CNY at a glance: Is the worst of China’s depreciation pressure over?

Short-term depreciation pressure on the yuan has eased as external factors have outweighed domestic issues

| 7.10 |

Our 2024 year-end USDCNY forecast |

| Lower than expected | |

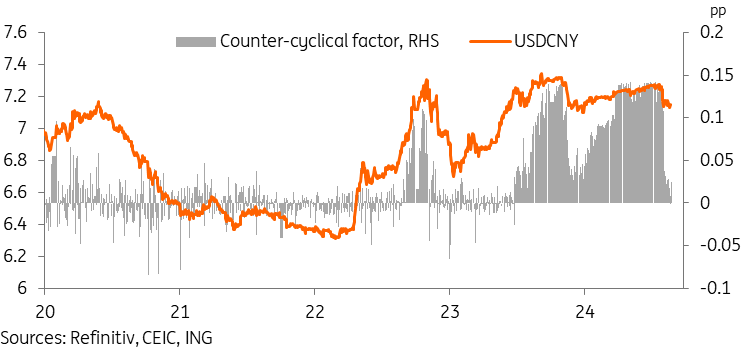

Counter-cyclical factor has moved back toward 0 amid CNY recovery

The People's Bank of China utilises a counter-cyclical factor which is an adjustment to their daily fixing during periods of high volatility. This tool is used to maintain the relative stability of the yuan and is one of the two main deciding factors for the trajectory of the USDCNY pair.

Since July 2023, the usage of the counter-cyclical factor has been quite significant, and marked new highs in June and July this year, reflecting the PBOC pushing back strongly against significant depreciation pressure on the CNY. However, the depreciation pressure faded quickly in August as a weaker dollar led to a rally of Asian currencies including the CNY. As a result, we've seen the counter-cyclical factor fall to nearly zero, which indicates that the daily fixing is in line with the closing price of the previous trading day.

After over a year, the PBOC's impact on the USDCNY pair has turned neutral for now. We expect use of the counter-cyclical factor to resume if necessary, but it looks like policymakers are comfortable with where USDCNY is trading, and indeed market reports are that they are seeking out research on the impact of a stronger CNY.

Counter-cyclical factor has dropped to near zero

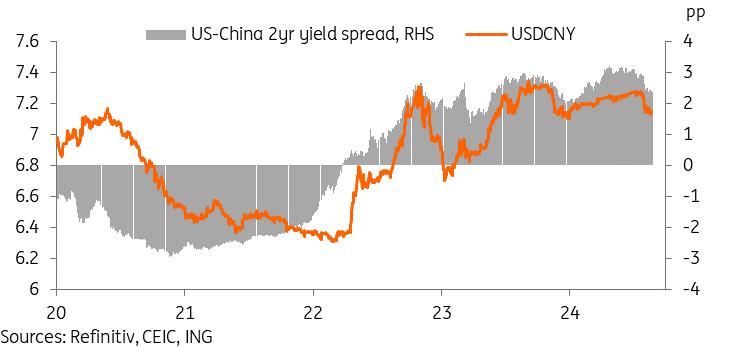

Yield spreads are moving to favour further CNY recovery

The other major factor in the USDCNY trajectory is the yield spread between Chinese and US bonds. While these spreads will vary across the curve, we tend to look at the 2-year yield spread as representative as it has good success in tracking the trajectory of the USDCNY pair.

The 2-year US-China yield spread has narrowed gradually in the last few months, with the current 2.4pp down significantly from this year's peak of 3.18pp seen in April.

Most of this has been driven by the US side, as US yields have fallen significantly over the past month as market expectations for a more aggressive rate cut cycle grew. Our ING house forecast is for 100bp of US cuts in both 2024 and 2025.

However, we've also seen a bit of action on the China side as well, with 2-year yields up slightly in August after threats of intervention from the PBOC caused some local financial institutions to cut holdings. Depending on the extent of intervention, we still expect market momentum to continue to add buying pressure on Chinese government bonds and to add to downward pressure on yields in the near to medium term.

Yield spreads have started to move in favour of a CNY recovery

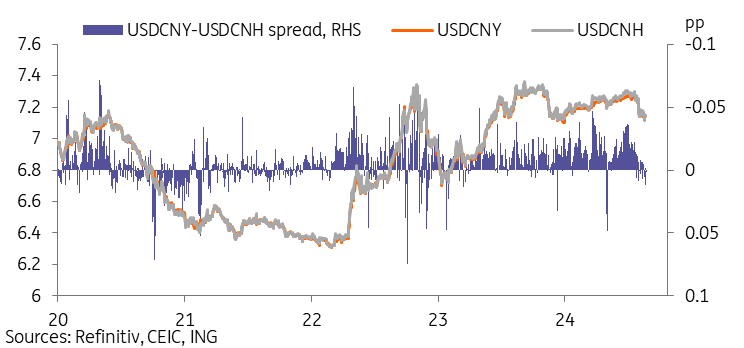

CNY-CNH spreads briefly moved to positive levels over the past month

Typically, the CNH and CNY pairs track very tightly as arbitrage opportunities typically quickly close any significant spread. However, the CNH tends to move a little more in either direction when there is momentum.

