ESG in FX: The current state of play

Environmental, Social and Governance (ESG) challenges have become a dominant theme in global financial markets. Yet in the context of foreign exchange, the points of contact with ESG are still very much evolving. We take a look at where ESG has found a footing in FX, where it can grow, and the roles to be played by both the public and private sectors

The E.

ESG investing has clearly come a long way over the last decade. Some estimates expect that there will be as much as $40tn in ESG-linked assets under management by the end of this year. Strong demand for ESG-linked instruments is seeing new financial market products being created all the time. Yet softening the lens away from the investment side and looking at the role of ESG in the broader FX market reveals a very different set of touch points.

We will discuss the development of ESG-linked FX products a little later, but when it comes to environmental considerations and FX, the focus is probably drawn to two areas: i) the greening of public and private sector assets and ii) the macro FX implications from the energy transition.

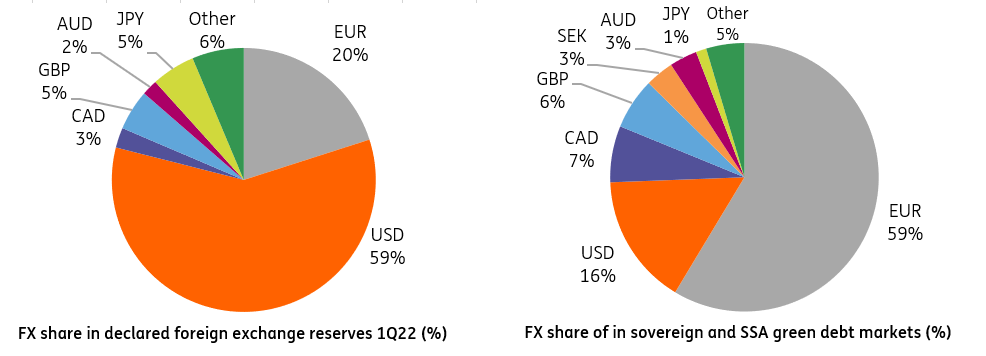

On the macro side, the war in Ukraine has sharpened the focus on the key commodities required for the energy transition, and their suppliers. Demand for the likes of aluminium, cobalt, copper, lithium, nickel and silver will provide some long-term support to the currencies of their key exporters. We have provided some coverage on this broad topic elsewhere. In this section, we want to focus on the greening of public sector assets and in particular the greening of the world’s $12tn pool of foreign exchange reserves.

One article catching our eye recently was a column written by senior economists and advisors at the European Central Bank looking at the role of monetary policy in the green transition. The connection with FX comes with one of the ‘proactive measures’ a central bank can take – the greening of FX reserves.

Possible central bank actions to respond to climate change

What effect could the greening of central bank FX reserves have on the FX market? The Bank of International Settlements released an important paper on this subject in 2020, which looked at wrapping sustainability into central banks' conventional FX reserve management targets of liquidity, safety and return. The report concluded that while the liquidity considerations of green bonds did pose a constraint, the safety and return of green bonds did not.

Issues to be considered here could be the following: how quickly does improving green bond liquidity allow FX reserve managers to go green and how quickly will green bond markets develop in currencies outside of the euro and the dollar?

The Czech National Bank (CNB) is an interesting case study here. It is one of the few central banks to spell out in its annual report what proportion of international reserves it allocates towards ESG – 3.7% in 2021 for reference. With relatively large FX reserves (peaking at 70% of GDP recently), perhaps the CNB more than most could put the investment tranche of its FX reserves to work in the ESG space.

Yet recent changes at the CNB board level have seen the koruna come under pressure and the CNB quickly lose 15% of FX reserves over the last couple of months – emphasising the importance of liquidity. The topic of the liquidity of FX reserves will therefore be a key constraint to a more wholesale shift into green bonds.

In addition, as the BIS paper also concludes, legal and governance frameworks will play a key role in the greening of FX reserves. For example, Switzerland has a huge FX reserve stockpile and could be a further big candidate for greening its reserve portfolio. The Swiss National Bank does undertake exclusionary screening in its large equity and corporate debt book against companies with controversial businesses – e.g. arms manufacturers. But unless its reserve management mandate is altered more actively towards green initiatives – currently FX reserves are held purely for monetary purposes – it is hard to see a significant shift towards greener assets in policy portfolios such as FX reserves.

Where there has been more progress is in the area of non-monetary central bank portfolios (e.g. own account and pension funds) and also domestic quantitative easing (QE) schemes. On the former, the ECB has about 3.5% of its own fund portfolio in green bonds. And while the ECB does not specify what proportion of its various QE schemes are in green bonds, a market-neutral weight would again be something like 3% when looking across both the public and private bond sector. That said, we assume the market-neutral weighting for green bonds will be rising. Sovereign and SSA bonds offer the most clearly-defined greenium, or funding advantage of issuers, despite some discrepancies. For reference as well, our credit strategy team tells us that currently, 15% of the ECB's CSPP bond holdings are green.

