Clear signs of recovery for Dutch new housing market in 2025

Higher turnover in project development, more building permits and increasing new home sales are all signs of a recovery in the Dutch construction sector in 2025

Expected decline in construction volume in 2024

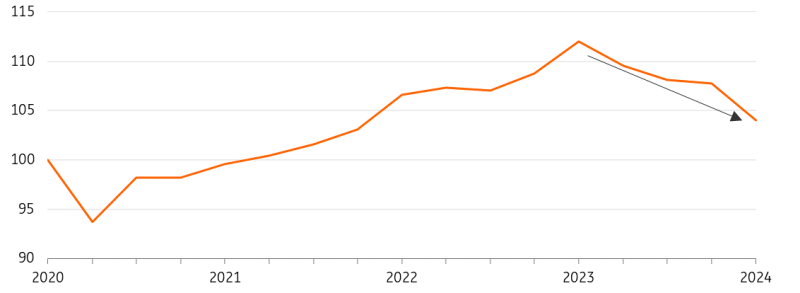

ING Research expects that Dutch construction output will shrink by around 3% in 2024, mainly due to a sharp decline in the first quarter. New construction production in 2024 will still be affected by earlier declining permitting and declining new home sales in 2023. In 2025, there will be a recovery for the Dutch construction industry, mainly due to the upswing in new build production of homes.

Construction production shrank in four consecutive quarters

Dutch construction production volume in added value (index Q1 2020= 100)

Clear signs of upcoming recovery

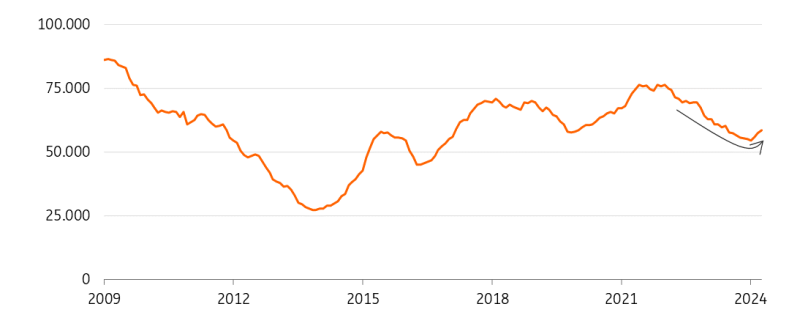

At the beginning of the construction value chain, clear signs of recovery are visible. Turnover of project developers is increasing and the number of building permits issued has increased in the first months of 2024. In addition, sales of new build homes are on the rise due to the improving housing market again. In addition, the production of concrete, cement and bricks increased slightly again in the first four months of 2024, after a contraction of more than 15% in 2023.

The contraction of the building materials industry has ended

Production of the Dutch building materials industry, seasonally & working days adjusted (index 2021=100 until April 2024)

Building permits are on the rise again, but new environmental law could have an impact

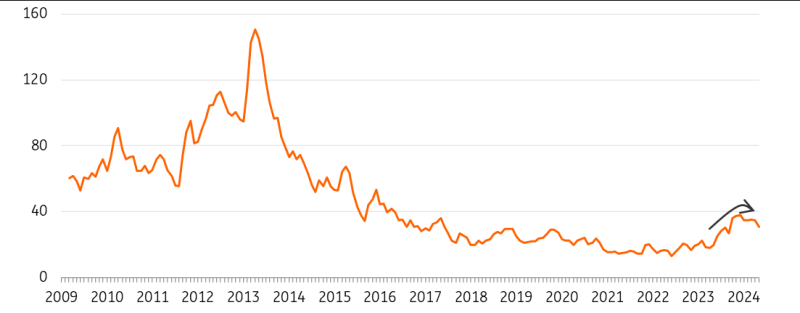

In May 2024, 6,753 building permits were issued for new build homes. That's a 23% increase compared to the same month in 2023. Substantial increases were also reported by Statistics Netherlands (CBS) in February and March. This could be positive for housing construction. However, the introduction of the new Environment and Planning Act (Omgevingswet) and the Quality Assurance Act (Wet Kwaliteitsborging) as of the beginning of 2024 cloud the picture. It is possible that builders and project developers submitted applications just before 2024 so that they still fell under the old (familiar) legislation. As a result, there may now be an additional increase in the granting of permits.

The number of building permits issued is increasing again

Building permits issued for new build homes (moving annual total per month until April 2024)

Low growth in the infrastructure sector

We expect small positive growth for the infrastructure sector in 2024 and 2025. This is mainly due to the much-needed reinforcement of the electricity grid, investments in infrastructure for new housing construction and a small impulse from the new Dutch cabinet.

Staff shortages still main obstacle

% of Dutch builders with production obstacles due to: (seasonally adjusted until June 2024)

Structural staff shortages are the biggest obstacle in the construction industry

Despite the drop in demand, staff shortages remain the biggest obstacle for Dutch construction companies to keep production going. In June, 18% of contractors indicated that they were mainly limited by a lack of (well-trained) staff. Despite the decline in production volumes, this remains a structurally pressing problem. On the other hand, 15% of companies in the sector indicated in this month that they did not have enough orders to keep their construction volume going.

Slight increase in construction bankruptcies appears to be over

Number of bankruptcies at construction companies per month up to and including May 2024 (three-month moving average, excluding sole proprietorships)

Few bankruptcies

All in all, most Dutch construction companies are in good shape after years of high growth. We expect that most companies should be able to weather the volume contraction of 2024 relatively well. The number of contractor bankruptcies did increase in 2023, but historically it is still low. And in the first months of 2024, they actually dropped again slightly. Structurally, the prospects for construction after 2024 are good with the tight housing market and sustainability challenges. We also expect some growth in construction volumes in 2025 (1.5%). However, it remains important for construction companies to stay future-orientated and to invest in digitalisation, attractiveness as an employer and sustainability.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article