China reopening rally to drive up iron ore prices

Iron ore has rallied above $120/t at the start of 2023, rising by more than 50% from the lows of just under $80/t in early November 2022, with China driving prices higher. We have increased our price forecast for 2023 reflecting continued China reopening optimism and likely further stimulus measures

China remains key for iron ore direction

Iron ore was one of the worst-performing commodities in 2022. Concerns over Chinese macroeconomic performance and Covid-19-related disruptions were key to driving prices lower. China alone accounts for about two-thirds of seaborne iron ore demand.

The Chinese economy has slowed since the second quarter of 2022, mainly due to strict Covid measures that disrupted port and land logistics, retail sales and catering, and caused temporary shutdowns of factories in some key manufacturing locations. Even when restrictions were eased, a mixture of a weak domestic economy and high external inflation hit manufacturing in the fourth quarter of 2022. In addition, real estate developers have struggled to get enough cash to complete residential projects.

The Chinese economy expanded by 3% last year, the second slowest pace since the 1970s, according to the latest official figures. This followed zero growth in the fourth quarter. With a stronger end to 2022 than expected, our China economist has revised its GDP growth outlook upward to 5% in 2023. That is not to ignore the fact that China still faces considerable headwinds, including external demand, with recessions likely in the US and Europe this year.

In our November Commodities outlook, we said the direction for iron ore is going to largely depend on how China approached any further Covid outbreaks as well as the scale of stimulus the Chinese government unveils.

Since the release of this report, most Covid measures have been removed and the virus was officially downgraded on 8 January, when international arrivals were no longer required to quarantine. China’s abrupt exit from its zero-Covid policy and improving reopening sentiment have supported iron ore prices so far in 2023.

In recent weeks, Beijing has also stepped up policy support for its ailing property sector. In its most recent move, China is planning to allow some property firms to add leverage by easing borrowing caps and pushing back the grace period for meeting debt targets. The move would relax the strict “three red lines” policy that had contributed to a historic property downturn, hitting demand for industrial metals.

China’s property sector accounts for almost 40% of its steel consumption. That sector has been in a steep decline for more than a year amid continued tightening of housing measures across China since March when cities began to introduce a sales ban.

And although the government has stepped up its support for the property market, the effects have been slow to kick in. China’s home sales continued to slump in December. The 100 biggest real estate developers saw new home sales drop 30.8% from a year earlier to 677.5 billion yuan ($98.2bn) in December, according to preliminary data from China Real Estate Information Corp. That compared with a 25.5% decline in November.

We believe more stimulus and infrastructure spending could be unveiled at the National People’s Congress in March, which is likely to boost demand for commodities further.

Iron ore rallies above $120/t at the start of 2023

China demand likely to recover in 2023

Qu Xiuli, vice chairwoman of the China Iron and Steel Association (CISA), said earlier this month that iron ore and steel demand in China is expected to pick up this year. She told an industry summit in Beijing that demand is expected to rise in 2023 thanks to the continuous optimisation of Covid-19 prevention and control measures and the effect of policies to steady the economy.

China likely produced one billion tonnes of crude steel last year, down 2.3% from 2021, according to CISA.

Meanwhile, inventories at major Chinese steel mills slumped to their lowest levels since January last year, CISA data showed. Stockpiles tumbled to 13.1 million tonnes in the final 10 days of December, about 18% down from the second 10 days of the month, according to a survey by CISA. Crude steel production at major mills fell by 2.4% to 1.92 million tonnes a day in the last 10 days of December from the previous period.

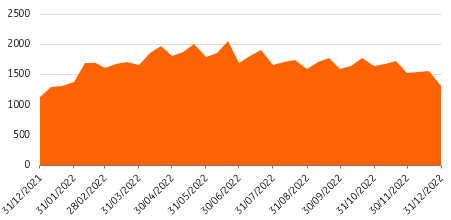

10-day inventory of key steel mills

Government scrutiny could cap further gains

Sharp price movements in iron ore have drawn scrutiny and warnings from regulators. The National Development and Reform Commission said this month that it was highly concerned about recent price changes and would closely monitor the situation. The government body also warned against publishing false market information and pledged to maintain tight supervision of pricing. Previously, government interventions to calm the markets have included subduing trading and ordering steel capacity cuts. If we see similar measures used again, this could add some downside pressure to our view.

Beijing pro-growth policy to support iron ore prices

Looking forward, we expect iron ore prices to remain supported by Beijing’s pro-growth policy stance. We have increased our 2023 iron ore forecast on China’s reopening optimism. We are still cautious for the first quarter and we now expect prices to hover around $115/t in 1Q with a seasonal lull expected during the Chinese New Year holidays later this month, when steel production usually slows down.

In the second quarter, we expect prices to rise to $120 and to $135/t throughout the third quarter, which is typically construction season in China, before edging down to $120/t in the fourth quarter.

ING forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article