CEEMEA economic outlook: Some like it hot

Unlike Western counterparts, many economies in the CEEMEA space came into the Covid-19 crisis with relatively high levels of inflation- largely a legacy of tight labour markets. But which policymakers will be more tolerant of inflation or, in other words, will be prepared to let their economies run hot? Find out in our Directional Economics report here

The alarming rise in case rates across Europe and what they mean for the 2021 European recovery is weighing on sentiment. The good news is that we expect politicians to have largely overcome vaccine challenges this summer. Propelled by the tailwinds of better growth in 4Q20 and continued loose fiscal policy, our team remain constructive on CEEMEA growth rates in 2021.

This means that the theme of reflation could indeed make a comeback and become a pressing issue in the CEEMEA region. In fact, every country is expected to see CPI above target this year, with drivers behind those higher prices largely similar. Namely, higher core CPI, ‘re-opening’ inflation and base effects.

But the scale and persistency of those CPI overshoots, as well as CPI trends, will differ. And some countries will be more tolerant of higher inflation than others. Hungary will see the largest overshoot, with CPI likely hitting 5% in April/May. Poland will also see CPI above the upper tolerance band, but the peak will come much later.

In contrast, Romanian and Czech CPIs will be more well behaved, albeit still above target. In Russia, CPI has likely already reached its peak and should start gradually decelerating while the Turkish CPI outlook looks more challenging.

We also consider which countries are most exposed to weaker FX and higher oil prices. Here, Hungary and Turkey stand out. Turkey suffers the highest oil pass through in the region, while Hungary, among free-floating currency regimes, exhibits the highest FX pass through.

Despite high inflation, the central banks’ preferences vary. In the low yielding CEE space, the two central banks with the most worrying inflation profiles (NBP and NBH) are, and will continue to be, heavily reluctant to tighten. While the NBP is likely to get away with loose monetary policy, we expect the NBH to be forced into hikes in 2Q due to FX consideration.

We expect the CNB to raise rates later this year, despite less pressing price pressure compared to Poland and Hungary. Similar to the CBR (which has already started tightening), the CNB will hike due to its strong inflation targeting framework. But in contrast to frontloaded CBR tightening, we believe CNB hikes will be backloaded into late-2021.

Our call for CBT rate cuts in 2H21 remains unchanged, but the easing should come earlier and be more aggressive. As is likely going to be the case in Hungary in 2Q21, we do not rule out CBT tightening next quarter should the TRY need stabilising.