Over the past year, the USDCNH pair has generally traded higher than the USDCNY pair, as offshore investors were generally looking for more yuan depreciation.

In the last few weeks, momentum has turned around, with the USDCNH actually trading at a lower level than the USDCNY pair on multiple days; other than several one-day spikes, this is the first time since 2022 we've seen this, and it generally reflects offshore investors positioning for a yuan recovery.

USDCNH moved lower than USDCNY pair in first sustained period since 2022

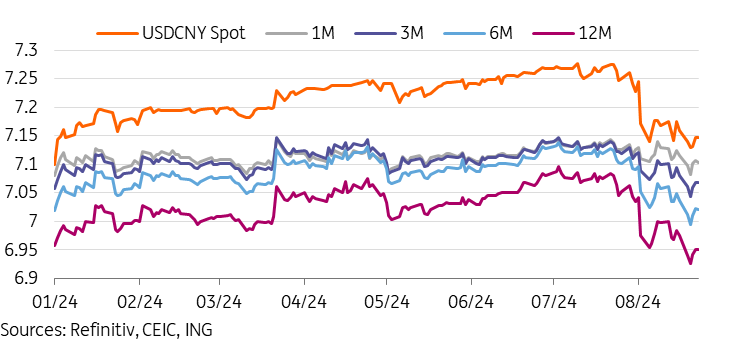

NDF market is pricing in quite a strong recovery of the CNY

The NDF market has generally been looking for a CNY recovery since late 2022, and generally, expectations for further CNY appreciation strengthened along with the spot.

Currently, NDFs indicate that the market is pricing in the USDCNY falling below the 7.00 level on a 12-month horizon, which is a little more yuan bullish than our current forecasts.

CNY NDF market developments

Developments are mostly driven on the external side with domestic challenges remaining

While markets may expect the PBOC to be breathing a sigh of relief as depreciation pressures fade, it will nonetheless remain vigilant as the pressures are largely driven by external factors. If we see hawkish developments in the US, we could soon be back to the same state from the last several months.

Domestically, several factors continue to represent a headwind on the yuan. Weak growth is likely to lead to more PBOC easing, and given interest rates remain low and risk appetite for domestic assets is still limited, there is still a level of capital outflow pressure.

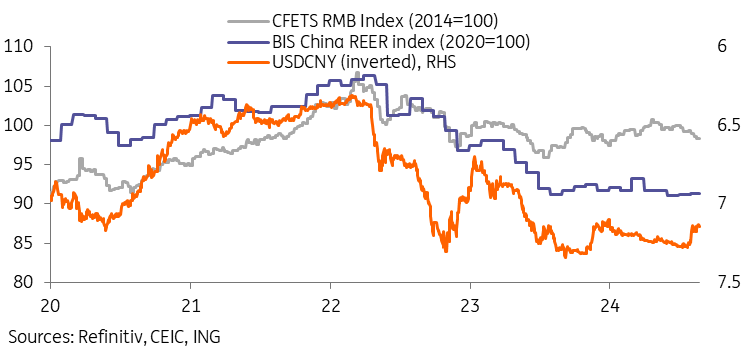

We can see that China's CFETS RMB Index, which is composed of a basket of currencies, generally continued to weaken over the last several months despite the appreciation against the dollar.

RMB index continued to slide despite recovery of the CNY against the USD

Our outlook for the CNY

We generally expect that external developments will continue to outweigh domestic drags, and the CNY should gradually move stronger. We expect the CNY to remain a low-volatility currency relative to other Asian FX.

While we have a relatively high degree of confidence in a more CNY-favourable yield spread in the coming months, the US elections represent a wildcard to the CNY. While little is yet known of a potential Harris administration's policies toward China and many market participants appear to be pricing this as a "Democratic status quo" type scenario, if she does signal a pivot away from the tariff policy (she and her VP pick Tim Walz both previously criticized the tariff policy) toward a different China policy, it could be another catalyst for further CNY upside. On the other hand, a Trump victory is generally seen as dollar-positive, and additional tariff action against China could add an extra country-specific downside risk for the CNY.

Our current baseline scenario has the USDCNY ending the year around 7.10, with a medium-term fluctuation range between 7.00-7.30, and our global ING interest rate scenario should favour the CNY appreciating over a 1-2 year horizon. We forecast the USDCNY to move stronger toward 7.00 by the end of 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article