agriculture

Agriculture represents 13% of all greenhouse gas emissions in the EU, but the reduction of emissions is lagging behind that of many other sectors. Currently, there is no specific EU reduction target for the agricultural sector, although some countries like Ireland and Denmark do have targets. The course that the EU is taking to reduce agricultural emissions influences food manufacturers because they often have corporate reduction targets and the majority of the emissions in their supply chain happen on farms.

The Strategic Dialogue advises providing more clarity on the general pathway for agriculture and the reduction goals for different types of agriculture at EU level. The Commission could also push countries to set reduction targets at national level, as well as stimulating incentives and standard setting to ensure measures such as higher technology uptake, more renewable energy on farms and increase in precision farming are implemented. It'll also be interesting to see whether the proposal from the Strategic Dialogue to set up a Agri-Food Just Transition Fund will be embedded in the forthcoming Vision. This Fund is meant to finance changes in business models. Finally, the introduction of an Emission Trading Scheme (ETS) for agriculture is an option.

More clarity on reduction targets for agriculture provides food makers with a better baseline to use in their own plans and incentives to farmers help to reduce emissions in their supply chain. While the Vision might contain a bit more guidance on reduction targets for agriculture, we think that an ETS for agriculture is definitely not part of the plan. In case an Agri-Food Just Transition Fund is set up, it remains to be seen whether it will have the size to be a game changer. Competition for additional EU funding is very fierce and calls to invest more in competitiveness and defence seem to get priority.

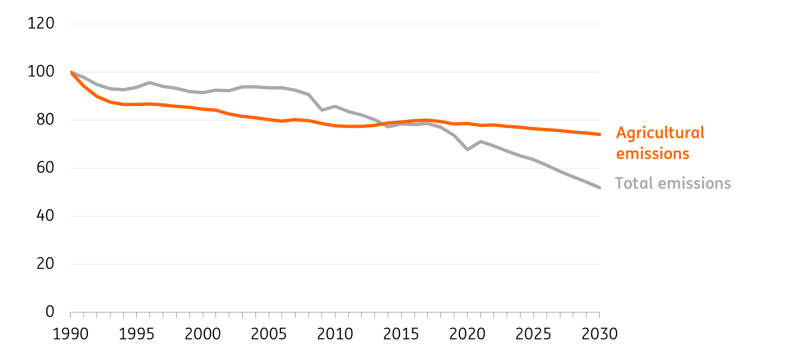

Agricultural emissions in the EU are falling at a slower pace compared to total emissions

Index 1990=100

Little appetite to use policy to steer consumer demand – reassuring for some food makers, disappointing for others

In the Strategic Dialogue, it's noted that "to keep farming within planetary boundaries, food consumption patterns need to change", and the benefits of steering demand for the sake of health and well-being are also mentioned.

Policy and regulation can drive changes in demand, and the shift towards electric cars is probably the best example here. In food, such interventions on the demand side are either absent or relatively soft. Interventions often don’t go further than providing consumers with information, for example through dietary guidelines. The advice from the Strategic Dialogue is to do more, like setting a strategy for plant based products and using fiscal tools to encourage more sustainable consumption patterns. Policymakers growing more active towards the demand-side would prove highly relevent for food makers – it would create opportunities for some, and risks for others.

However, the EU Commission's leverage on consumer demand is quite limited compared to its influence on supply. Many of the policy options that could increase demand for some products and decrease demand for others rest with national governments. This includes the introduction of certain price signals, such as differentiating VAT rates or higher taxes on products that have a negative health impact or a high environmental impact.

We don't expect any far-reaching ambitions on the demand side

Aside from a call out to the industry to promote demand for sustainable products, we don’t expect any far-reaching ambitions on the demand side. Commissioner Hansen said during his hearing that it would be “dangerous” for the EU to “impose top-down who needs to eat what”, which clearly shows that the appetite to take action is low within his DG Agri.

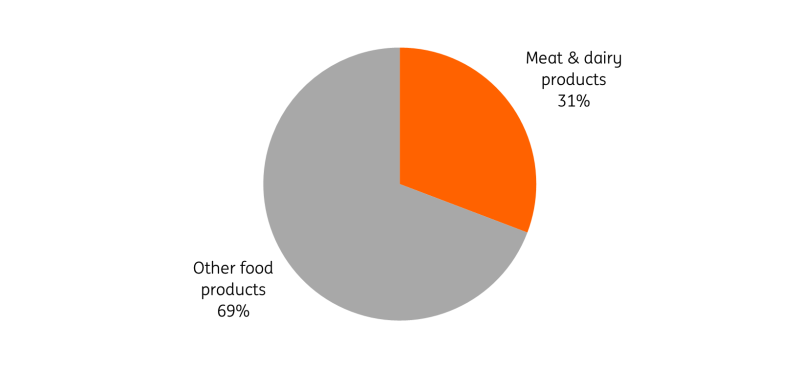

Let's not forget the economy reality here that meat and dairy represent almost a third of total food exports

There is also no strong support on the national level. Many recently formed national governments aren’t keen on demand-side policies and instruments like meat taxes. Denmark, with its recently introduced climate tax on farms, is an exception rather than the rule in this instance. Let's also not forget the economic reality here: meat and dairy form a large part of people's shopping baskets and represent almost a third of total food exports. We consider big policy proposals aimed at increasing or decreasing demand for certain products very unlikely. While that’s reassuring for incumbents in subsectors like the meat and dairy industry, it will continue to feel like an uphill battle for companies and startups active in plant-based, cultured meat and precision fermentation.

Meat and dairy products represent a large chunk of EU food exports

Share in total exports, Q2 2024

EU Vision to spark internal debate on sustainability targets at food manufacturers

Ambitions were high during the previous Commission – but in the end, many policy proposals didn’t make it to the finish line or only made it in a watered down version. Due to its political colour, the new Commission is less outspoken on environmental objectives and more pragmatic in its ambitions and promises. While general climate targets won’t change, in the short term sustainability efforts are likely to lose steam as other priorities such as supporting economic growth, maintaining a high level of food security and additional spending on defence gain momentum.

That might be comforting for many food companies in the short-term as it limits the speed with which they have to change their businesses, but it makes it more difficult to achieve longer term targets on GHG emissions, biodiversity or other environmental indicators. For business leaders, it means that the Vision will likely bring the debate on the gap between their corporate ambitions and reality back to the table.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article