Astonishingly high cocoa prices set to continue as deficit concerns grow

Fresh record highs in cocoa prices last year are set to continue into this one as supply fears continue to mount. The cocoa market is set for a third consecutive deficit

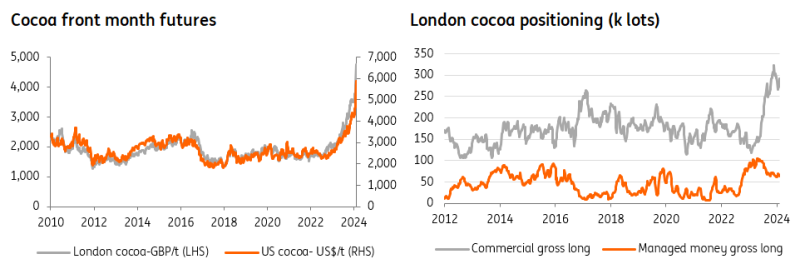

Cocoa hits record highs

The cocoa market was the strongest performing commodity of 2023, with London cocoa finishing 2023 up 70%, while US cocoa futures rallied a little more than 61% last year. The relentless move higher has only continued into 2024, with US cocoa futures up a further 39% so far this year, while London cocoa has rallied by an additional 37%. Both contracts have hit new record highs this year.

Concerns over West African supply, specifically in Côte d'Ivoire (Ivory Coast) and Ghana, have driven the market higher. The bullish narrative has attracted participants into the market, with aggregate open interest in London cocoa surging above 400k lots in December, although admittedly, it has fallen back towards 350k lots more recently. However, this is still above the 2018-22 average of around 270k lots.

But looking at positioning data and specifically the managed money (speculative) category for London cocoa, there has not been a significant increase in buying. In fact, the managed money gross long has decreased from roughly 105k lots in May last year to around 64k lots currently. Instead, the squeeze appears to have been driven by commercial players, where the gross long position has increased from around 119k lots in February last year to more than 290k lots currently. Whether this is an intentional squeeze or not is less clear. If it is, it wouldn't be the first time the cocoa market has experienced one. Although supply shortfalls could be seeing some suppliers/traders needing to find alternative supplies in order to meet contractual obligations, the uncertainty over how much higher prices could go may also be seeing some physical buyers rushing in to lock in prices.

The key question, and also the toughest, is how much higher cocoa prices can go. They need to go to levels where we start to see significant demand destruction. We are already seeing some of that already, but clearly not enough to bring the market back into balance and ease tightness concerns.

Cocoa prices surge as commercial long position grows

West African supply is the big concern

Africa is crucial for the global cocoa market, with 73% of global supply coming from the region. West Africa dominates supply. Côte d'Ivoire is the largest producer, making up 44% of global supply. Ghana, the second largest producer, holds a share of around 14% of global output.

Last year, heavier-than-usual rainfall raised concerns over the impact it would have on the crop, with rising cases of black pod disease. Heavy rains also led to issues over cocoa being delivered to ports. This year, drier weather conditions and strong Harmattan winds are raising only further concerns over how the current crop evolves.

Cocoa arrivals at Ivory Coast ports are down significantly; as of 11 February, arrivals totalled 1.09mt so far this season, down 33% YoY.

Côte d'Ivoire produced 2.18mt of cocoa last season, while for this season, expectations are that the crop will be no more than 1.75mt. Meanwhile, for Ghana, there are suggestions the crop could be 25% lower YoY. These losses would be equivalent to around 11% of global demand.

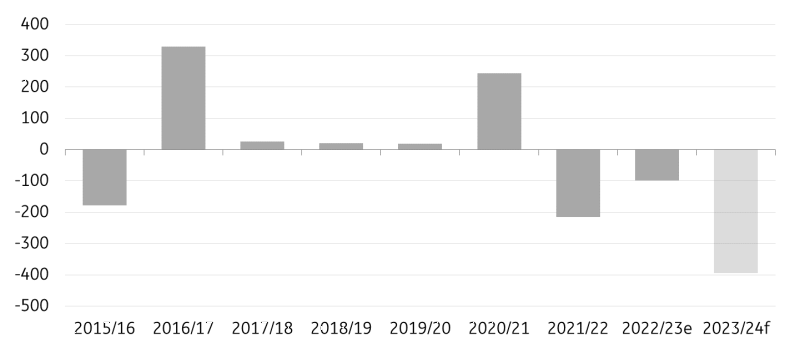

Market set for a third straight deficit

The issue for the cocoa market is that it was already in a deficit environment in the two previous seasons, which has meant that global inventories are already at their lowest levels since the 2015/16 season. According to the International Cocoa Organization, the global market saw a deficit of 216kt in 2021/22 and 99kt in 2022/23. And with a big fall in West African output in the current 2023/24 season, the market is set for a sizeable third deficit- close to 400kt, which would take stocks to their lowest levels in at least a decade.

Concerns about the impact on the 2024/25 season will also be raised. The cocoa regulator in Ivory Coast has halted forward sales for the 2024/25 season until there is some clarity on how next season’s crop may play out.

Global cocoa supply/demand balance (k tonnes)

How is demand responding to higher prices?

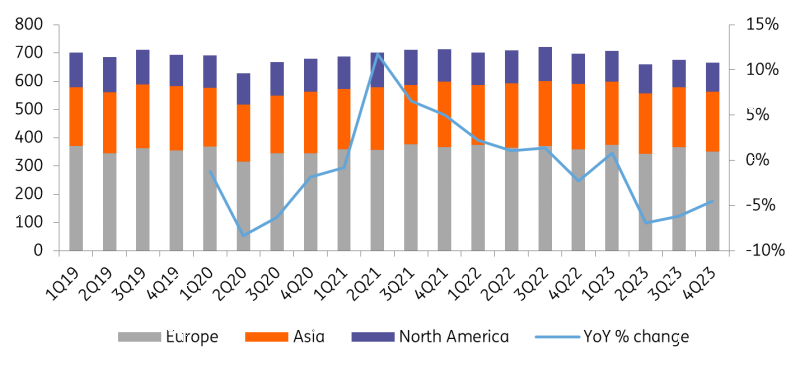

Stronger prices last year led to lower demand. However, the demand destruction we have seen has not been enough to balance the market, suggesting that stronger prices will be needed in order to leave the market in a more comfortable position in terms of supply and demand. Looking at combined grinding data for North America, Europe and Asia, grindings in 2023 were down around 4% YoY.

North America saw the largest decline, with grindings falling by a little more than 9% YoY, while for Asia, grinding fell by around 5% YoY. However, the key grinding region, Europe, has seen demand remain a little bit more sticky, with grinding last year only a little more than 2% lower YoY. Clearly, higher prices are still needed to drive more aggressive demand destruction in Europe.

Regional quarterly grindings (k tonnes)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article