Divided Bank of England hikes UK rates by ‘only’ 50bp

The Bank of England has stuck to its guns and hiked rates by a further 50bp, less than markets had been pricing and defying some expectations that UK policymakers might be forced into a larger move given what other central banks have done recently. Gilts and sterling are failing to find support and remain vulnerable before Friday's 'fiscal event'

A divided central bank

What stands out most from this decision is that the Bank of England's Monetary Policy Committee is becoming more divided. It’s no surprise that three hawks voted to hike rates by 75bp, not least given some have been vocal about the implications of sterling's weakness this year. But for the first time since the great financial crisis, we have a three-way split. One dove, Swati Dhingra, voted to hike by ‘only’ 25bp, signalling she’s worried about the demand outlook.

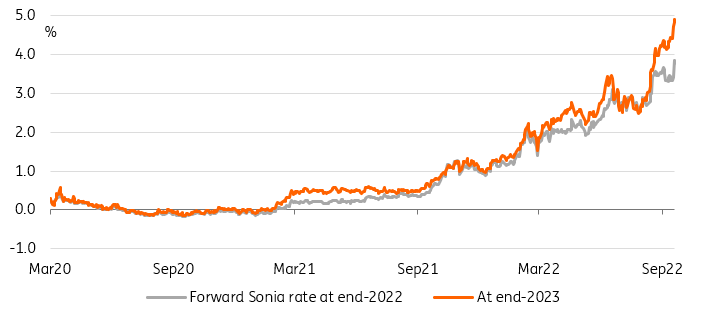

For investors, this increasing divide should be seen as a sign that market expectations are unlikely to be met. Swap markets are now pricing a peak for the Bank Rate close to 5% next year.

This increasing divide is a sign that market expectations are unlikely to be met

Admittedly the statement makes it clear that extra government spending, and we'll get more details on that tomorrow, will lead to higher medium-term inflation, given that it should dramatically lower the risk of a deep recession. But the accompanying meeting minutes also explicitly highlight that the government’s energy price guarantee - which caps prices for households and businesses this winter - reduces the risk of inflation expectations becoming de-anchored. Headline inflation will be around 5pp lower by January compared to a scenario without the price cap.

A 75bp move later this year can’t be ruled out, and it’s clear the bank is delaying some judgement on the government’s fiscal plans until it has had a chance to update its forecasts ahead of the November meeting.

But Thursday’s decision makes us more comfortable with our existing call that the BoE will simply hike by 50bp again in November, and by at least 25bp if not 50bp again in December. That would take Bank Rate a little above 3%.

Undeterred, Sonia swaps are now pricing a terminal rate near 5%

Gilts: no relief from the 50bp hike

A smaller than expected 50bp hike (markets were pricing 70bp ahead of the meeting) failed to provide any relief to gilts. The swap curve continues to price a terminal rate near 5% and the curve’s knee-jerk reaction was to invert further. The tone of the statement is expectedly hawkish in highlighting strong inflation dynamics and in noting that the energy price guarantee would add to inflationary pressure in the medium term. That three MPC members voted for a 75bp hike is leading markets to expect larger rises than the 50bp delivered today in the future, seeing as this has become the standard increment at both the Fed and the ECB.

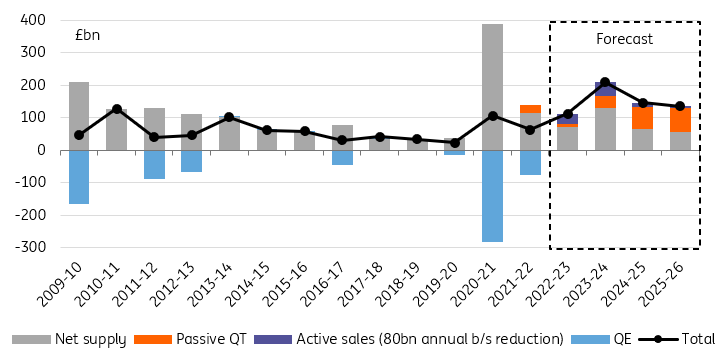

It should also come as no surprise that the BoE is pressing ahead with its active quantitative tightening (QT) plans, through bonds maturing and through active sales to start next month, by £80bn in the first year. We understand the Bank's willingness to show that its balance sheet reduction plan won’t be scuppered by market volatility but we continue to argue that current gilt market conditions warrant greater attention.

The BoE and the Treasury are competing for private investor demand

Attention now turns to tomorrow’s ‘fiscal event’. Market expectations are for the majority of new energy-related spending to be financed via gilt issuance. Given that future wholesale gas prices are unknown, this amounts to an open-ended liability for the Treasury. The BoE didn’t step off the brink today on QT and will add to the number of gilts private investors have to buy. The BoE and the Treasury competing for this private investor demand is the key reason why gilt yields have risen faster than their peers. We continue to expect 10Y gilts to trade 200bp above Bund yields. This could put gilt yields at 4% in the near future.

Fiscal support and QT mean private investors will have to absorb a record amount of gilts

BoE can only stand and stare at the weaker pound

With the market split on whether the BoE would tighten 50 or 75bp, the smaller 50bp adjustment has seen sterling sell-off by roughly 0.5%.

Reading through the statement and the minutes it is quite remarkable how little the pound featured. Businesses are concerned that the weak pound is adding to their input costs. But the Bank had very little to say on sterling beyond that it had fallen 4.5% since its August meeting. The lack of comment probably reflects the realpolitik of linking sterling weakness to growing fiscal concerns in the UK.

It is quite remarkable how little sterling featured

Sterling will go into tomorrow’s ‘fiscal event’ on a fragile footing. The 4% sterling sell-off since August did go hand-in-hand with the sell-off in gilts. Concerns over unfunded government giveaways and debt sustainability challenges could well see the pound continue to underperform this year. A stronger dollar also favours GBP/USD to 1.10, while even EUR/GBP can press 0.88. And don’t expect UK authorities to emulate their Japanese counterparts by trying to support the pound with FX intervention. The UK doesn’t have sufficient FX reserves for that.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article