China opts for eye for an eye retaliation as Trade War 2.0 breaks out

As expected, China opted for a strong response, hitting back against the US 'Liberation Day' tariffs with a 34% across the board tariff on the US

| 34% |

China's retaliatory tariffs |

As we wrote in our earlier note, the abrupt hike in US reciprocal tariffs indeed prompted a strong response from China, opting to match the retaliatory tariffs of 34% across the board. There does not appear to be exemptions in place, and the response appears to be in the spirit of an eye for an eye.

One of our key talking points since Trump won the election was that amid all the talk of China de-risking, the flip side of this is that China has de-risked the US since the first trade war. The proportion of China’s total exports to the US has fallen from around 19% in 2017 to 14.6% in 2024. While the US is still obviously a very important market, fewer firms are now existentially dependent on US suppliers or consumers compared to before the first trade war. China’s moves toward technological self-sufficiency also give China more confidence to retaliate in this latest round of trade friction.

Retaliation will hit more than agriculture this time around

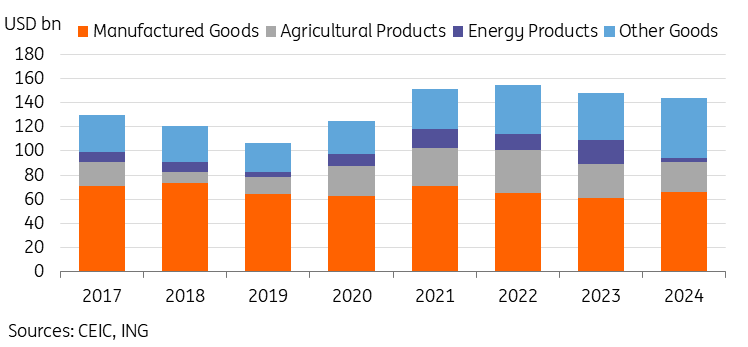

According to US customs data, US exports to China accounted for approximately USD144.4bn in 2024, with USD65.8bn of manufactured goods, USD25.1bn of agricultural goods, and just USD3.4bn of energy imports.

During the first trade war, China's response was primarily implementing tariffs on US agricultural products, which resulted in a sharp -54% year-on-year slowdown of agricultural exports to China in 2018. Overall, US imports to China fell around -18% YoY from 2017 to 2019.

This time around, it’s likely that the blanket 34% tariff will render many of the agricultural items non-competitive, and energy imports are already at quite minimal levels as well. What is less certain at this point is the price elasticity of the manufactured goods, but the biggest component is in machinery and transportation products, which will almost certainly also take a hit.

Given the US exports to China are obviously much smaller than their imports from China (USD438.9bn of goods imports in 2024), the retaliation may not have the same bite at first glance, but will likely also have significant implications on specific industries, especially the soybean industry which is heavily reliant on Chinese demand.

Furthermore, 16 US companies were added to an export control list, which bans the exports of sensitive products such as rare earths and related products. Another 11 US companies are being added to both China's unreliable entities list, which has little immediate impact but opens them up to restrictions, including possible bans on investment and trade with China. It is possible that the next phase of retaliation, if there is further escalation, will be to hit back at US corporate interests.

Evolution of US exports to China since the first trade war

Retaliation shows China is ready to dig its heels in

The retaliation should come as no surprise. The aggressive tariff hikes followed by an invitation to come and negotiate was never going to fare well in China. Trump’s hopes for a TikTok deal using tariffs as a sweetener look like a very long shot at this juncture.

As China’s Ministry of Foreign Affairs signalled last month, “if the US has other intentions and insists on a tariff war, trade war or any other war, China will fight to the end.” After earlier measured responses to the fentanyl tariffs still kept some hopes for negotiation alive, it looks like the second trade war is well under way.

A lot remains in flux, with how other countries will respond to the tariff aggression will play a huge role in how things unfold. Many scenarios remain in play.

But as for the US and China, while it’s always possible that policymakers could soon come to the table, it looks like until then, a test of endurance is underway.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more