Dutch pension reforms suddenly at risk

Dutch pension reforms are at risk due to a proposal in parliament that requires each fund to obtain a vote of approval from its participants before transitioning assets to the new system. This proposal could lead to a more gradual implementation of the reforms, delaying the unwinding of longer-dated fixed-rate receivers. Moreover, funds may become even more protective of their funding ratios until their transition date, potentially increasing the demand for fixed receivers in the near term

Proposal would require votes of approval before transitioning

Dutch pension funds were caught by surprise when one of the coalition parties filed a proposal that could radically impact the ongoing reforms. In essence, the reforms are a move from a Defined Benefits to a Defined Contributions model and funds would have until 2028 to implement these changes. The new system would be more future proof and thus practically all pension funds are preparing to transition their current assets. Roughly half of the assets under management aim to transition on 1 January 2026, the other half in 2027, whilst three smaller funds already transitioned this month.

The proposed amendment to the current rules would require each fund to pass a vote of approval by its participants before transitioning assets to the new system. A majority would be needed and the minimum participation rate would be 30%. If participants were to vote against the transition, then the current pot of assets of a fund would remain under the old system and only new contributions would fall under the Defined Contributions model. In effect, the impact of the reforms would take place more gradually (over multiple decades) and funds would need to run two pots of money in parallel.

The next touchpoint in Parliament on the proposal will be Tuesday 4 February, and a more in-depth debate is scheduled beginning of March, which should give us a better understanding of the position of other political parties on the proposal. The parties that have previously opposed the pension reforms have a majority in parliament, so the support could be broad enough to pass the amendment there. In the Senate, however, this is not the case, and thus passing the law there could turn into a hurdle. In addition, the minister responsible will first await advice from the Council of State and involve all stakeholders before taking a stance on the proposal.

Complexity of vote could mean funding ratio plays important role

The reforms are a contentious topic and thus getting a majority of pension fund participants to vote for approval will be challenging. A survey by Netspar suggests that only 26-41% would vote in favour of transitioning assets to the new system, whereby the phrasing of the referendum would make a big difference in the outcome. This same survey also suggests that the majority of people deem the reforms too complex for a referendum.

The outcome could rely heavily on the funding ratio at the time of the vote. Very simply put, participants are given the choice between fixed pension payments under the current system (Defined Benefits) and variable pension payments that depend on the participant’s portfolio returns (Defined Contributions). The risk is therefore transferred from the fund to the participant. For the new (more uncertain) system to be attractive to participants, the expected payments would have to be higher.

If we take ABP’s transition plans (largest fund with €500bn AUM) as an example, we can see that a funding ratio of 120% or higher would draw a compelling picture for participants to change to the new system. In this case, the expected pension payments would increase by 3.5% on transition. If, however, the funding ratio falls below 110%, then the benefits are less obvious. A funding ratio of below 101.5% would even trigger a cut in expected payments. One can imagine such a scenario would be unlikely to find a majority vote.

ABP transition plan illustrates complexity behind vote

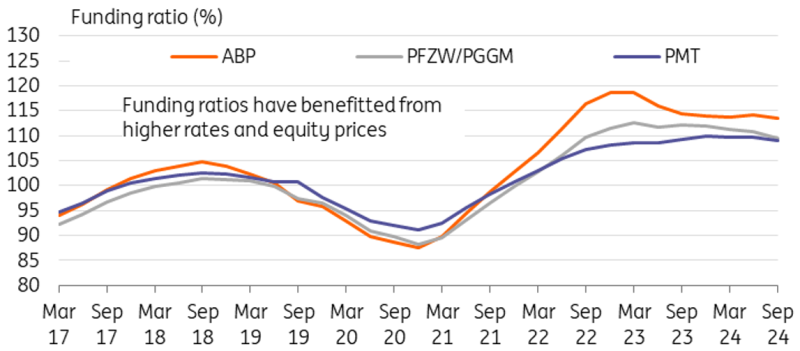

Funding ratios are exposed to plenty of downside risk

Funding ratios of the largest three pension funds have benefitted from higher rates and good performance of equities, but remain at risk for market shocks. The long duration of the funds’ liabilities means that funding ratios fall when interest rates decline. Should a downside interest rate shock come with a broader equity sell-off, funding ratios may well return closer to 100% or even below, as was often the case pre-Covid. This would reduce the chance of passing an approval vote.

Funding ratios of largest funds offer little headroom going into reforms

Given the importance of the funding ratio for a smooth transition, we foresee that the proposed changes could further increase the demand for fixed-rate receivers in the near term. As explained before, the new model reduces the demand for longer-dated receivers, those of 20 years or more. But in the meantime, pension funds may turn more risk-averse to ensure the funding ratio is in a good place on the date of transitioning.

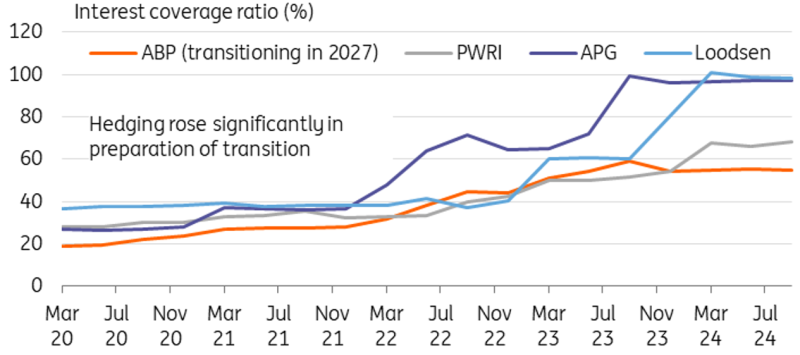

When looking at the first three funds that transitioned on 1 January 2025, we see that their interest rate hedging ratio increased significantly in the quarters leading to the transition. After the transition date, they communicated a recalibration of their hedges by reducing exposures to longer-dated bonds and swaps. As seen in the chart below, a fund like ABP has a relatively low-interest coverage ratio, so we wouldn’t exclude more demand for fixed receiver swaps if the proposal makes it through parliament.

Pension funds increased their hedges before transitioning on 1 January 2025

If funds fail to secure a majority approval, then the transition to a new system would be more gradual and thus the unwind of longer-dated fixed receivers would not be concentrated between now and 2028. As such, expect upward pressure on 30Y+ euro swap rates from the pension reforms to remain subdued until there is greater clarity on the proposal’s direction.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article