Central banks: How your views compare to ours

We ran a series of live polls at our recent Economics Live webinar earlier this week, and this is how the views of our listeners compare to our own. You can listen back to our event via our THINK Aloud podcast

On Monday 18 September, we hosted almost 500 ING customers and colleagues in a live webinar which looked at the latest central bank meetings and our longer-term expectations. We asked participants for their own views on a range of topics, and we've included the results below. We've also laid out how these compare to our own house view.

You can listen back to the event via our THINK Aloud podcast, available on our website and via Apple/Spotify podcasts.

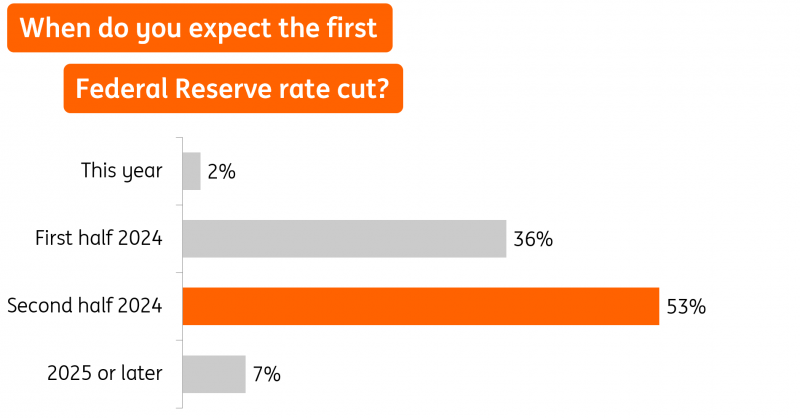

Question one

Our verdict: Federal Reserve

The US economy has certainly confounded the doubters this year with its resilience standing in stark contrast to the troubles China and Europe have experienced. Despite the most rapid and aggressive series of interest rate hikes in 40 years combined with much tighter lending conditions, the US continues to grow strongly with third-quarter GDP growth set to exceed 3% annualised. With inflation remaining above target and the jobs market still incredibly tight, the Federal Reserve could potentially hike once more this year. The narrative of “higher for longer” with regards to interest rates in 2024 is firmly in play and it is not particularly surprising that a narrow majority of respondents think the Fed will wait until the second half of next year before gradually loosening monetary policy.

We believe that interest rates have most probably peaked already and that rate cuts could start in the first half of the year. The combination of higher borrowing costs and less credit availability plus pandemic-era savings being exhausted and student loan repayments restarting should mean that households feel more of a financial squeeze in the fourth quarter and beyond. Rising credit card and auto loan delinquencies also hint at intensifying stress with the Federal Reserve’s Beige Book warning that we may be in "the last stage of pent-up demand for leisure travel from the pandemic era".

A sharp consumer slowdown, coupled with weaker hiring and poor external demand, could quickly reignite recession worries, especially if rising commercial real estate delinquencies and defaults put more pressure on the still-stressed small and regional banks. While higher energy prices will keep headline inflation elevated we continue to expect slowing housing inflation and competitive pressures to constrain core inflation, offering the Fed flexibility to respond to the threat of recession. Moreover, real interest rates will likely be around 3% in the early part of next year. By historical standards, this is high. As such even without recession, there is the argument that the Fed could bring interest rates back to a more neutral level before the second half of next year.

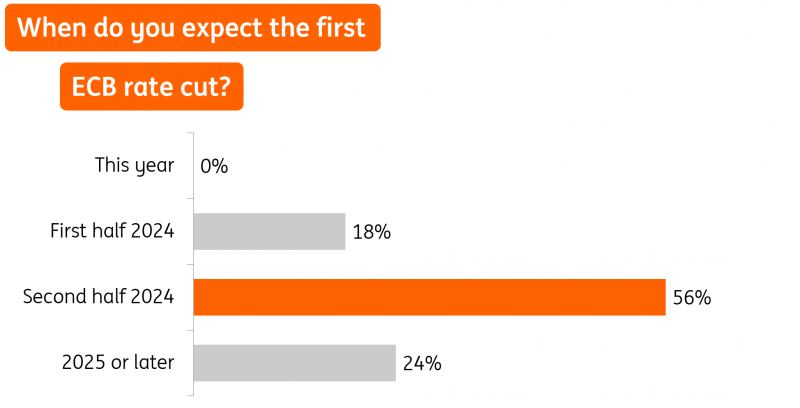

Question two

Our verdict: European Central Bank

At the September press conference, European Central Bank President Christine Lagarde said the Bank had not even pronounced the word “cut”. We don't think that will change this year. In fact, some ECB members still seem to be dreaming of a final rate hike before year-end. We think the ECB is done hiking though and similar to our webinar participants see a first rate cut at the start of the summer next year.

The September meeting was a typical ECB compromise between the doves and hawks. The hawks got yet another rate hike of 25bp while the doves got a sentence in the policy statement implying that interest rates have reached, or are very close to, the peak. This sentence stated that rates, at their current level, would substantially contribute to bringing inflation back to target. The main reason for another rate hike, despite the worsening economic picture, was a still too-high inflation forecast. The fact that inflation would only drop below 2% in the final quarter of 2025 was strong ammunition for the hawks.

