Coffee companies urged to step up efforts to tackle sector’s sustainability issues

Global coffee demand is growing but the coffee sector is struggling to tackle sustainability issues at farms. Traders and roasters have been ramping up their initiatives to solve issues and safeguard future supply, but there's a long way to go

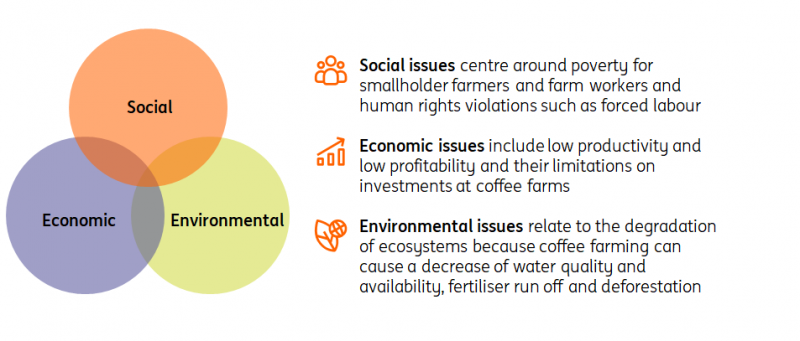

Coffee supply chains face three major sustainability issues

Among the many industries affected by the war in Ukraine is the coffee sector, with coffee companies having to suspend their exports to and operations in Russia. This has come at a time when the sector is striving to become more sustainable, because coffee farmers face persistent social, economic and environmental issues. Social issues are most pressing in coffee-producing countries in Africa, while certain environmental issues, such as excessive use of agrochemicals, are more prevalent in Brazil and Vietnam. In this article, we argue why it’s in the interest of coffee traders and roasters to find solutions, while we also take a look at current commitments in the industry and describe the root causes that prevent companies from doing more. We wrap up the article with a view on what conditions are needed to speed up structural change.

Three types of issues come together in the coffee industry

Poverty among small coffee farmers is a common problem in many countries

Estimated number of smallholder coffee farmers* and proportion of farmers living in poverty, country ranking based on the share of total global coffee production

Future coffee supply and variety depend on support from traders and roasters

It is in the interest of coffee traders and roasters to counter the issues in their supply chains as they rely heavily on the 12.5 million smallholder farmers who produce between 60-75% of the world's coffee. Although coffee production has increased by 75% since the 1990s thanks to improved yields, both ageing farmer populations and climate change pose risks for future coffee supply.

- The average coffee farmer is estimated to be around 50 years old. Ageing farmer populations can negatively impact coffee yields as older farmers tend to invest less. It can also lead to a decline in the total coffee area when farmers have no successor.

- Climate change poses multiple risks for the industry given that coffee trees are very sensitive to temperature rises. In the short term, the increased likelihood of extreme weather events like droughts or frosts negatively impacts yields. In the longer term, some regions are expected to become less suited for coffee production which poses a threat to general supply and a specific threat for coffee varieties in the most affected regions. Providing the know-how and technology to adapt to the effects of climate change is one way of lowering these risks.

There are plenty of sustainability initiatives among major coffee companies…

Sustainability strategies in the coffee sector tend to have at least one pillar aimed at farmers. Over the last decade, many major traders and roasters developed a range of programmes and initiatives to support farmers and increased their reporting on this topic. Their strategies often focus on increasing productivity and decreasing costs. For such initiatives, companies usually join forces with state-led development programmes and non-profit organisations to provide things like training and higher quality coffee trees. In many cases, these activities fill a gap in coffee regions where governments are not able to provide the same level of security and support as in major producing countries like Brazil and Vietnam.

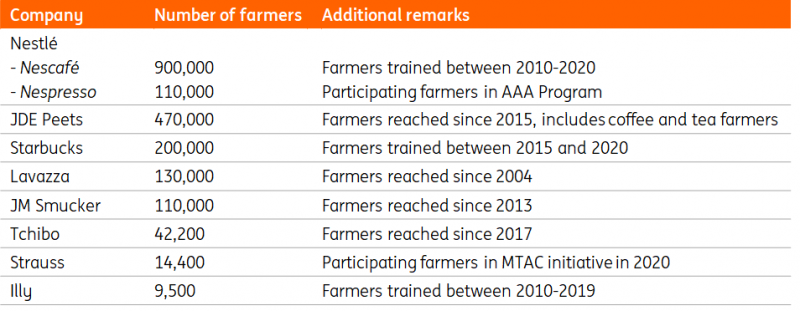

Millions of farmers are reached by programmes in which the largest roasters participate, but overall we estimate that eight out of ten smallholder farmers haven't been reached.

Many coffee roasters mention the number of farmers involved in their programmes and initiatives

…but it's unclear whether the money they invest is sufficient

There is an ongoing debate within the coffee industry about the additional effort needed to solve the major issues in the supply chain. Previous research suggested that an annual US$10bn global fund would be needed to make significant progress in solving sustainability issues in the sector. But such an overarching fund hasn’t become a reality yet. Meanwhile, bottom-up data from several stock listed coffee companies shows that they invest between 0.5% and 2.5% of their annual revenue in sustainability. If that range would apply to all of the ten major global roasters, then their combined investment amounts to between $250m and $1.35bn a year. On top of that, there are investments by smaller coffee roasters, traders and (development) funds from governments, but when all taken together it seems unlikely that these add up to $10bn.

More sustainable production makes sense, but economics don’t always play out

So what is holding coffee companies back from showing a deeper commitment? We have found several reasons why there is a gap between what’s currently invested and what'st needed:

1. Companies will always make trade-offs due to competition within the coffee sector.

Given the competitive environment in which they’re operating, coffee traders and roasters will make trade-offs as investments in sustainability compete with other investment opportunities. Research also shows that having sustainability measures in place is not a universal practice, with one in three companies in the coffee supply chain not having any.

