China: Two Sessions sets a lower GDP growth target

This year's Two Sessions' government work report set a lower growth target, and highlights employment as the top challenge. The growth engine of infrastructure investments is confirmed. But we do not think that infrastructure investments in 2022 can replace the loss of consumption. As such our GDP forecast is lower than the government's target

| 5.5% |

GDP target |

A lower GDP target

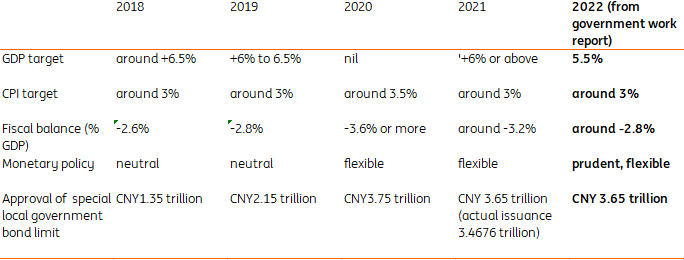

The 5.5% GDP target, a thirty-year low, implies a weaker economy compared to the 6% target set last year. The 5.5% target is still higher than our forecast of 4.8%, as we believe slower consumption growth cannot be compensated by growth in infrastructure spending.

The government work report does not point out more challenges than the previous year. It seems that it is going to handle social issues like poverty and Small and Medium-Size (SME) difficulties at a deeper level rather than just scratching the surface.

Economic targets 2022

Challenges repeat almost every year

Among all challenges, the biggest one mentioned in the government work report is employment. There will be more than 10 million college graduates this year; the number increased from around 9 million. Usually SMEs absorb some of these graduates, but it may not be viable this year as the SMEs face a difficult operating environment, and the report mentions that the government will help SMEs by increasing inclusive loans and cutting corporate taxes.

We believe that behind the government's active emploment policy objective is to support consumption, which is currently fairly weak, partly due to strict Covid measures. But the recent weak consumption also comes from a policy hit faced by technology corporates, which cut staff and bonuses, and also shrunk businesses with their upstream and downstream business partners. We expect that policy reform on technology companies are not going away in 2022.

Even the report does not mention US-China trade relationship explicitly, it highlights the independence of foreign policy. This signals if there is trade tension between China and US, China is likely to approach with a firmer stance.

Attitude towards zero Covid

The report does not clearly state that the Chinese government is going to move away from a zero-Covid approach (the official name is dynamic clearing of Covid). But it did not use "dynamic clearing" in the report. By removing "dynamic clearing" description, China could be planning to open the borders.

Growth engines come from infrastructure

Local government special bond issuance target is set at CNY3.65 trillion. Most of it should be used on infrastructure spending. The government report mentions digitalisation. This makes us believe that part of these infrastructure projects would be used on "new infra", which covers digitalisation of factory operations, full 5G coverage of the economy. "Old infra" includes renovation of old public facilities.

Private investments would contribute the most for infrastructure investments, and local government special bonds would be a supplement to the funding needs. This is because the government would like to ensure that the projects are financially sustainable.

The fiscal deficit is set at -2.8% of GDP, smaller than -3.2% in 2021 as the government would like to build a healthy public budget. Most of the fiscal spending will be passed on to SMEs and the rural regions.

Monetary policy will also help but reducing interest costs as the report points to a prudently flexible monetary policy stance. We expect policy rate cuts will continue, and the focus on SMEs means that targeted RRR cuts are more likely than broad-based RRR cuts.

The report mentions very little on the exchange rate. We believe that the exchange rate regime of managed float does not change. But as the yuan has become a safe-haven currency, it is also difficult for the government to "decide" the route of the exchange rate.

Forecasts

The GDP growth target tells it all. China will experience a slower economic growth in 2022. When we projected our GDP forecast of 4.8% and USDCNY exchange rate forecast at 6.5, we did not make the assumptions based on the current geopolitical tensions. We are considering revising these forecasts.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article