China’s Third Plenum provides little support to metals

Last week’s key Communist Party meeting failed to lay out more policies to prop up demand for metals and we expect copper and other industrial metals to decline further in the near term to reflect a softer demand outlook in China

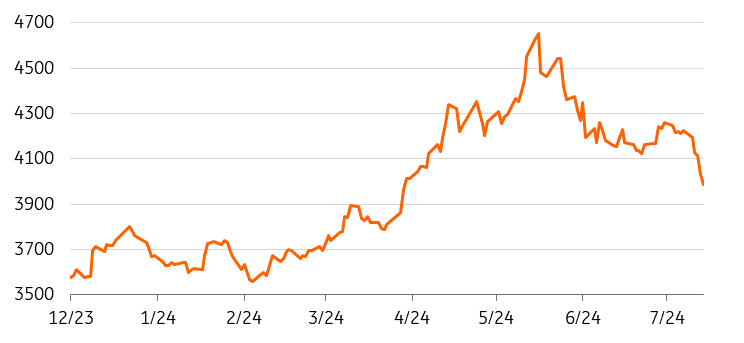

LMEX Index plunges on China demand concerns

Copper hits new three-month low

China’s Third Plenum, a twice-decade policy meeting, wrapped up last week and metal markets have been looking for signs that the government will take action to address the country’s prolonged property slump, the biggest driver for industrial metals demand.

The slowdown in China’s property sector has been a major headwind to copper and other industrial metals demand for over two years. Metal markets have been looking for signs that the government will take action during the key meeting of Communist Party officials in Beijing last week, to address the country’s prolonged property slump but the lack of short-term stimulus disappointed.

The government released a lengthy document over the weekend providing further details. For housing, the government wants to establish a system that promotes renting and purchasing, as well as boosting the construction of affordable housing. In addition, the government will give local governments more power to regulate their property markets.

However, without further stimulus measures, there is little hope for a near-term recovery for the property and construction sector. We believe the continued weakness in the sector remains the main downside risk to our outlook for industrial metals.

The LMEX Index, which tracks six base metals, plunged 5.6% last week with copper extending its retreat from a record high hit in May amid concerns over China’s weak consumption and rising global inventories.

Our China economist believes the road to the property market recovery will be long. Stabilising prices is only the first step, as unsold housing inventories remain high, and sales have been slow. As long as inventories remain elevated, new investment and building activity will remain depressed, and the drag on growth will persist.

China’s property market crisis doesn’t show signs of bottoming out yet

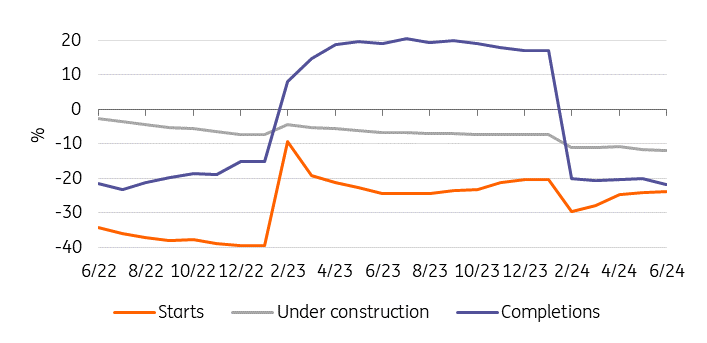

China’s property still a drag on demand

China’s commercial housing sales, floorspace starts and completions are all down around 20% year over year in the first six months of the year. The slowdown in new construction activity will in particular hurt demand for iron ore and steel, for which new property projects are the key drivers of demand.

Meanwhile, a slowdown in floor space completions remains a key drag on demand for copper and aluminium. The low level of housing starts will also continue to weigh on copper and aluminium demand looking ahead, given the lag between starts and metals usage. A recovery in completions usually lags two-to-three years behind the growth in starts.