One final point here, green bonds are largely a euro- and dollar-denominated proposition. Would a shift to more green bonds in FX portfolios lead to even higher shares in allocations towards the dollar and especially towards the euro? We’ll need to keep tabs on green bond supply trends for developments here, though the default scenario is probably one of FX reserve compositions being unaffected by the greening of FX reserves.

Currency shares in FX reserves differ from those in sovereign and SSA green debt market

The S and the G.

When it comes to social and governance considerations here, our initial thoughts focus on two areas: i) the FX global code (FXGC) and ii) the weightings towards ESG, especially governance, used by the rating agencies in their sovereign reviews.

Introduced in 2017 and updated in 2021, the FXGC seeks to promote a ‘robust, fair, liquid, open and appropriately transparent foreign exchange market’. The top two of its six leading principles are ethics and governance. The code’s development arose out of the FX fixing scandals of the last decade and its adherence has effectively become a necessary condition to offer an FX service to clients.

FXGC adherence could become a more important criterion for FX pricing

The sell-side take-up of the FXGC has been strong on the back of the need to demonstrate best-in-class ethics. The take-up from the buy-side has been less strong in that FX liquidity is not yet being rationed to those yet to sign up to the code. Commercial interests mean that this environment may not change in a hurry. But new conditions of volatility and reduced liquidity could increasingly mean that the sell-side becomes more selective as to whom they extend FX pricing – with FXGC adherence becoming an ever more important criterion.

Rating agencies have long used governance (especially the institutional framework) in their sovereign ratings. The focus is generally on domestic political stability, which can have a significant impact on the predictability of policymaking. This contributes to the risk premium of a given country and currency. The highest profile sovereign ratings story in the FX market over recent years was probably South Africa being downgraded to junk status back in 2017. The rand saw large outflows as its local currency sovereign bonds were removed from investment grade bond benchmarks.

ESG ratings scores typically feed into the structural quantitative rating of a country, along with allowing for a subjective adjustment of ratings in certain country-specific situations, such as times of elevated political instability. Our EM sovereign ratings analyst, James Wilson, notes that while governance has typically played a strong role in emerging market country ratings, environmental issues are becoming increasingly important. Be it a country’s dependence on fossil fuel exports and suffering stranded assets through the energy transition or a country being more directly at risk from the physical impact of climate change – these environmental issues on the whole have seen far more discussion in the rating process in recent years given increasing client demand and evolving investor mandates.

This demand for ESG data and analysis will likely increase along with related market developments, including more issuance of sustainability-linked and green-focused sovereign bonds in developing nations. There have also been wider discussions in linking sustainability criteria to potential future sovereign debt restructurings – Belize, for example, last year implemented a debt-for-nature swap to cure its default while committing to implement measures to protect ocean biodiversity.

ESG products in the FX space

Financial market derivative products linked to ESG continue to evolve and as in other asset classes, those in the FX space typically involve two counterparties agreeing on ESG key performance indicators (KPIs). Should the client meet those KPIs (usually assessed annually by an independent third party such as an auditor) then the client would either secure a cheaper hedging cost on, for example, a strip of FX forwards or in some cases a cash rebate depending on the amount of FX hedging business done in a year – the latter effectively a loyalty scheme contingent on ESG goals being met.

Banks could offer FX pricing incentives to clients with better ESG ratings

A further scheme being looked at by some participants is the integration of ESG metrics into FX counter-party considerations. Those metrics could generate reductions for fee-linked products (e.g. FX algorithms) or indeed affect the pricing of a counterparty’s access to FX liquidity. This could see banks offering FX pricing incentives to clients with better ESG ratings and equally clients allocating business to banks based on the banks’ own ESG ratings.

Constraints to the further growth in some of these initiatives could be the lack of homogeneity in the KPI metrics, where each client requires their own specific ESG targets. Greater take-up in these products could require some move towards standardisation of ESG benchmarks, although the regulation of benchmarks in derivatives remains a minefield.

Another challenge in the FX space is that the industry works on fine margins, meaning that the scope for rebates and the financial incentives to meet ESG targets may not be as large as in some other asset classes or products.

A long way to go

Above we have highlighted several touch points between ESG and the FX industry. Undoubtedly there are many more and we would love to hear about them. Progress has been made, but a move to the next level probably requires an even greater push towards green assets in the public sector. Here, we should keep track of developments at the Network for Greening the Financial System – a body that released a seminal article on this subject in 2019.

Equally, the financial incentives have to be present in the private sector. The good news is that the FX industry is heading in this direction and the challenge will be how regulators can support this progress too. Expect a lot more transparency on this subject with the introduction of the European Commission’s Sustainable Finance Disclosures Regulation (SFDR) which comes into force at the start of 2023.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article