Lockdowns delay, but do not derail recoveries

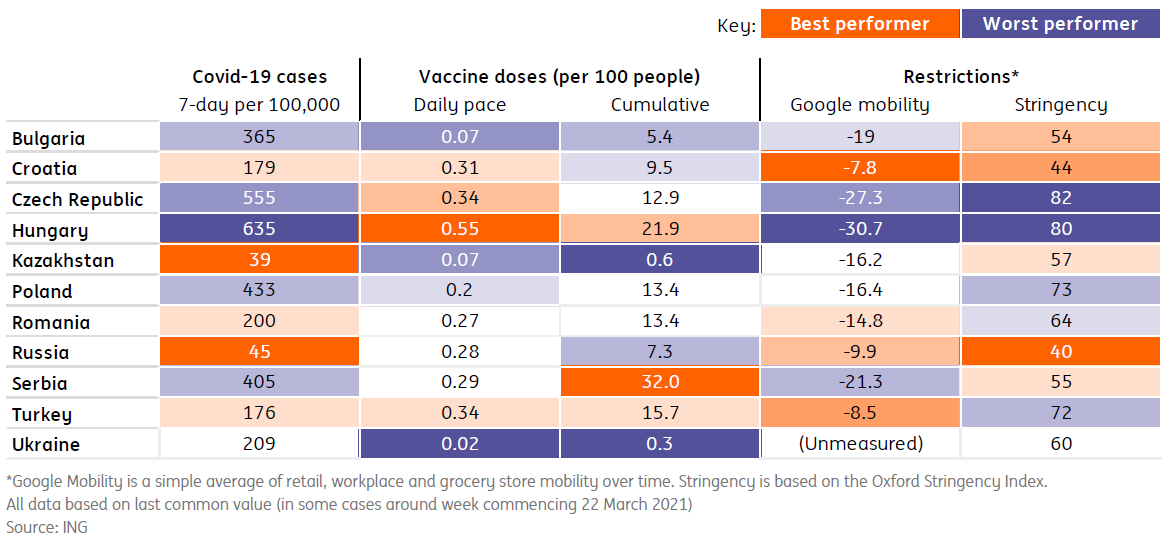

CEE economies have had varying degrees of success in controlling the virus and rolling out vaccines. Currently, the Czech Republic certainly looks the underperformer in terms of case numbers and the extent of its lockdown restrictions, though Hungary and Poland are not too far behind. As Europe has discovered, failure to roll out the vaccine has allowed vaccine-resistant strains to become more prevalent and ultimately forced policymakers into more severe restrictions. Political cycles in the CEE have also played a role in policymakers’ appetite for more stringent restrictions.

In Figure 1 we highlight the relative performance of the region based on: (1) Covid-19 cases, (2) Vaccine programmes; and (3) current restrictions.

Fig 1 - Covid-19 Cases, vaccines and restrictions - the current state of play

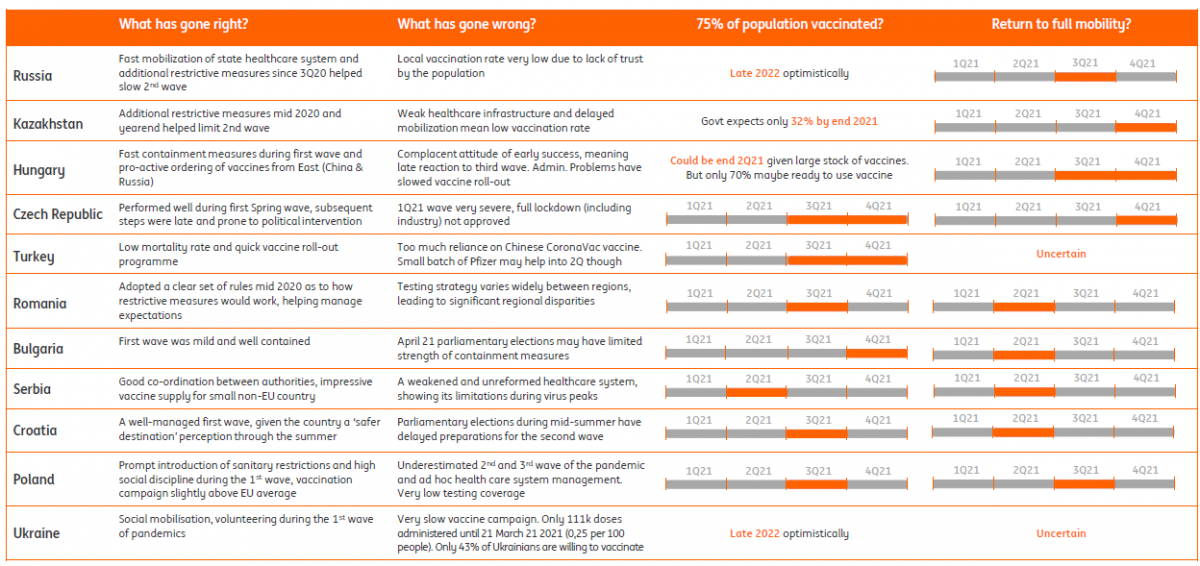

Ultimately, if vaccines are the way out of this crisis, then successful vaccine rollouts will determine when economies can return to some kind of normal. The good news here, as Carsten Brzeski discusses in a recent podcast, is that 50-60% of Europe’s population should be vaccinated by this summer, achieving a degree of herd immunity.

Within the CEE space, herd immunity looks like it will largely be achieved by 3Q21 – albeit with a few exceptions. In the infographic, in Figure 2 we showcase our best guess on when that may be achieved, alongside some of the positives and negatives in how the crisis has been handled. Southern Europe looks better positioned here with the Balkans potentially returning to full mobility as early as 2Q21.

