Sugar surplus should limit upside

- 30 November 2022

- Commodities, Food & Agri

The global sugar market is set to see yet another surplus, driven by expectations of stronger output from Brazil, India and Thailand. We believe the surplus environment should limit further upside in sugar prices through 2023

2022/23 global surplus

Global sugar output in the 2022/23 marketing year is expected to hit around 180mt, which would leave it near record levels. Stronger output is largely due to expectations of higher output from Brazil. This production growth should mean that the global sugar market will see yet another surplus in the 2022/23 season- in the region of 4mt. This surplus should cap prices although we could see seasonally stronger prices over the CS Brazilian off-crop (1Q23). How much strength will really depend on how Indian sugar exports perform.

CS Brazil to see larger 2023/24 crop

The current Centre South Brazilian crop is quickly coming to an end as the region moves deeper into the rainy season. The industry is expected to crush around 530m tonnes of sugarcane (vs. 523mt last season) and with a sugar mix approaching 46%, sugar output is expected to total 32.5mt tonnes, marginally up on the 32mt produced the previous season. Changes to fuel taxes this year in Brazil (due to high prices) led to lower gasoline prices. The ethanol/gasoline parity has been above 70% for much of the current season, which saw motorists deciding to fill up with gasoline rather than hydrous ethanol this year. As a result, domestic ethanol demand in Brazil has been weak this year.

The industry started the crush late this season and given the fact that the region is entering the rainy season, it's unlikely all cane will be harvested this season. Therefore, there is the potential for an early start next season, so that mills can crush this stood-over cane. An earlier start to the 2023/24 crush would be helpful to the global market as it would ease some of the seasonal tightness during the off-crop. Furthermore, harvesting stood-over cane next season suggests that we will see a larger CS Brazil crop next season.

Given the more recent strength in sugar prices along with a generally weak Brazilian real, sugar returns for Brazilian mills are attractive in BRL terms. As a result, we would expect that mills increase their sugar mix for the upcoming 2023/24 season, which officially gets underway in April. However, with the change in government, we could also see some changes to the domestic fuel policy, which could have a knock-on effect on the sugar/ethanol production mix.

While recent rainfall has proved disruptive for the current harvest, this rainfall is likely to prove beneficial for the 2023/24 crop. The size of the 2023/24 season will depend on how the rainy season develops but early estimates suggest that CS Brazil could crush close to 570mt of cane. A larger cane crush and expectations of a stronger sugar mix suggest the region could produce in excess of 34.5mt of sugar next season. This would be the highest output from the region since 2020/21.

How much will India export in 2022/23?

Following Russia’s invasion of Ukraine, India has been concerned about inflation, which saw the government take steps to try to limit domestic price increases. This has seen the government take action to restrict exports of wheat, rice and sugar. In the 2021/22 season, mills were allowed to export 11.2m tonnes of sugar. And even though India is set to produce another large crop in the 2022/23 season, the government has decided to set the quota for the current 2022/23 season at 6m tonnes. To be fair, this quota runs until the 31 May. The government will then decide on whether to issue another tranche of export quotas for the remainder of the season (June-September). There are reports suggesting that an additional 3m tonnes of quotas could be made available at a later date. This will obviously be dependent on how the 2022/23 crop develops and ultimately domestic prices.

In addition, there have been reports of a small number of Indian mills defaulting on export contracts and trying to renegotiate at higher levels given the more recent strength in the world market. However for now, the tonnage of defaults appears to be marginal.

India is expected to produce 36.5m tonnes of sugar, an increase of almost 2% year-on-year. As we have seen in recent years, the amount of sucrose diverted to ethanol is expected to grow. Last season, 3.4mt of sucrose was diverted to ethanol production, whilst for this season 4.5mt of sucrose is expected to be diverted. This is a trend that will only grow in the years ahead given the government’s ambitious plans to bring forward a 20% ethanol mandate from 2030 to 2025. For 2023, the government is targeting an ethanol blend of 12% in fuel. This move helps reduce India’s import needs for oil whilst also dealing with persistent domestic sugar surpluses, which are largely due to government policy of fixing sugarcane prices for farmers.

Thai output continues its recovery

Thailand is expected to see sugar production in the current 2022/23 season increase by 3% YoY to 10.5mt. However, output is still expected to fall well short of the record 14.7mt produced back in the 2017/18 season. Thai output in recent years has suffered due to drought conditions but is slowly recovering. Planted area is still below levels seen prior to the drought years of 2019/20 and 2020/21. Higher fertiliser prices for much of this year have pushed farmers to plant more cassava instead of sugarcane, which is less fertiliser-intensive.

Tighter EU sugar market

EU sugar market set to tighten

The European sugar market has seen significant strength in prices so far this year. According to data from the European Commission, prices in September averaged EUR515/t. However, these prices are not a true reflection of spot prices. In fact, spot prices have been reported to be in excess of EUR1,000/t.

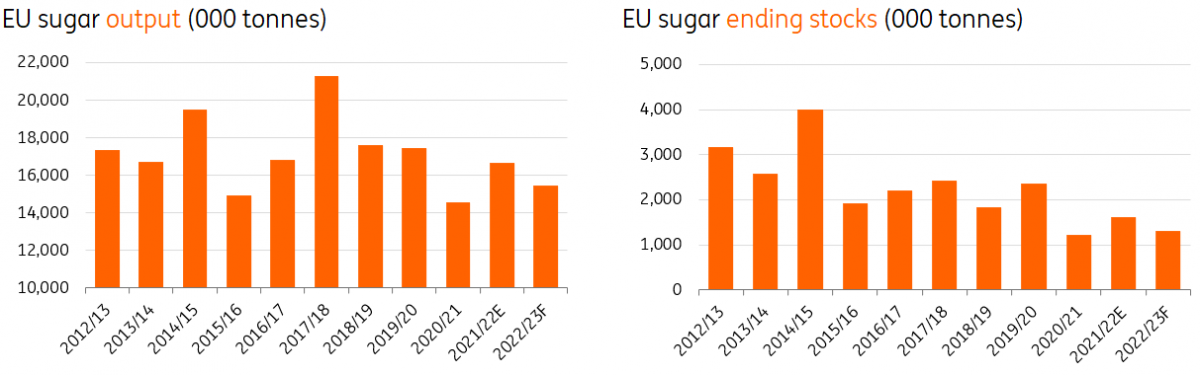

While EU sugar production in 2021/22 saw a recovery, the hot and dry summer seen across parts of Europe will have had an impact on the 2022/23 crop. European Commission data estimates that sugar yields will be down 3.4% YoY to 11.4t/ha while area is also expected to be down 4.3% YoY to 1.34m hectares. As a result, EU sugar production this season is estimated to total a little under 15.5mt, down almost 1.2mt YoY.

Assuming EU consumption in the region of 17.3mt, this does leave the region with a shortfall of a little more than 1.8mt. It is clear that the EU will need to meet this through a combination of stronger imports, weaker exports and the drawing down of inventory. The Commission estimates that stocks at the end of 2022/23 will total 1.3mt, which meets around 8% of annual demand, similar to levels that we have seen in recent seasons.

Given that EU spot prices are trading well above the world market, one may think that we would see a flooding of sugar into the EU. However, import duties on world market sugars are prohibitively high, which means we are not likely to see these flows. However, there is room for increased import volumes under current import quota programmes, which should prevent the EU market from getting significantly tighter. In addition, the large premium at which Europe is trading to the world market should limit EU sugar exports.

ING sugar price forecast

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

2023 Commodities Outlook: Stormy seas ahead

- This bundle contains 13 Articles