China April slowdown shows the impact of economic uncertainty

Trade war uncertainty is denting Chinese confidence, resulting in slower economic activity in April. Retail sales and fixed-asset investment both underperformed forecasts amid heightened caution. Yet the impact on manufacturing was less than feared.

Property market softened in April as trough remains elusive

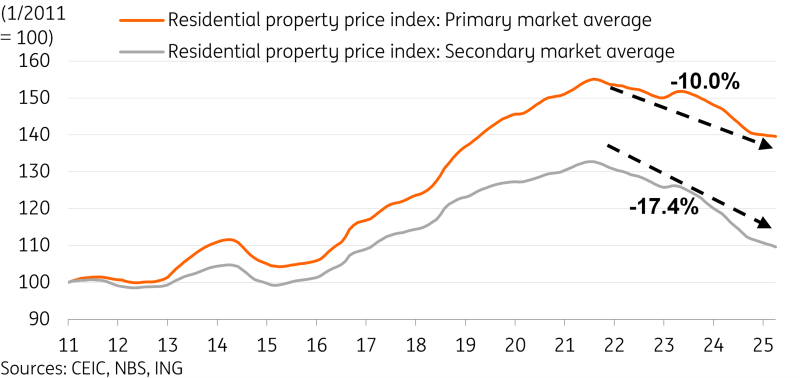

China's 70-city property prices for April continued to slide overall, with new home prices down -0.12% month-on-month and existing home prices down -0.41% MoM, both seeing slightly steeper declines than the pace in March. Establishing a trough on a national level is taking some time, as the recovery of the property market remains uneven and gradual. It's possible that tariff-related pessimism and uncertainty kept more buyers on the sidelines in April.

As the headline number suggests, April's city-level breakdown also softened a bit from March. Data showed that 25 of 70 cities saw new home prices unchanged or higher. This is a little lower than the 28 in March, but still a respectable number. Steps that could be taken to slow new supply coming to market include potentially moving away from the home pre-sale model. This could help new home prices recover faster.

The secondary market continues to underperform, with only 6 of 70 cities showing existing home prices stable or higher in April, down from 14 of 70 in March. The health of the secondary market is arguably more important in terms of stabilising domestic household confidence, as these are the assets on household balance sheets.

The 10bp rate cut in May could lower mortgages a little, and marginally help the property market recovery process. Data in recent months has showed a generally slower rate of decline. There are certainly silver linings in individual cities, but a nationwide turnaround has yet to be confirmed.

Property price decline has slowed but not yet turned around

Retail sales growth slows with strength quite uneven

Retail sales grew at 5.1% year-on-year in April, down from 5.9% YoY in March, and notably softer-than-expected on a headline level.

However, some categories showed a lot of strength. They include trade-in policy beneficiary categories, with a 38.8% YoY growth in household appliances and 19.9% YoY uptick in communications appliances. Other obvious standouts included gold and jewellery (25.3%), furniture (26.9%), and sports & recreation (23.3%). Gold and jewellery sales may have been supported by renewed interest after gold hit record highs. Furniture sales may have benefited from signs of recovery in the housing market on a city level.

Auto sales were the main exception, with just a 0.7% YoY growth in April. It’s possible that despite the trade-in policies in effect, lots of the immediate car upgrade demand has already been satisfied over the past few years. Amid the EV transition, petroleum (-5.7% YoY) continued to drag retail sales as well.

Other drags on retail sales included apparel (2.2%) as well as beverages (2.9%) and tobacco (4.0%).

The retail sales data paints a mixed picture. On one hand, it shows that autos aside, the trade-in policy has clearly been quite effective in stimulating consumption in its desired categories. On the other hand, the rest of the consumption picture is quite uneven. This indicates that while measures such as the trade-in policy indeed can help stabilise short-term consumption, a more sustainable recovery may require an improvement in consumer sentiment. This requires a broader stabilisation of asset prices and a recovery of wage growth.

Trade-in policy beneficiaries continued to outperform this year

Industrial production showed tariff impact is focused on lower end

Industrial production grew by 6.1% YoY in April, down from 7.7% YoY. It was in line with our forecasts, but IP is generally faring better than market expectations.

Many market participants expected a bigger drag on manufacturing from the tariff escalations, but, similar to the trade data seen earlier in the month, the actual impact was not as bad as feared. Within the industrial production data, manufacturing managed a 6.6% YoY increase in April.

In terms of the sector impact, textiles slowed to 2.9% YoY in April, down from 6.5% YoY in 1Q25. This is perhaps a clearer indication of the tariff impact on goods with more readily available substitution products from other countries. This development in the textiles sector is in line with our earlier arguments. Tariffs will have an outsized impact in areas where there is an easy alternative, but many products that China manufactures don’t have easily available alternatives. Exports and manufacturing of these products could stay sticky for some time.

The risk is that tariffs remain in place for a long time, and eventually, we see production offshored. But amid tariff unpredictability, not just for China but across the world, few companies will be rushing to commit resources to set up offshore manufacturing facilities. This could mean that a decent portion of China's manufacturing and exports will be less impacted than originally feared.

Furthermore, it’s possible that the tariff ceasefire could lead to an increase in activity again in the coming months. Importers may be keen to secure inventory in the event that trade talks are unsuccessful and tariffs are raised again.

Industries with easily substitutable products could take bigger tariff hit

Fixed asset investment growth slows amid uncertainty

Finally, fixed-asset investment growth softened to 4.0% YoY, year to date, which marked a larger-than-expected slowdown. Both public (6.2%) and private (0.2%) sector investment FAI growth slowed in April. This is understandable given the sudden tariff escalations causing overall uncertainty for businesses.

Manufacturing FAI also slowed slightly to 8.8% YoY ytd, though this growth level remains quite strong. The sector could continue to outperform as companies take advantage of the equipment renewal scheme.

Real estate investment unsurprisingly remained a major drag on the economy, down -10.3% YoY ytd. It will take quite some time before it recovers. Prices need to first stabilise, and housing inventories will likely need to normalise before developers consider ramping up investment.

The rate cut in May could help a FAI recover a little moving forward, but overall the more important factor remains stabilising private sector confidence.

China FAI slowed as caution prevails amid uncertainty

Caution amid uncertainty is acting as headwind

Overall, April data was a bit of a mixed bag, showing an overall moderation of growth as the tariff escalations shook global markets.

The immediate impact of the escalated trade war may have more of a direct impact on sentiment and confidence. The April data showing slowdowns in FAI and retail sales, as well as a bigger downturn in property prices, illustrates that China's private sector and households may be erring on the side of caution amid the recent volatility. While the trade war ceasefire is no doubt welcome news for many, the uncertain environment remains.

The silver lining is that, similar to what we saw with the trade data earlier this month, the actual impact on manufacturing and industrial production data was somewhat smaller than many had feared.

Reaching any sort of China-US grand bargain will remain a tall task. But greater clarity and a return to calm will likely benefit the outlook moving forward. We recently upgraded our GDP forecast to 4.7% YoY, and risks to this outlook appear to be broadly balanced at this stage.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Retail sales Property Industrial Production Fixed asset investments Emerging markets China Asia Pacific AsiaDownload

Download article