Political cycles have played a role here as have vaccine purchasing programmes. On this latter point, Hungary stands out in being well supplied with vaccines. One of the bigger challenges across the region is confidence in the vaccine. This is particularly relevant for Russia, where trust in the locally produced vaccines seems to be slowing take-up rates.

Other challenges for the region include complacency following early successes with the first wave, and in some countries, weaknesses in healthcare infrastructure are now being exposed.

Fig 2 - Covid-19: How have countries performed and when will they re-open?

What does this mean for CEE growth?

As usual the country sections of Directional Economics provide a detailed breakdown of growth drivers but suffice to say here that the 2021 CEE recovery looks to be on track. Certainly, strong 4Q20 growth figures have provided a useful tailwind to the 2021 outlook, supported by continued loose fiscal policy and what should be the first release of the EU’s Next Generation funds.

Apart from Turkey, which had already recovered by 3Q20, we believe those countries quickest to return to 2019 levels of activity will be Serbia, Russia and Poland. Some of the last to regain those levels will be the Czech Republic and Croatia.

With most reasonably confident that a recovery can come through and doubts emerging about structural shifts in supply chains, attention has understandably shifted to inflation. We now look at the sources of inflation drivers across the region, the persistence of inflation and – the focus of this article – which central bankers will apply the monetary brakes and which will let their economies run hot.

Fig 3 - Back on their feet: CEE economies return to pre-pandemic growth levels 2Q21-3Q22

Reflation theme intact

Despite the ongoing extensions of lockdowns across Europe and CEE, the CEE reflation theme remains intact. CPI everywhere in the region remains above the respective targets, and headline numbers are set to, in most of the cases, rise further. The general drivers are similar; already high core prices, the expected ‘re-opening’ inflation in the service sector and base effects coming from high oil prices.

However, where countries will differ will be in the scale and persistency of the inflation overshoot and the direction of core CPI.

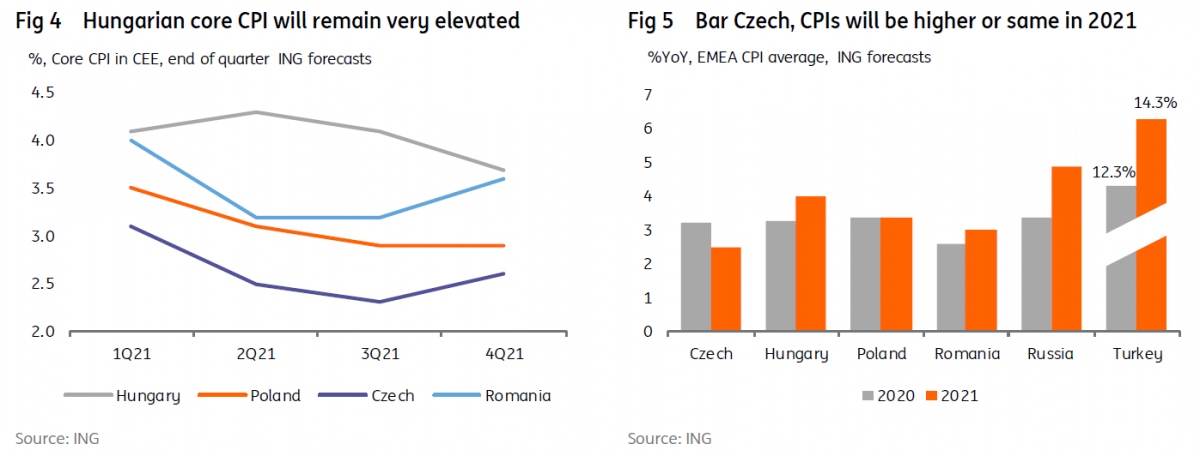

Here, Hungary stands out. The scale of the overshoot should be the most profound, with CPI possibly hitting 5% in April and May. This will be driven by one-offs (base effects coming from the oil price) as well as rising core CPI, an outcome of the local authorities running a high-pressure economy plus excise duty changes. Indeed, unlike the rest of the CEE, core CPI will remain sticky and high, above 4%, throughout most of the year (Figure 4). This is in sharp contrast to the rest of the region, where core prices should normalise from high 1Q levels. This means the headline CPI is also expected to stay persistently above 4% (the upper tolerance band) most of the year.