When the December meeting comes, and with it a fresh round of macro projections, we think that the economy will have worsened further, inflation will have come down and the ECB’s own forecasts will have inflation at or below 2% at the end of 2025 and in all of 2026. This will be sufficient for the ECB to stop hiking. If inflation continues on a downward trajectory in 2024 and eurozone growth remains sluggish, this should be reason enough for the ECB to bring monetary policy from a restrictive to a neutral stance, cutting rates by 50- to 75bp by the end of 2024.

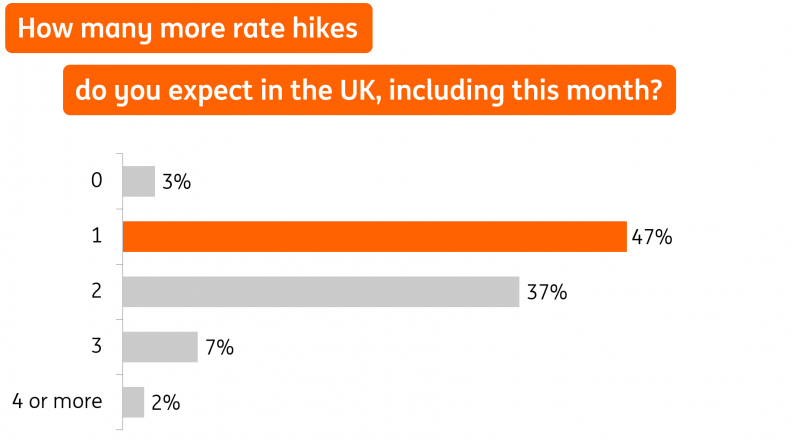

Question 3

Our verdict: Bank of England

Back at our last Economics Live in June, the audience overwhelmingly felt that the UK had a bigger inflation problem than the US or the eurozone.

Judging by market pricing, and the latest poll response from Monday's event, that view has become less fashionable over the summer. We think that's partly because it's become more evident that the trends we've been seeing elsewhere - food disinflation, lower electric/gas prices - are feeding through in the UK too. Likewise, sticky services inflation isn't confined to Britain either.

But it's also because the Bank of England itself has visibly started to lay the ground for a pause. The BoE is making no secret of the fact that the length of time rates stay high is much more important to them than how high rates go. That's a simple reflection of the UK's mortgage market, where most lending is on fixed rates, but typically for less than five years. That means the average rate being paid on mortgages will continue to rise noticeably even after the Bank has finished hiking,

Our audience this week clearly agreed that this is the gist of recent BoE messaging, and we agree with them that we'll get one final rate hike this week. We don't totally rule out another in November, especially if the next round of wage and inflation data comes in much hotter than expected. But for now, our base case is a pause in November and the first rate cut in the second quarter of next year.

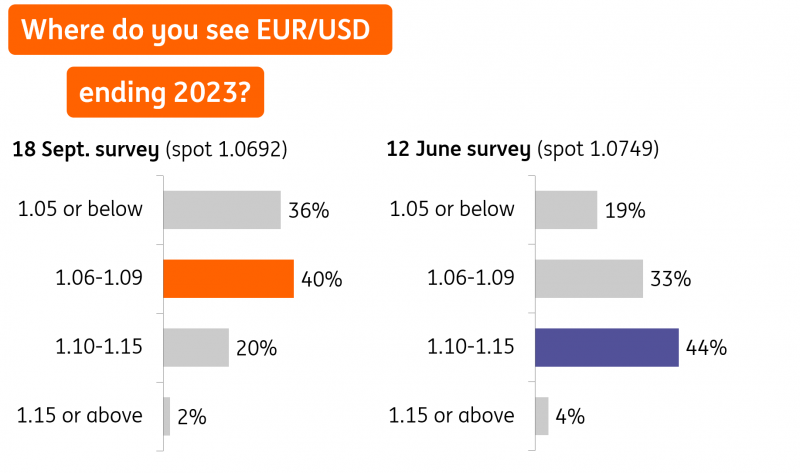

Question 4

Our verdict: EUR/USD

The clear verdict from our online polling was one of pessimism for EUR/USD. Back in June, when EUR/USD was also trading around 1.07, just about half the respondents felt EUR/USD would be stable or lower. That share has now increased to three-quarters. And those looking for EUR/USD to trade at a new low this year (below 1.05) has doubled.

Driving that EUR/USD pessimism over the last few months has no doubt been the relentless run of strong US data which has supported a continued hawkish Fed profile. At the same time, eurozone business confidence has slumped – undermining prospects of a prolonged tightening cycle from the ECB.

Where our views differ from the EUR/USD poll results is largely a function of the Fed and dollar story. We think there will be signs by year-end that tighter credit conditions are impacting the US economy and that US consumption is softening. If so, US short-dated yields will finally be turning lower in a period (November-December) when the dollar is seasonally weak.

As such, we would assign a greater probability to EUR/USD trading above 1.10 by year-end.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article