Dutch commercial real estate outlook: Growth ahead, but with limits

- 8 December 2025

- Real estate The Netherlands

Further growth in Dutch commercial real estate trade seems possible in 2026. However, it will likely be limited due to higher interest rates and construction costs, ongoing (geo)political uncertainty, and increasing demands from investors regarding sustainability and location

Dutch commercial real estate enters 2026 with cautious optimism. While investment opportunities remain, the market faces significant headwinds: elevated financing and construction costs, persistent geopolitical uncertainty, and rising investor demands for sustainability (compliance with climate and energy targets) and for prime locations with strong infrastructure and a deep talent pool. These factors are reshaping investment strategies and limiting the pace of expansion. Against this backdrop, interest rates will play an important role in determining market dynamics.

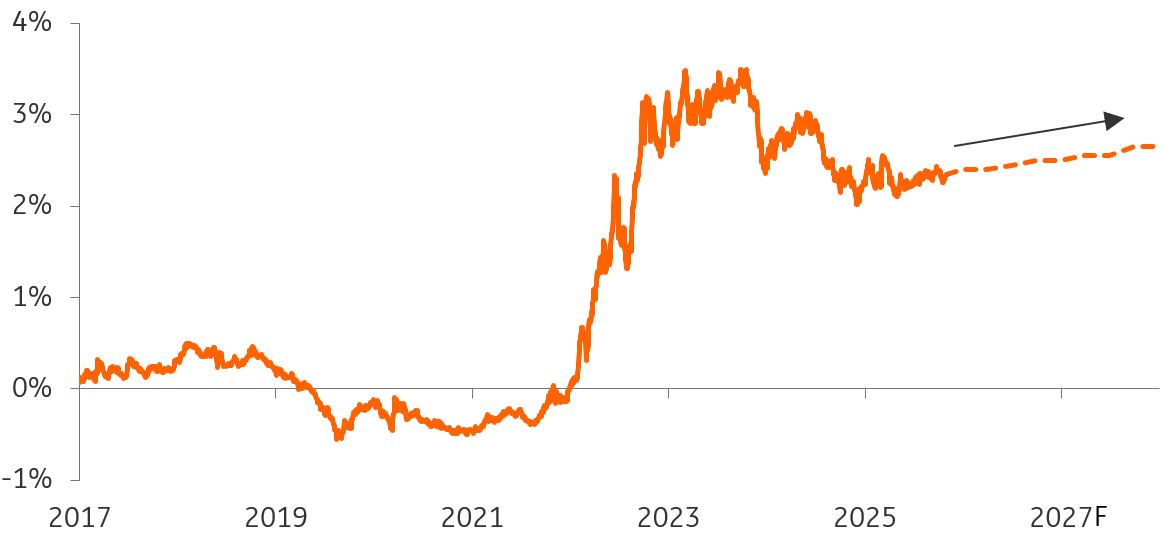

Slight increase in interest rates expected in 2026

We maintain our earlier forecast of a very modest rise in interest rates: a mild increase of 10 basis points in the 5-year IRS swap rate during 2026. This rate partly determines financing costs in the commercial real estate market and thus influences investor demand. The winding down of the European Central Bank's asset purchase programme and higher expected government spending by EU countries exert upward pressure on rates. However, the anticipated further decline in inflation toward the 2% target works in the opposite direction, largely offsetting this effect.

Slightly higher interest rates expected

Development of the 5-year IRS rate

Rates and costs well above pre-2021 levels

Compared to 2019 and 2021, interest rates are now much higher; for example, the 5-year IRS rate is currently about 230 basis points higher, resulting in increased financing costs for commercial real estate. Construction costs also surged a few years ago due to higher prices for building materials, while today it is mainly wage increases that continue to drive these costs upward.

Lower demand for commercial real estate

Higher financing and construction costs are dampening new-build investments, making financial feasibility increasingly challenging. This also affects investment demand for existing commercial properties; investors are more cautious about acquiring older assets that will soon require significant upgrades to meet user expectations and regulatory standards. To comply with Climate Agreement targets, stricter requirements on energy efficiency, renewable energy generation, and charging infrastructure will be needed. However, these investments are not always financially viable given the higher cost environment.