While Poland will also see a meaningful overshoot of the CPI target and, like Hungary, see CPI breach the upper tolerance band multiple times, the overshoot should be less profound and less driven by the core component. Peak Polish prices will also come much later than in Hungary (in December at 4% versus the Hungary CPI peak at around 5% in May).

The least pressing situation is in Romania, where high CPI in 2021 will largely be due to the increase associated with the liberalisation in energy prices, worth 0.6% this year. Without this, CPI should be at the target. Hence, the above-target CPI will be looked through by the NBR and investors, in our view.

Czech CPI should feel the offsetting factors of declining core prices on the one hand (due to base effects also stemming from VAT changes in tax rates last year), but the proinflationary pressure from volatile factors, such as a high oil price, on the other hand. This means that CPI will decline this year versus the 2020 average (in contrast to other CEE countries, where CPI will be higher or the same versus 2020 - Figure 5).

In Russia, CPI has likely reached its peak (March should be the same as the February 5.7% reading) and is expected to start gradually declining throughout the year, with a rapid deceleration at the year-end - very close to the 4% level, largely due to base effects, such as more stable agriculture prices, from here. The possible RUB volatility is a risk – although the FX passthrough from the exchange rate into inflation is relatively muted (the second-lowest in our CEEMEA basket, after PLN).

While Russia has passed beyond the peak in CPI, the Turkish CPI outlook appears more challenging. Even before the lira sell off, inflation dynamics were defined by demand conditions, elevated services inflation, the recent uptrend in commodity prices and supply constraints during the pandemic. Now with a weaker TRY, this creates further upside risk to CPI and is likely to push the peak CPI level higher (to be reached in April, in our view).

Which countries are exposed the most to weaker FX and a higher oil price?

With price pressures building across the region, we look at two possible pro-inflationary risk factors to the already elevated CPI readings: currency depreciation and a higher oil price. As is evident below, the two high CPI economies of Hungary and Turkey stand out.

FX spill over into inflation

In Figure 6, we show the estimates of FX pass-through for the region. While the FX pass-through is the highest in Romania (due to the euroization of the economy), the heavily managed nature of the currency means inflation should not be an imminent risk. Rather, among the freely floating currencies, Hungary sees the highest FX pass-through, underlying the risk to the already high CPI projections (particularly when HUF does not benefit from a current account surplus, unlike CZK and PLN).

In contrast, Poland shows a very contained link between FX and CPI, which is a clear supportive factor for the current NBP stance on the currency. One reason behind such a low FX pass-through in Poland versus Czech and Hungary is the openness of the economy, with the latter two being meaningfully more open economies (Figure 7). Russia is expected to see the second-lowest FX pass-through (which has halved over the past ten years), largely due to the inflation-targeting framework and lower Russia dependence on imported food items.

