China’s Two Sessions economic targets signal greater confidence

China's 2025 key economic targets were released today, including an “around 5%” GDP goal in line with our expectations. Growth and fiscal ambitions imply stronger policy support this year

| "Around 5.0%" |

China's 2025 GDP growth target |

| As expected | |

GDP growth and fiscal targets imply stronger fiscal policy support this year

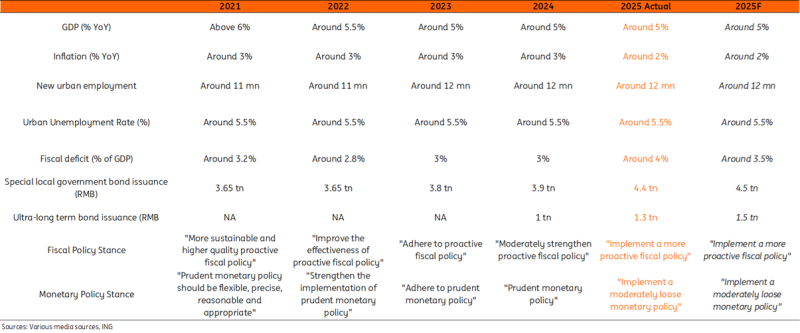

The National People's Congress opened in Beijing today with officials announcing a growth target of “around 5%,” and also unveiling other important targets including the inflation and fiscal targets. The key economic targets were broadly in line with our expectations this year.

The 2025 GDP target mirrors last year’s. As we've previously stated, policymakers tend to attach high importance to achieving this goal; China has a strong track record of meeting it year after year. We tend to see the strength of fiscal and monetary support vary depending on how much is needed to reach the year’s growth target.

Repeating the "around 5%" growth target, despite a more challenging external environment, is in our view a show of confidence and a harbinger of stronger policy support for domestic demand. In his speech, Premier Li Qiang acknowledged the "adverse impact of changes in the international environment," as well as the impact of weak public sentiment, is dragging domestic demand. Given these two big headwinds, more assertive policy will be important to help pick up the pace of growth.

The fiscal targets back up this story. Targets for special local government bond issuance rose 12.8% from RMB 3.9tn to RMB 4.4tn, while the ultra-long term bond issuance target was raised 30% from RMB 1tn to RMB 1.3tn. The fiscal deficit target was also raised from 3% of GDP to 4% of GDP. These targets imply that we will see a stronger fiscal policy push this year, while still keeping in mind long-term debt sustainability considerations.

Monetary policy easing set to continue despite lowering of inflation target

The monetary policy direction was changed from "prudent" to "moderately loose" at this year's Two Sessions. This change was previously flagged at last December's Central Economic Work Conference, and was the first major shift since 2011. The Government Work Report noted that we would see timely cuts in interest rates and required reserve ratios. We expect that the first of these cuts could come in the next month or two, especially given risks related to US tariffs set to begin in early April. We are currently forecasting 30bp of cuts to the 7-day reverse repo rate and 100bp of RRR cuts in 2025. We see a potential for more easing if growth comes in weaker than expected.

The Government Work Report reiterated a desire to “maintain the basic stability of the RMB exchange rate at a reasonable and balanced level.” This implies that top-level policy guidance hasn’t changed; CNY stability remains a priority and the People’s Bank of China will likely continue its stabilisation efforts. Our key call on the USDCNY this year is that China won’t intentionally devalue the currency to help offset tariffs. This would likely be ineffective, as Trump could easily hike tariffs further -- indeed President Trump has already warned against currency devaluation despite China's efforts to maintain the currency stability. Intentional devaluation would also nullify the benefits from exchange rate stabilisation efforts these past few years. We don't see a reason to change our 7.00-7.40 fluctuation band call for now. We believe the CNY will likely remain a low-volatility currency this year.

As we expected, China lowered its inflation target for the year from 3% to 2%. This isn’t surprising, as deflationary pressure has been significant these past few years. Actual inflation has fallen well short of 3% in the past years. That said, we think the implications for policy are quite limited. We don't expect concerted efforts to move inflation higher. Setting a 2% target puts China in line with most global central banks, and seems a natural next step. Even with monetary policy easing expected to continue this year, we don't see inflation overshooting the 2% target barring some significant unexpected shocks.