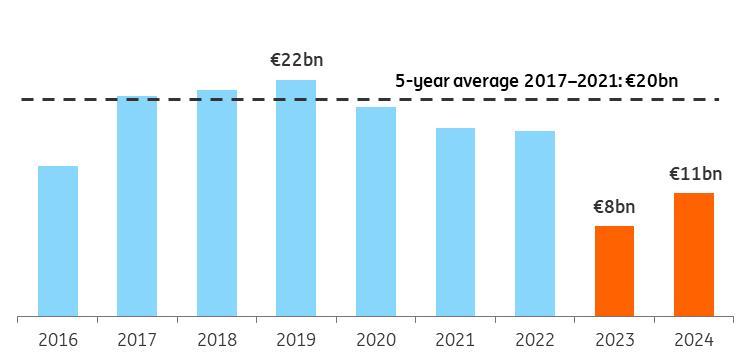

Investment volume far below 2019 peak

Investment volume in 2026 well below previous peak

Next year’s investment volume will likely fall far short of the 2019 peak. Even the average level seen between 2017 and 2021 appears out of reach. In addition to higher interest rates and construction costs, persistent (geo)political uncertainties are weighing on the market. Furthermore, the office sector (due to the shift towards remote work) and retail property market (due to the rise of e-commerce) face structurally lower user demand.

With this market outlook in mind, we now turn to the individual trends shaping rental housing, offices, retail, and logistics real estate.

New rental housing: Affordable housing mandates, higher costs reduce returns

The combination of rising construction and renovation costs and stricter affordability requirements for new builds is reducing investment returns on rental housing and putting pressure on new housing production. Planned legislation in 2026 stipulates that two-thirds of new homes must be affordable. This includes social rental homes with rents up to €900.07, mid-market rental homes with a maximum of €1,184.82 per month, and affordable owner-occupied homes priced up to €405,000 (2025 prices).

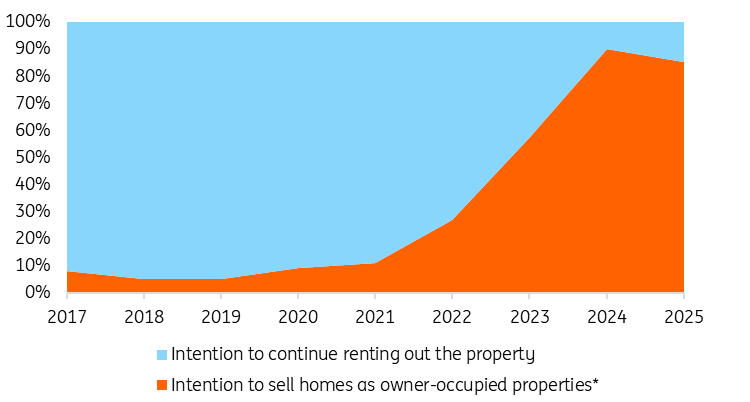

Existing rental housing: Sell-off continues

In the existing rental housing market, investors are mainly active in purchasing (older) rental properties with the aim of selling them on the owner-occupied market once the current tenant moves out. Continuing to rent out these homes is often financially less attractive than selling them, due to the sharp interest rate hikes in 2022, the introduction of fixed-term rental contracts as the standard, and the implementation of mid-market rent regulation. The expected further rise in home prices also plays a role.

Investors are currently buying rental homes mainly to sell them off

Share of investment volume in the existing rental housing market by investor intent