Oil price spill over into inflation

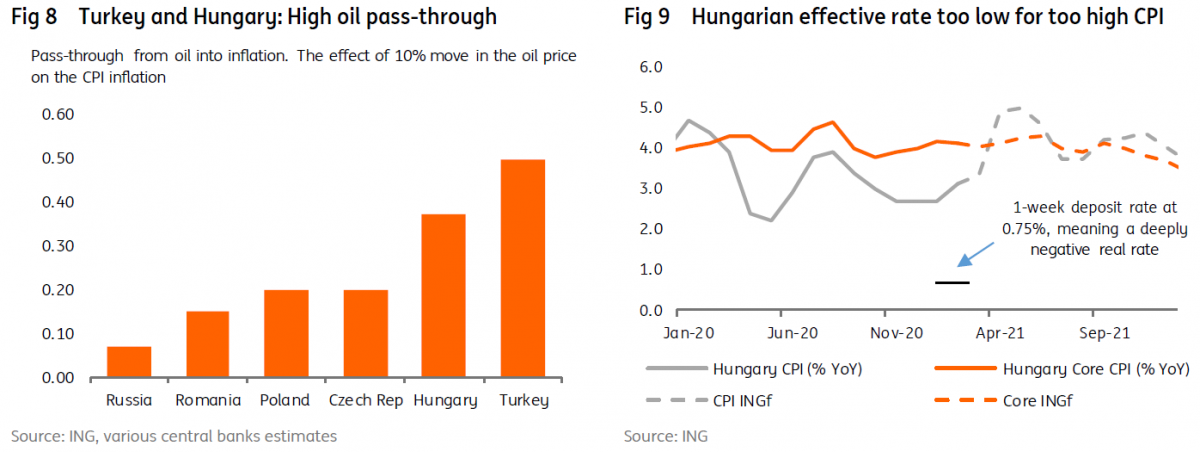

The talk of a commodity supercycle and, up until recently, the meaningful rise in oil prices makes oil another clear pro-inflationary risk factor. This will be already evident in 2Q21 numbers as oil prices will heavily contribute to higher CPI in most countries due to the base effects stemming from low prices in 2Q20). Again, Hungary appears one of the most vulnerable here, showing the second-highest oil pass-through in the EMEA region (with the difference quite large when compared to its CEE peers), as per Figure 8.

This is likely due to the specific tax situation (high VAT of 27%), FX volatility and a less energy-efficient industrial sector. Turkey exhibits the highest oil pass-through, due to the increasing natural gas intensity of the Turkish economy and rising share of oil products in the consumer basket. In contrast, Russia CPI exhibits relative insulation of CPI from global oil prices through dampening mechanisms and direct price controls.

Central banks: Some prefer to run the economies hot, some are/will be pre-emptive

Despite clear upside price pressures in the region, central bank preferences vary and their reaction functions differ. In the low yielding CEE space, the two central banks with the most worrying inflation profiles (NBP and NBH) are heavily reluctant to tighten. The clear preference is to run the economy hot, with financial stability risks being the most likely impetus to hike, in our view. We think this will be the case for Hungary, where we expect the NBH to deliver FX stabilising hikes in response to the projected currency weakness in 2Q21.

In our view, a sharp spike in CPI in April and May is likely to lead the market to question the appropriateness of the policy stance (Figure 9). While the NBP will also face a rather pressing inflation outlook, the lower likelihood of currency pressure (unlike the HUF, the PLN benefits from a sizable current account surplus) and the negligible FX pass-through into CPI (Figure 4) mean that Polish Zloty weakness: (1) is less likely; (2) will have a lower implication for the CPI profile. This should give the NBP some breathing room to avoid tightening. Importantly, the central bank has a clear preference for zloty weakness, with a lower risk of a disorderly sell-off given the discussed current account surplus.

While the NBH is likely to be the first central bank to hike in the region (being forced into it by circumstances rather than hiking willingly), the most fundamentally hawkish CEE central bank remains the CNB. Although CPI pressures are not as pressing as in Hungary and Poland, the inflation-target minded CNB should start the tightening cycle later this year – we look for two hikes in 2Q21 and three in 2022. In Romania, the NBR is to remain on hold. Although, CPI will be above target, it will remain comfortably in the tolerance band, with the main reason behind the target overshoot this year being the spike in energy prices (which will be one-off). This should give the NBR clear comfort to remain on hold.

In contrast, the CBT and the CBR have already started the tightening cycle, albeit for different reasons. While the CBT has been forced to deliver a meaningful tightening to stabilise the currency (and more could be on cards given the unfavourable perception from the global investment community of the latest personnel changes within the CBT leadership), the CBR appeared to be pre-emptively reacting to the upside surprise to domestic inflation. We expect the CBR to continue tightening by delivering at least two additional hikes over the next three meetings (by July) with risks skewed to four hikes by the end of 3Q21. Deterioration in the US-Russia relations has introduced the risk of emergency rate hikes, albeit this not our base case. In the case of increased pressure on RUB, the CBR may opt to suspend FX purchases (instead of hiking rates) – as has been the case previously, such as during the 2H18 pressure on RUB.

As for CBT, the recent TRY sharp sell-off and the risk premium attached to TRY assets may warrant further tightening near term in order to stabilise the currency. As before, we look for some eventual reversal of the tight monetary stance in the second half of the year, but compared to our prior expectations, this may now start earlier (July versus October) and could be more pronounced

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article