What to expect from China’s Two Sessions

China's Two Sessions annual meeting is both a political and economic event. It will set the tone on geopolitics as well as on economic targets and policy direction. Here, we examine some of the key things to watch out for at the event

| 5.5%-6% |

GDP growth target expected by the market |

High GDP growth rate is not easy to achieve

The Two Sessions are the meetings of the National People's Congress, China's top legislature, and the National Committee of the Chinese People's Political Consultative Conference, the country's top political advisory body.

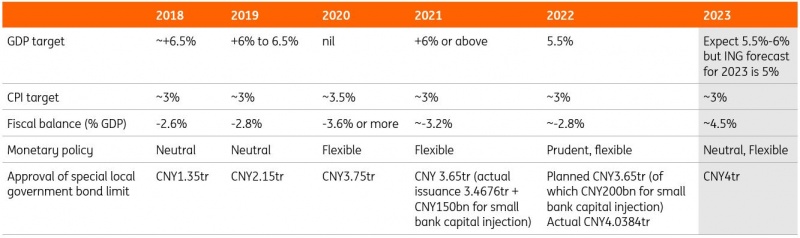

We expect that the most eye-catching target will be for GDP growth this year. It should be in the range of 5.5%-6%. This will not be easy for the government to achieve even though China is gradually recovering. The challenge will come from the weakening external market, which could affect exports and manufacturing activity related to exports.

We expect GDP growth for this year to be 5%, moving up to 5.5% if consumption and the job market are very strong.

Previous targets set by the Two Sessions

Quality growth

The Chinese government has issued a plan to attain high-quality economic growth. The plan covers almost all areas of the economy, from the quality of services to the advancement of technology, to building national brands to governance.

There are two timelines for all the achievements, one set needs to be achieved by 2025, and the other by 2035.

But the plan will not be easy to implement as it is very broad-based and also specific in terms of what 'high quality' means in each area. Each party, including government departments, local governments, and private enterprises, will have a role to play, and will therefore have to share responsibility in attaining the 'high-quality' targets. As quality is sometimes vague to measure, this could easily turn into a numbers game, which is not the central government's intention.

Achieving technology self-reliance

Recently, self-reliance in advanced technology has been a key topic at many high-level government meetings. This involves R&D funding and personnel. We believe that there will be funding from the government for both public and private research bodies to engage in R&D, with the ultimate aim of achieving self-reliance in advanced technology. Hiring more personnel from other countries may be more difficult than getting funding.

This focus on self-reliance comes amid a technology war with the US, which remains challenging for China. It is uncertain how this will damage both China and the global economy this year. The feedback effect of deterring China from having access to advanced technology in the global economy cannot be ignored, and the damage will feed back to the Chinese economy like a vicious cycle.

Infrastructure investment

We have identified infrastructure investment as the second major growth engine for 2023 while consumption is the main source of growth for the economy. The question is, when will infrastructure investment turn into actual construction activity? Unlike previous years, new issuance of local government special bonds has not been front-loaded at the beginning of the year.

So far, local government special bond issuance has been less than CNY500 billion as of January 2023, and we expect the total new issuance amount to be CNY4 trillion. This signals that the new bond issuance has been slower than in previous years. This will affect the growth of infrastructure investment as more than half of the special bonds go into infrastructure projects.

This could be related to the change in top government personnel as infrastructure planning can involve different government departments. Another reason could be that the fiscal deficit has been big at around 8%-9% of GDP in 2022, partly due to high expenses for Covid. Our concern is that the government may need to slow down fiscal spending and be very selective in its infrastructure investments. In this case, infrastructure may not be a growth factor, and China's overall economic growth could be slower than we expect.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article