Car market update: Full speed ahead in the run up to 2024

The auto sector maintained momentum throughout 2023, which pushes sales an expected 8% higher. We think that order books and underlying demand will still bring positive developments next year, too. There are signs of a slowdown in electrification but intensified competition and lower relative prices will push the trend forward, with China in the lead

Global car sales forecasts on the rise

Light vehicle sales saw a strong rebound in 2023, reflecting a demand overhang from previous years which were disrupted by the Covid-19 pandemic and supply chain interruptions. We expect that the European and US markets will achieve double-digit growth this year, with global light vehicle sales growing by approximately 8% in 2023. The outlook for the next year is less certain – but after a few years of subdued production, we still currently expect modest growth in 2024.

Following such a notable bounce, we expect that next year’s rate of growth will moderate to 2-3%, with the three largest auto markets – China, the United States and Europe – all growing within that range. We expect a more balanced picture between production and sales in 2024, reflecting greater synchronisation between supply and demand next year.

Global car sales rebounded in 2023, level remains lower than pre-pandemic

Global light vehicle unit sales (in mn units)

What are the risks to our base case for 2024?

While our expected rate of global car sales growth of 2-3% in 2024 looks relatively modest, it still implies an expansion of the market. In our base case, the three key auto markets will avoid severe economic contraction. However, the main risks include the worsening of labour markets in combination with further deteriorating consumer confidence, renewed supply chain disruptions and/or further escalation of geopolitical tensions.

We will be watching out for any signs of consumer demand slowing due to the overall economic climate or as a result of diminishing purchasing power in combination with higher financing costs. Heading into the new year, order books still seem well-filled and replacement demand from corporate fleets is set to remain relatively strong. On balance, however, we feel that there is a greater downside rather than upside risk to our otherwise benign outlook for the auto sector in 2024.

Electrification is progressing, but signs of a slowdown also appear in 2023

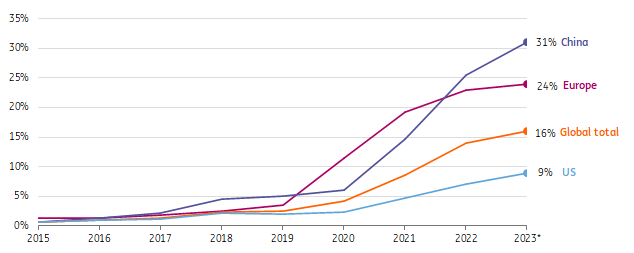

The process of electrification continued to progress over the course of this year, with China leading among the three key regional auto markets and the share of the country’s new energy vehicle sales exceeding 30% in the fiscal year of 2023.

In Europe, battery electric vehicle (BEV) and plug-in hybrid electric vehicle (PHEV) sales reached 23% of total car sales in the first nine months of this year (including the BEV share of 15%), although differences between countries are on the rise. In the US, the penetration rate is lower – still below the 10% level, but also gradually increasing year-on-year. We had, however, anticipated a slightly stronger acceleration this year. Automakers experienced a slowdown in the pace of ordering growth for EVs amid higher finance costs (EVs are often financed via private lease as this includes residual values), along with a higher number of people waiting for new more affordable models and concerns rising over charging opportunities for a large group of potential EV drivers who don't have access to home-charging options.

Expansion of EV-shares continues, but slows, particularly in Europe

Share of electric vehicles (BEV + PHEV) in total new car registrations per region

Intensified competition and more attractive pricing helps electrification

In Europe, the uptake of electric cars seems to have reached an intermediate phase. Those able to regularly charge at home and those eligible for fiscal support are already driving electric cars. This is also increasingly the case in the US, where longer mileage plays a more important role in day-to-day car usage. Businesses continue to push electric driving for corporate drivers, but 'middle-class drivers' could spark a new wave of electrification as EVs aren’t yet on par for all.

The downward trend in battery prices is set to resume after an interruption due to higher battery material prices, which is beneficial for the comparison. At the same time, price competition has also intensified as Tesla seeks to ramp up its production volume, Chinese brands push for the European market share and incumbents urge to protect their market positions. These dynamics could lead to more attractive EV options.

Chinese brands meeting customer needs

The introduction of smaller and cheaper models could also help move the transition forward. Well-known brands such as Volkswagen and Tesla announced the market introduction of more affordable cars – but they’re not quite there yet. At the same time, Chinese brands like BYD and MG already offer more affordable models with a sufficient range (like the Korean brand, Kia). These cars are likely to meet customers' needs, which has been proved by the increasing market share in Western Europe in 2023. Potential regulatory intervention – i.e., imposing higher tariffs on Chinese brands – could change their market position. European brands also have interests in China, and Chinese cars could help the overall uptake of electric vehicles. For now, we expect the inflow of Chinese electric cars into the European market to continue.

All in all, there are (economic) headwinds, but also some tailwinds for electrification. We expect that the trend towards greater electrification will broadly continue in 2024 – although likely at a somewhat slower pace and to varying degrees among regional and national markets.

Supply chain partners face drastic changes as the markets shifts to EVs

From an industry perspective, car and auto parts manufacturers are also undergoing the process of transition of their product offerings. While there is a relative consensus from the policy and strategy perspective, the transition process is anything but straightforward. Individual original equipment manufacturers (OEMs) and auto parts manufacturers each have their individual paths and technological solutions. We believe that electrification will be a key area of operational focus for OEMs and auto parts manufacturers in 2024 and that things will remain that way until the end of this decade.

We will also be watching to see if any further technological developments – including autonomous driving and solid-state batteries – will have an impact on the electrification process and the industry landscape. Alongside the development of a full-scale electric product portfolio, production innovations such as Tesla’s 'gigacasting’ are also likely to rattle the automotive supply chain. Trade supply chains will also be recalibrated amid a new geopolitical reality, with protectionism and new regulations such as the European Commission's Critical Raw Materials Act coming into play, as well as lessons learned from the recent supply disruptions. Amid these shifting patterns, suppliers should watch the market closely and think ahead to remain relevant.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article