Offices: Prime green offices remain in demand

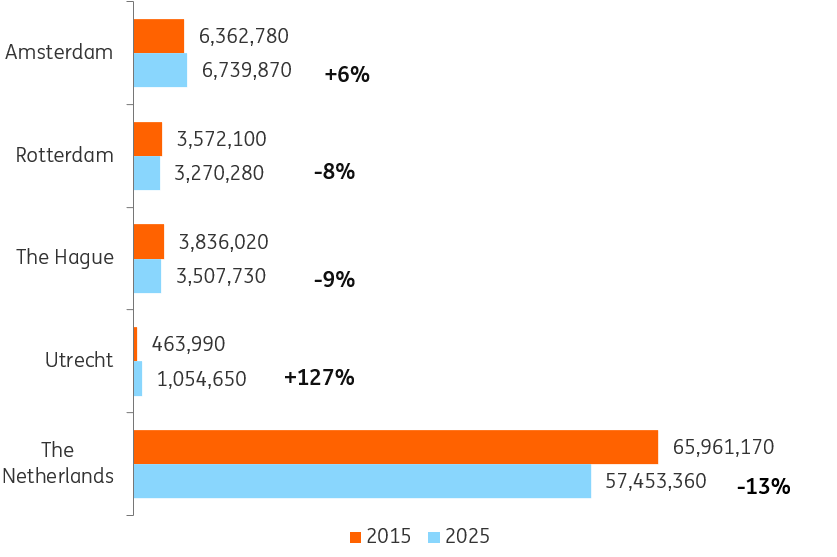

Overall, demand for office space is structurally declining due to the shift toward remote work. Companies will continue to focus on reducing office usage wherever possible. However, sustainability and location remain more important factors in office space decisions. In practice, large companies are shedding fewer square meters than they initially planned, suggesting that other considerations weigh more heavily. Interestingly, office stock in Amsterdam and Utrecht has increased over the past decade, contrary to the nationwide downward trend.

Decline in Dutch office supply, but not everywhere

Development office supply in m2

Retail (Non-Food): Shift to e-commerce continues

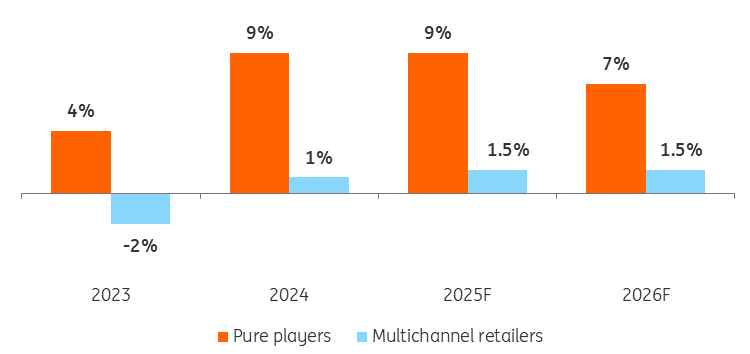

Demand for physical retail space should continue to decline due to retailer bankruptcies and the ongoing growth of e-commerce. Since 2023, revenue growth for pure online players has been significantly higher than for multichannel retailers, who combine physical stores with online sales. High-traffic retail locations remain attractive to retailers, creating room for rental growth in these areas. The Dutch retail property market is mainly driven by private investors with strong local market knowledge.

Pure online store revenue grows faster

Online revenue growth, year-on-year

Logistics real estate: Demand softens amid uncertainty

Current (geo)political uncertainties are reducing user demand for logistics properties, leading to rising vacancy rates. However, not all logistics locations are equal: vacancies are concentrated mainly in regions outside established logistics hotspots – often newer sites developed during the pandemic years when demand seemed limitless.

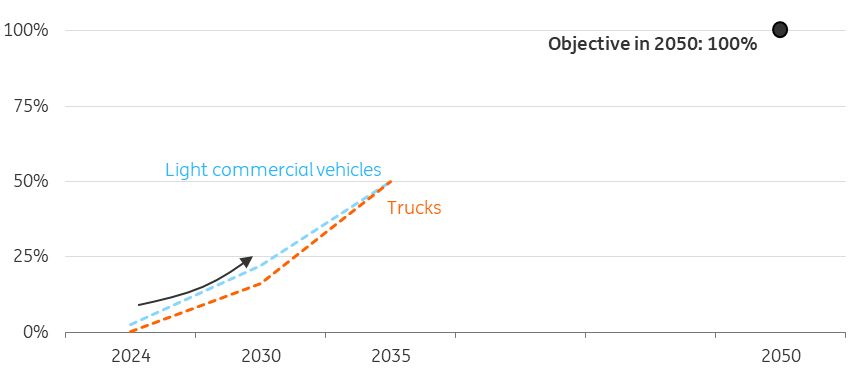

Locations with multimodal accessibility, automation potential, and easier access to labour remain attractive. In addition, the availability of sufficient grid capacity (to enable on-site electric charging) will increasingly determine the value of logistics real estate, given the expected continued growth of electric transport.

Faster growth of electric vehicles expected after 2030

Expected share of zero-emission commercial vehicles

The outlook for Dutch commercial real estate in 2026 is one of cautious progress. While the sector faces structural and cyclical challenges – such as elevated financing and construction costs, persistent geopolitical uncertainty, and stricter sustainability requirements – it is also evolving in ways that create selective opportunities. Segments aligned with long-term trends, including prime green offices, well-located logistics hubs, and housing resilient to physical climate risks, are likely to stand out as areas of resilience and value creation in the year ahead.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more