Middle distillate tightness to persist

- 30 November 2022

- Commodities, Food & Agri Energy

Middle distillates have been a standout among refined products. Inventories are tight in all regions and there is plenty of uncertainty over Russian flows when the EU ban comes into effect next year. While we expect middle distillate cracks to come off from the highs this year, the market is likely to still trade at elevated levels on a historical basis

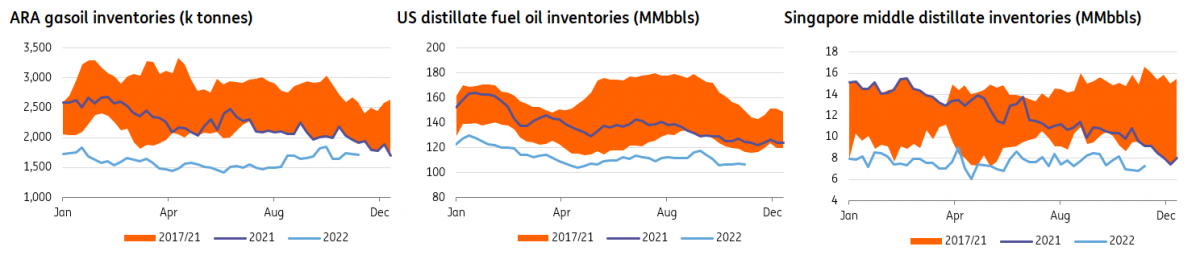

Low middle distillate inventories

Middle distillate inventories are tight around the globe. In the US, distillate fuel oil stocks are at their lowest levels on record for this time of year. And the tightness is even more extreme on the US East Coast. In Europe and specifically the ARA region, gasoil stocks are at their lowest levels since 2008 for this stage of the year, according to Insights Global. In Singapore, middle distillate stocks are down at levels last seen back in 2004 for this time of year.

The tightness in the market has led to governments in Europe tapping into emergency diesel stockpiles in a bid to ease the tightness. Emergency inventories have fallen from more than 41m tonnes back in January 2021 to less than 36m tonnes by the end of August. In the US, there have been calls for the release of diesel from the Northeast Home Heating Oil Reserve although these reserves are fairly modest at just 1MMbbls.

The US administration is concerned about tight inventories and high prices. As a result, options are being looked at to try to ease price pressures. These options include mandating producers to hold a minimum amount of fuel inventories, increasing the Northeast Home Heating Oil Reserve, and possibly limiting fuel exports. However, any step to limit fuel exports would have to be done in combination with a relaxation of the Jones Act which would make it easier to ship product from the US Gulf Coast to the US East Coast. Furthermore, increasing the size of the Northeast Home Heating Oil Reserve in the short term would only add more pressure given that this product would need to be bought from the market.

Middle distillate inventories by region

What is driving this tightness and will it persist?

There are multiple factors which have driven the tightness in the middle distillate market, and whilst some of the issues will likely intensify, some will ease. On balance, middle distillates are likely to remain relatively well supported.

Russia/Ukraine war - Russia is a large supplier of middle distillates and a significant portion of this goes into Europe. Prior to the war, Russia was exporting in the region of 1MMbbls/d of gasoil - almost 40% of total Russian refined product exports. While current sanctions and self-sanctioning have affected Russian flows already, the key disruption to these flows will occur once the EU ban on Russian refined products comes into force on 5 February 2023. This means Europe will need to find an alternative for the more than 500Mbbls/d it has been importing from Russia. And this is at a time when the global middle distillate market is already very tight.

Whether the EU ban on refined products is manageable will depend on how quickly trade flows can adjust and whether there are willing buyers of Russian gasoil further afield. If so, this would free up alternative supplies for the EU. However, the quality of product and logistics could certainly complicate the necessary shift in trade flows.

China export quotas - China has played an important role in the tightening of the refined products market. Policy has meant that the government has reduced export quotas for refined products in recent years, which has led to a sharp fall in refined product exports, including middle distillates. In 2019, Chinese exports of gasoil averaged 1.78mt per month. So far this year, Chinese gasoil exports have averaged just 554kt per month. The reduction in export quotas has been part of China’s broader aims of reducing emissions and improving efficiency within the refining industry.

However, more recently this seems to have taken a back seat, with the government more concerned about trying to prop up the economy. This is evident with the government issuing 15mt of export quotas back in September. In theory, these quotas should be used by the end of 2022, however, it appears as though refiners will be able to use these quotas through until the end of the first quarter in 2023. This should provide some relief to tight middle distillate markets in Asia. Recent trade data is already showing that Chinese gasoil exports picked up significantly in September and October. The refined product markets will have to wait and see if this policy change from China is a complete U-turn or whether in the medium to longer term the aim is still to drive consolidation within the domestic refining industry.

Reduced global refining capacity - Since the start of the Covid pandemic, we have seen a significant amount of refining capacity shut. These closures have been seen in Europe, the US and APAC. This was largely due to weak refinery margins during Covid. As a result of these closures, global refining capacity saw a net decline of 730MMbbls/d in 2021, the first net decline in 30 years.

In the US, operable refining capacity has fallen by a little more than 1MMbbls/d or 5% since February 2020. These declines have been predominantly driven by PADD1 (US East Coast), where more than 400Mbbls/d refining capacity has shut - reflecting a 33% decline in capacity in the region. This reduced refining capacity helps to explain the tightness we are seeing in refined product inventories on the East Coast.

Reduced capacity has meant that it has been more difficult for refiners to respond as demand has recovered. And it is unlikely that we will see large investment in refineries in Europe and North America given the uncertain demand outlook in the longer term. As a result, the oil market will have to rely on growing capacity from elsewhere.

There is a fair amount of new refining capacity expected to ramp up over 2023. The 615Mbbls/d Al Zour refinery in Kuwait recently started the first phase of commercial operations and will ramp up through 2023. In Nigeria, Dangote is scheduled to start up its 650Mbbls/d refinery in the middle of 2023. And in Oman, the 230Mbbls/d Duqm refinery is expected to start operations by the end of 2023. The IEA estimates that a net of 2.7MMbbls/d of new refining capacity will start up between 4Q22 and the end of 2023.

While a meaningful amount of capacity is set to start up next year, which will eventually help to offer some relief to middle distillate markets, the bulk of this new supply will only become available quite some time after the EU ban on Russian refined products comes into force.

Gas-to-oil switching - High natural gas prices through the year have led to a significant amount of demand destruction this year. This is particularly the case for industrial users in Europe and also power generators. However, where possible some have likely switched to cheaper fuels, including oil and specifically fuel oil and middle distillates.

As for what lies ahead, weaker gas prices more recently have taken some pressure off the market. However, the European natural gas market is still expected to be tight next year, which suggests the potential for continued switching to other fuels like oil.

Will there be relief in 2023?

The middle distillate market is likely to remain tight over 2023. There is plenty of uncertainty as we head towards the EU ban on Russian refined products. Clearly, this will see European buyers looking for supply elsewhere. Europe will likely have to rely more heavily on the Middle East for supplies, however, new refining capacity will take time to ramp up and so will not offer immediate relief to markets. In addition, expectations are that natural gas prices will remain elevated through 2023, which should support gas-to-oil switching. We should also not rule out the risk that the US takes action to alleviate tightness in the domestic market, which could have an impact on global middle distillate markets.

China could help the middle distillate market if the government releases sizeable export quotas for 2023. However, this is a big unknown for markets at the moment.

ING middle distillate forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

2023 Commodities Outlook: Stormy seas ahead

- This bundle contains 13 Articles