ECB cheat sheet: Half a gear down

Another well-telegraphed hike from the European Central Bank brings another tough challenge for the Governing Council and Christine Lagarde: committing to another move in September or switching to full data dependency. We think the second scenario looks more likely, which may be read as a modestly dovish surprise and could weigh on EUR/USD

Stressing the "higher for longer" to counter market rate cut speculation

A 25bp hike is a done deal. More relevant is what the European Central Bank will signal as its next steps. Given the surprisingly dovish remarks by some of its most hawkish members, a renewed commitment to future hikes – as we have seen in past meetings – seems unlikely. Switching to greater data dependency for the meeting ahead will be viewed as mildly dovish and could see markets nudge down hike expectations, which are close to fully discounting a further 25bp hike before the end of the year.

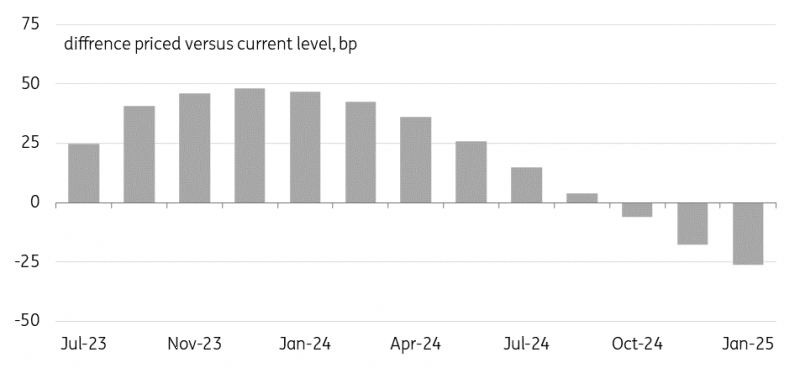

The ECB will be aware of that dilemma, and the risk is that it will seek to influence rate expectations further out, thereby manufacturing a (bearish) steepening of the front end. Currently, markets see the ECB cutting rates by around 75bp over the course of 2024. The challenge will be to overcome indications of a further softening macro backdrop as conveyed by today’s flash PMIs.

Markets see the ECB cutting rates 75bp over next year

One way to show determination would be to revive talk of quantitative tightening. Given that reinvestments from the Asset Purchase Programme have already ended, this would mean hinting at the possibility of outright sales. The obstacle to changing the guidance for reinvestments in the Pandemic Emergency Purchase Programme might be higher since they also serve as a backstop for sovereign spreads. Hints of quantitative tightening do not necessarily have to come at the press conference – but should the market reaction be deemed too dovish, the topic could be picked up in the typically active post-meeting commentary by officials.

Both the Federal Reserve and the ECB will not want to take any chances on inflation this week. They will both be wary of not giving the markets a premature bull steepening signal for broader yield curves just yet. Overall re-steepening of curves could be more gradual alongside evolving data this time around – that is, if nothing breaks before.

EUR/USD: Short-term valuation still offers room for correction

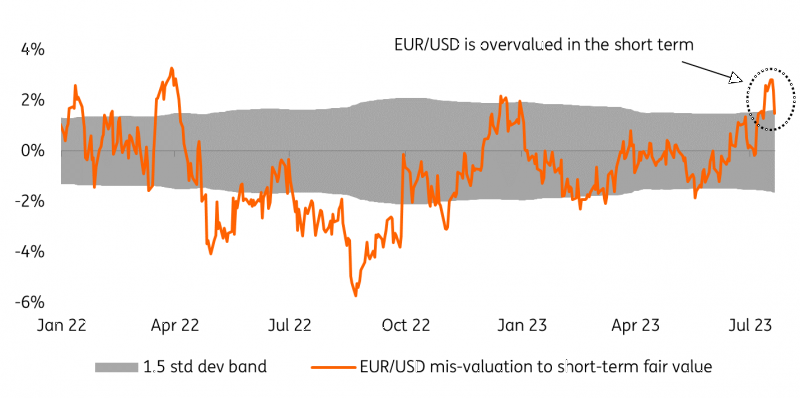

In the days following the large post-US CPI dollar drop, we had stressed how the short-term valuation picture for EUR/USD was looking quite stretched on the bullish side, having peaked above 3.0% at one point. One key input to our short-term fair value model is the 2-year USD-EUR swap rate gap, which at the time of writing has rewidened to near 130bp after a temporary contraction to 100bp after the US inflation report.

The latest bearish adjustment in EUR/USD has signalled a re-linking with that wider rate gap and allowed the short-term overvaluation to return to more sustainable levels of around 1.50%. That still leaves some room for another moderate EUR/USD correction this week, and we think the combined central bank messaging across the Atlantic is more likely to put some additional pressure on the pair than trigger a new rally.

EUR/USD isn't cheap

As discussed in our latest Fed preview, the FOMC may see little advantage in switching to more dovish rhetoric in spite of disinflation evidence as they hike again this week, and we expect Chair Jerome Powell to leave the door open for more tightening. As discussed here, the ECB's well-telegraphed 25bp increase should not – unlike recent instances – come with a commitment to another hike at the next meeting in September.

On balance, the Fed and ECB outcomes should be relatively similar. Markets, however, are barely pricing in any Fed hikes after July while for the ECB, they are pricing in 15bp by September and 20bp by December.

A default to data-dependency by ECB President Christine Lagarde could be interpreted as a moderately dovish signal for markets which have been accustomed to meeting-by-meeting guidance, and we expect EUR/USD downside risks to prevail given that a) the Fed decision may support the dollar, b) there is still room from a short-term valuation perspective for EUR/USD to correct lower.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article