Energy transition to fuel robust demand growth for copper

We expect a synchronised recovery in copper demand from both China and other economies next year. Energy transition-related copper demand is set to accelerate as the world pivots towards a ‘green recovery’ after the pandemic. Given the bullish demand narrative and favourable macros, risks for the market are tilted to the upside

A stunning market recovery after Covid-19 rattles supply

Following the Covid-19 blues, London Metal Exchange copper has bounced back strongly as a result of the robust demand recovery from China and a weaker USD. While on the supply side, Covid-19 has primarily disrupted some mine operations in Latin America, but as some mines have returned, the world’s largest copper miner, Chile is on track to achieve modest output growth this year.

This year’s disruptions compounded with a major mine that is transitioning underground and will lead to the global mine supply declining by 2% YoY in 2020, before rising to 3.1% YoY next year

Overall, this year’s disruptions compounded with a major mine that is transitioning underground and will lead to the global mine supply declining by 2% YoY in 2020, before rising to 3.1% YoY next year. For 2021, the disruption rate is expected to remain well above the long-term average, largely due to uncertainties around labour contract renewals. Meanwhile, the concentrate market has remained tight due to robust demand from smelters. This is evident in the lower treatment and refining charges (TC/RCs) on spot terms, which dropped to an eight-year low of around US$50/tonne compared to the annual benchmark of US$62/tonne for 2020.

Further tightening the market was China’s restriction on scrap copper imports, while Covid-19 related disruptions didn't help. China customs data shows that copper scrap imports into China dropped 50% YoY over the first ten months of 2020. As a result, the shortfall in scrap supply saw the market turn increasingly to cathode. However, in October, China released the new HS code for high-quality copper scrap imports, which will allow any scrap which meets the new standards to be imported without restrictions from 1 November 2020. As this helps in clarifying the standards for imports, we expect higher grade scrap imports into China to recover from this year’s low, but it may take some time for market participants to adapt to the changes.

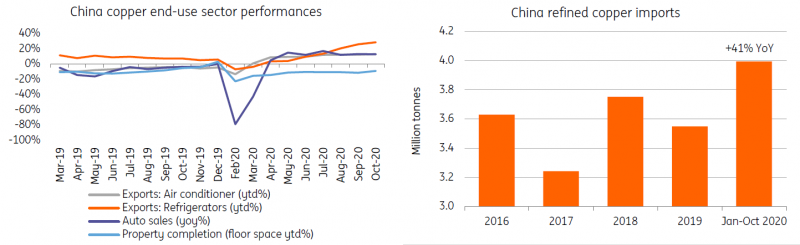

Demand recovery along with robust imports from China

The recovery in copper demand has primarily been driven by a speedy demand recovery in China, and further fuelled by government-led investment in metal intensive sectors after the lockdown. Real copper demand is driven by traditional old infrastructure projects in parallel with projects put forward under new infrastructure initiatives.

Other sectors have also seen a speedy recovery since 2Q20, which has helped to drive copper usage higher. This includes the property sector, the automotive industry, while a recovery in exports of copper intensive end-use products such as air conditioner and refrigerators has also played a role. Strong copper imports into China also helped to inflate the demand in apparent terms, growing by 10% in 2020, and this has further helped to absorb some surplus in the offshore market. China’s unwrought copper imports have increased 41% YoY to 4mt over the first ten months of the year, driven by several factors including the positive arbitrage and potential purchases by the nation’s State Reserve Bureau.

The 'green' revival holds the future for demand prospects

Looking ahead, there is likely to be a synchronised recovery in copper demand from both China and other economies.

The demand side bull narrative lies in the energy transition, as the world pivots towards a ‘green recovery’ post-pandemic. We are seeing some major economies gearing towards a greater share of power generation from renewable energy, while also seeing an increase in penetration rates for new energy vehicles (NEVs). Based on existing government plans, we expect green investment induced copper demand to register double-digit growth over the next five years.

Major economies are gearing towards a greater share of power generation from renewable energy

China recently revealed its plan on new energy vehicles (2021-2035), in which it plans to boost NEVs market penetration to 20% by 2025. Copper will benefit from this, along with the need for further charging infrastructure. In Europe, it is expected that the Green Deal could boost the region’s copper demand by more than 800kt over the next seven years, according to BNEF. The focus of the projects will likely be on incentives for electric vehicles and charging-infrastructure installations, doubling the retrofit rate in buildings to improve energy efficiency, and supporting wind and solar power.

Globally, multiple countries have pledged to achieve a carbon-neutral economy from 2050, and this reinforces the view of robust demand growth for copper in the years ahead.

End-use sectors recovery drives the real demand, and a robust import leads to higher growth in apparent demand

Price Outlook

Global reportable copper inventories (exchanges and China bonded) have fallen by around 25% from the start of this year, and have remained low on a historical basis. The refined copper market is seen to be relatively balanced in 2021, with a negligible surplus. Given it is estimated that the disruption rate for mine supply next year will still be above the long-term average, along with expectations for a synchronised recovery in global demand, the fundamentals for copper are likely to remain constructive.

As copper prices have already jumped by 64% from the lows of US$4,630/tonne in March, much of the bull narrative has already been priced in. However, the market will need a favourable macro environment to continue with its current trend, along with further weakness in the USD, which is what we expect. We expect LME 3M copper to average US$7,400/tonne over 2021.

ING forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

8 December 2020

ING’s Commodities Outlook 2021 This bundle contains 11 Articles