2. Fragmentation in the number of farmers and the number of producing countries.

Due to the fragmented nature of supply chains and the diversity of sustainability issues, creating impact often requires a tailor-made and structural approach across multiple countries, which is labour-intensive and costly. On top of that, the farmers who need it the most are also the least connected to (digital) infrastructure and thus the hardest to reach.

3. A lack of economies of scale complicates the business case for many smallholders.

Coffee production has become more concentrated in a few countries and for many farmers it’s hard to compete on price with the highly-productive coffee sectors in Brazil and Vietnam. For example, the average coffee plot in Brazil is 120 times larger than in Uganda, 30-60 times larger than in Ethiopia and five times larger than in Colombia. For some farmers, a focus on premium speciality coffees does provide an alternative and a better business case but for many others it is difficult to be profitable throughout the price cycle.

4. Farmers can be reluctant to change the way they work for a variety of reasons.

Complying with higher sustainability standards and more regulation usually requires investment or leads to higher operational costs, while the gains in terms of better productivity and/or a higher price are uncertain or lacking.

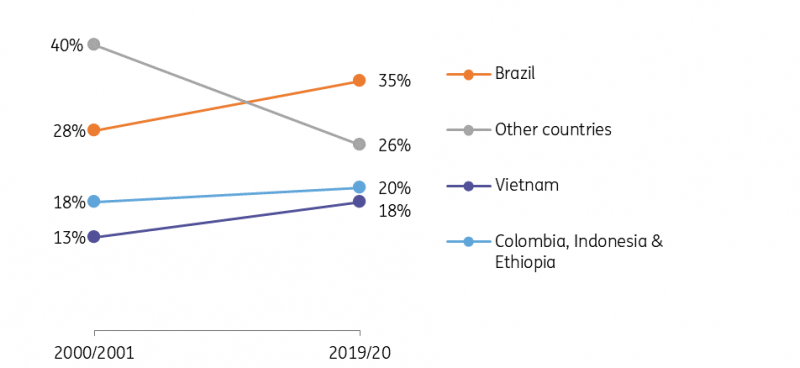

Coffee production is getting more concentrated in a few countries

Share in global coffee production

Without a coordinated approach it’s more difficult to reach structural change

Coffee traders and roasters play a pivotal role, but they cannot solve the issues at coffee farms by themselves. Companies along the coffee supply chain, governments and consumers share responsibility and their combined actions can lead to structural change. Developments in the market for certified coffee provide an example of how this works out in practice.

The case for certified coffee

Many major coffee companies have commitments to raising the share of sustainably produced and sourced coffee. Joint efforts to increase certified coffee production have led to a situation where there is more certified coffee than the market can absorb. At this point it’s up to the brands that sell coffee to make the more sustainable cup of coffee the default option, and to get consumers to pay a certain premium. In that sense the premiumisation of coffee in developed markets is a favourable trend, but getting that premium will be a tougher nut to crack in growing coffee markets where affordability is of major importance.

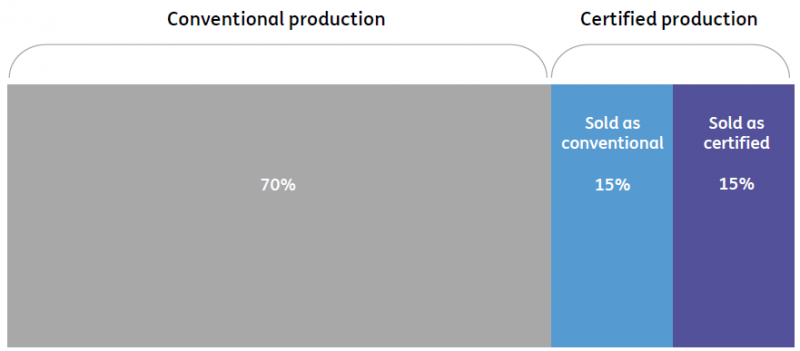

Supply and demand for certified coffee don’t match and an estimated 50% of all certified coffee ends up as regular coffee

Finally, governments in both coffee exporting and importing countries can stimulate the adoption of sustainable practices by translating them into laws and regulations. But lawmakers face a delicate balance because well-intended measures in one coffee producing country can result in a disadvantage to other exporting countries. This can only be avoided by aligning interests and jointly raising the bar. Interventions can also come from importing countries – one example is the EU’s deforestation regulation which requires everyone selling coffee and several other products in the EU to prove they’re living up to certain standards.

Only half of all certified coffee production is actually sold as certified coffee

Coffee production and coffee sold per certification/verification scheme* in 2019

Efficient infrastructure is crucial for more impact at farm level

When commitments are in place and investment is secured, it comes down to execution and partnerships with others like farmer organisations, retailers, governments, NGOs and financial service providers. Due to the complexity of their supply chains, coffee companies require an efficient physical and digital infrastructure to scale up their impact. Such an infrastructure consists of several elements in order to:

- Asses farmer needs: Traders and roasters have to be able to reach out and collect input from a huge number of farmers in an efficient way to make their approach as tailor-made as possible.

- Distribute the right support: It requires a lot of effort to set up the physical infrastructure to distribute tangible goods like fertiliser and young coffee trees, and the partnerships to bring intangible knowledge to farmers in remote places across the globe.

- Prove the impact: The evolution of reporting standards creates more urgency for coffee companies to prove their impact for investors and other stakeholders. So systems that enable or track payments to farmers can be an important part of the digital infrastructure as they provide a guarantee that farmers received a living wage or a premium for reducing environmental impact. Novel schemes in other supply chains such as Nestle’s Cocoa Income Accelerator Program will be watched closely within the coffee sector.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article