China’s outlook boosted by US trade truce and latest data

- 6 November 2025

- China

Stronger-than-expected third-quarter GDP and the US trade truce help to keep China's 5% growth target on track, but increasing dependence on external demand raises risks

China well on track for 2025 growth target

China’s third-quarter GDP growth came in stronger than expected at 4.8%, keeping the full-year growth at 5.2% YoY for the first three quarters of the year. The main drivers of growth this year are still tied to external demand, as exports and manufacturing continue to drive growth.

The data so far shows that barring a sharp collapse in fourth quarter data, growth looks likely to achieve this year’s “around 5%” target. A dramatic slowdown doesn’t look likely, despite an unfavourable base effect for the fourth quarter.

The recent meeting between US President Donald Trump and Chinese President Xi Jinping marked a major milestone in what has been a period of friction for US-China ties. The meeting concluded on a positive note, setting up a year-long truce. In terms of the immediate implications, the successful meeting defuses the immediate prospects of another sharp cycle of tariff and non-tariff escalations and the potential economic and market fallout that would accompany it.

While there is no guarantee the truce will last for the entirety of the one-year period, the extension gives hope for more constructive ties and removes a source of major risk for November. The 10% tariff cut should improve Chinese exporters’ competitiveness in the US to some extent.

We’ve nudged our full-year GDP forecast a little higher, up to 5.0% YoY.

Solid case for more stimulus remains but rising odds for a delay into next year

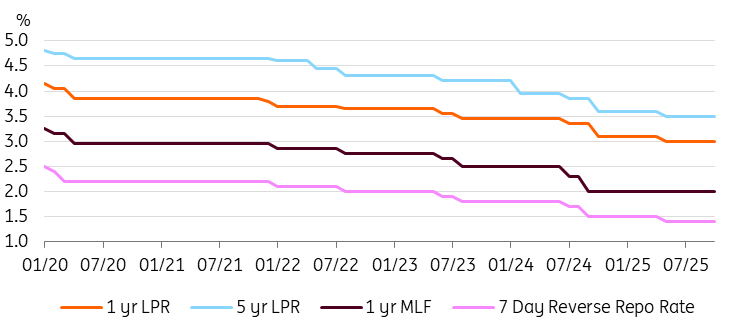

The immediate implications of stronger third-quarter data and the truce with the US on policy could be a reduced urgency for stimulus to secure this year’s growth target, resulting in an increasing possibility for further stimulus to be pushed into next year, when a new set of growth targets is unveiled. A 10bp rate and 50bp RRR remains possible in the fourth quarter, but we have pushed the baseline case for this easing back to 1Q26.

Resilient external demand should keep this year’s growth target on track, but this does not mean there’s no need for further policy support. Other parts of China’s economy, such as consumption and investment, have been losing steam in the past few months, and domestic confidence remains downbeat. China’s property prices continue to fall, which threatens the transition towards consumption-driven growth.

Rising odds of postponed rate and RRR cuts after October developments

Fourth Plenum signals China’s continued commitment to its upcoming Five-Year Plan

We got our first look at China’s 15th Five-Year Plan after the Fourth Plenum meetings in October.

China’s key focuses will remain on industrial modernisation, tech self-sufficiency, boosting innovation, and building out domestic demand. Resources will likely continue to be directed to these broader themes.

In an increasingly protectionist global economy, China is attempting to take a different path, putting a greater emphasis on expanding external cooperation through trade and investment in the next FYP. These efforts have helped China weather the impact of the trade war with the US this year, and look to be increasingly important in the years ahead. While China has historically benefited more from exports and inward investment, increasingly these flows should evolve to be more two-way as Chinese consumers grow wealthier and as companies invest outward.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: All the small things are adding up

- This bundle contains 14 Articles