China's 2025 key economic targets mostly in line with forecasts

Shift in government work tasks shows increased priority of boosting domestic demand

The sequencing of this year's government plans show that domestic demand has become the top priority.

The first mentioned target was to "vigorously boost consumption and improve investment efficiency." A similar goal last year to "boost domestic demand" was only put in the third slot. This year promised RMB 300bn of ultra-long-term special government bond proceeds to be spent on expanding the trade-in policies. As we covered in a previous report, the trade-in policy scope will be expanded to include electronic devices, home renovations and decoration products. This should lead to improved demand for these categories this year. The report also highlighted "new consumption" as a theme, with "digital, green, and smart" products being potential policy beneficiaries this year. There’s still a focus on improving wage growth as well as strengthening the social safety net, but few details were given on this front.

Interestingly, there was also a mention of optimising the vacation system. Currently, China's vacation structure features several long public holiday blocks with limited personal leave days for many workers. This leads to heavy congestion and price spikes during holiday periods, and uneven consumption. While there were no details, we believe that revamping the leave structure would be beneficial for tourism and leisure industries overall, as well as improved work-life balance.

On the investment side, the budget for investment was set at RMB 735bn, up from RMB 700bn last year. Tight local government finances restricted new investment last year. But the RMB 10tn fiscal package announced last November should help some local governments find more room to operate this year. We expect that resources will continue to be dedicated toward stabilising the real estate market and investing in longer-term strategic priorities including tech and green investments.

Strong tech focus signals continued fierce China-US tech competition ahead

Last year's top priority of boosting so-called "new quality productive factors" was moved from the first slot to the second slot, but remained a prominent focus.

This category highlighted that efforts to strengthen advanced manufacturing and future industries will continue. The themes mentioned included biomanufacturing, quantum technology, embodied intelligence, and 6G.

Tech competition between China and the US has ramped up in the past few years, with export restrictions and sanctions utilised in the process. Nonetheless, China looks set to continue to dedicate considerable resources to the AI race. Some focus categories were highlighted in this year's government work report as well. They include promoting the "AI+", supporting LLM development and application, and developing next-generation intelligent terminals such as AI-enhanced new energy vehicles, mobile phones, computers, robots, and manufacturing equipment.

The success of DeepSeek has awakened markets to the promise of China’s AI industry. It looks like there’s still a strong focus on the further development of new products this year.

China keeps doors open for business as world turns more protectionist

The Government Work Report typically features a section on high-level opening up to the outside world.

This year the priority remained the fifth-mentioned work task for the year, unchanged from last year. However, the language turned a little more supportive and proactive this year. This includes a goal to "actively stabilise" foreign trade and investment regardless of how the external environment changes.

There are indications that policy support for exporters will expand this year, including expanding cross-border ecommerce and logistics, as well as ramping up construction of warehouses overseas. This is particularly important in a higher tariff environment. For example, in the US case, if the de minimis exception is not cancelled, these measures could help Chinese companies continue to sell low value products of under USD 800 directly to the consumer without tariffs.

On the investment side, China kicked off an "Invest in China" programme last year. But overall, the momentum for global FDI has appeared to be quite weak. This year's Government Work Reports calls for "vigorously encouraging" foreign investment, including pilot programmes for opening up the service industry, as well as the Internet, telecom, healthcare, and education sectors. There are also calls to guarantee foreign enterprises will have the same treatment as domestic firms in procurement, regulation, and licensing.

With tariffs rising this year and the "China de-risking" theme still quite common, it remains to be seen how effective measures will be to stabilise foreign trade and investment. Nonetheless, it's a positive sign that amid rising global protectionism, China is taking further steps to open up.

Government Work Report signals confidence and sets the stage for more supportive policy in 2025

Overall, this year's government work report more or less came in line with our expectations, signalling that policymakers continue to have confidence in stabilising growth despite stronger external headwinds. The markets avoided a potentially damaging scenario where growth targets were cut to 4.5%. Maintaining 5% growth this year will need a stronger policy push, and the key targets were raised accordingly. In general, we rarely see major surprises to the policy outlook barring emergency developments. Chinese policy tends to move at an incremental pace. The key point is that things look to be moving in the right direction, with an increased focus on supporting domestic demand this year. Markets will watch closely to see how fast and how aggressively new policy measures roll out in the coming months.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Monetary Policy Inflation GDP Fiscal policy Emerging markets China Asia Pacific Asia Markets AsiaDownload

Download article