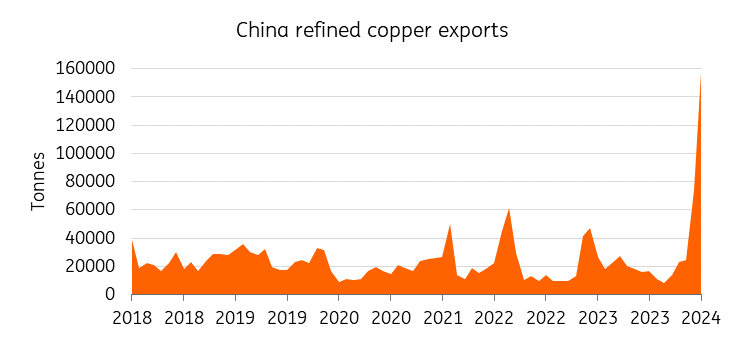

Meanwhile, China’s refined copper exports more than doubled in June, in a fresh sign of demand weakness in the country. Exports more than doubled to 157,751 tonnes in June from May, surpassing the previous all-time high of 102,000 tonnes in 2012, according to China Customs data.

China’s refined copper exports surge to a record in June

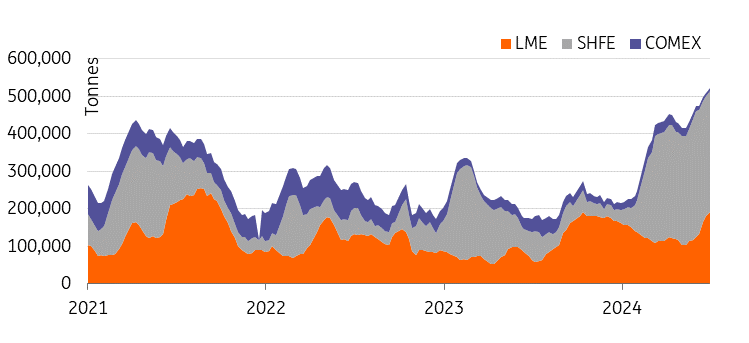

Amid a surge of Chinese exports, global copper inventories have been rising, underscoring soft spot demand in China and elsewhere. LME copper stockpiles have more than doubled since the middle of May, to the highest level since September 2021, with most of the build-up seen in warehouses in Asia. On the Shanghai Futures Exchange (SHFE) stockpiles have also surged this year and there has been no significant drawdown over the past few months, usually the peak period for copper demand.

Global copper stocks have ballooned as China exports surge

Green development remains in focus

Meanwhile, green development continues to be a priority for Beijing, with the Third Plenum calling for the promotion of green development through carbon reduction, pollution reduction, and improvement of environmental governance systems and low-carbon development mechanisms.

With China’s goals to hit peak carbon by 2030 and carbon neutrality by 2060, the green economy will likely remain a major long-term area of growth.

We believe that metals that are linked to green energy, like copper and aluminium, will benefit from the transition that China is going through as Beijing moves its focus to the new three growth drivers – EV, batteries, and renewable energy.

Beijing’s supportive policies for the electric vehicle sector have pushed the EV market share of total vehicles sales to an all-time high of 41.1% in June and sales up 32% year over year between January and June, according to data from the China Association of Automobile Manufacturers.

Copper is used in everything from EVs to wind turbines and power grids. EVs use more than twice as much copper as gasoline powered cars do. Copper has also no substitute for its use in EVs, wind and solar energy.

Aluminium is also vital in the clean-energy transition. The lightweight metal is used in wind power, energy storage and hydroelectricity. Around 30% more aluminium is used in EVs than in internal combustion (ICE) vehicles.

Looking further ahead, we believe that, as demand from the traditional sectors, like property and construction, stagnates, the increasing adoption of EVs and clean power, will drive demand growth for green metals, including copper and aluminium.

However, in the short-term, risk remain to the downside for both physical demand and sentiment, particularly related to China and the slowdown in the country’s property and construction sectors. This also means, that prices for the two metals are likely to remain volatile, responding to any changes in Chinese policies.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article