Bulgaria and Croatia set to join the lengthy ERM II process

- 10 July 2020

- Bulgaria Croatia

Despite the current tide in European politics to slow EU expansion, Bulgaria and Croatia are proving more integration is possible. Ultimately, the decision will be a political one and the journey to joining the euro for both countries will go well beyond 1 January 2023

News reports have been emerging overnight that a decision to accept Bulgaria and Croatia’s bids for ERM-II will be taken today at the EU finance ministers video conference.

While this is not necessarily a huge surprise given that the ECB successfully closed its assessment on the two country’s banking sectors in early June, it does stand as a bright spot and welcome development amid the gloomy Covid-19 induced socio-economic background.

Coming somewhat against the current tide in European politics to slow EU expansion, Bulgaria and Croatia are proving that more integration is possible within the EU, in the context of other politicians in Europe still contemplating Brexit example or the EU’s relatively fragmented response to the Covid-19 crisis.

We believe Bulgaria and Croatia joining the ERM-II does not mean a guarantee that the euro adoption process is now on autopilot

Nevertheless, we believe Bulgaria and Croatia joining the ERM-II does not mean a guarantee that the euro adoption process is now on autopilot as both countries still face important challenges. These might tend to be tilted towards the qualitative side for Bulgaria (institutional framework, rule of law) and quantitative side for Croatia (public finances sustainability), but the reality is that none of the two will meet all the convergence criteria anytime soon.

The Maastricht criteria

To adopt the common currency, a candidate country needs to meet four main convergence criteria known as Maastricht criteria:

- Price stability - Average inflation should not exceed more than 1.5 percentage points above the rate of the three best performing member states.

- Sustainable public finances - Budge deficit below 3.0% of GDP and the debt-to-GDP ratio remains below 60%.

- Convergence sustainability - Long-term interest rates don't exceed more than 2 percentage points of the three best performing member states in terms of price stability

- Exchange rate stability - Participation in ERM-II for at least two years

Equally important and implied by the adoption process, a fifth criteria is the legislative compatibility, as national legislation needs to be adapted to the treaties and statue of the European central bank, i.e. ensuring central bank independence and prohibition of monetary financing.

What is ERM?

ERM stands for Exchange rate mechanism and is meant to ensure that prior to adopting the euro, the candidate country can control its economy without recourse to excessive currency fluctuations.

ERM-II was introduced in 1999, together with the single currency and it is a compulsory step for the countries wanting to join the eurozone. Thus, for a period of at least two years, a country needs to demonstrate that it can maintain its currency stable within a maximum tolerance band of ±15% around a central parity rate for a period of at least two years.

Central parity rate: What is this all about?

The candidate country needs to demonstrate that it can maintain the relative stability of the currency.

The decision on the central parity rate is taken by mutual agreement of the ECB and finance ministers and central bank governors of the euro and non-euro area countries participating in the ERM. The maximum variation band around this central rate is 15%, but a narrower band can also be set.

The Danish krone, for example, has a fluctuation band of ±2.25% but for the Baltic countries, Slovenia and Slovakia the band was set at 15% band at the time of ERM-II entrance. It's worth mentioning that the central rate can be changed by mutual agreement of the parties, as was the case of the Slovak koruna which was revaluated by 17.6% in 2008.

The Bulgarian lev has been successfully pegged to the euro at a fixed rate since 1997. Croatia's case is slightly more nuanced, but essentially its rate is a quasi-peg

In Bulgaria’s case, the currency board arrangement (CBA) in place since 1997 managed to successfully peg the Bulgarian lev to the euro at a fixed FX rate of 1.95583 BGN/EUR. This has remained unchanged since then and we have strong confidence that it can be preserved in the upcoming years too until the country joins the eurozone.

Croatia’s case is slightly more nuanced than Bulgaria, but essentially its FX rate is a quasi-peg. The Croatian central bank uses the exchange rate as its main instrument to achieve price stability. Hence, tightly controlling the FX volatility is already embedded in the central bank's institutional memory and of course its policy framework.

The Covid-19 crisis came with some depreciation pressures in March 2020, firmly tempered by the central bank which allowed only for a mere 2-2.5% temporary kuna depreciation. All things considered, we believe that maintaining the stability of the kuna around a central parity rate, which we estimate to be set at 7.55 (usually the rate is set around the current market levels) will not pose major challenges for Croatia.

Challenges for the euro adoption lay elsewhere

In its latest Convergence report, the European Commission underlines that Bulgaria does not fulfil two criteria (leaving aside the FX rate stability which is currently tackled via ERM-II), namely the legislative compatibility and the price stability.

The inflation criteria for Bulgaria could prove trickier than one might imagine while the relatively high-debt-to-GDP ration in Croatia will be the main problem

While on the former we don’t expect major challenges, the inflation criteria could prove trickier than one might think. We anticipate that the future unit labour costs growth will pose constant upward pressure on inflation for many years to come, in particular in the services area. Also, in the European Commission’s words, “the relatively low-price level in Bulgaria (about 49% of the euro-area average in 2018) suggests significant potential for price level convergence in the long term”. While in the short-term (2020/2021) inflation developments might look encouraging given the expected fall in the inflation rate, we believe that these should be viewed as temporary - on the back of the volatile oil prices and temporary demand contraction. Over the medium to long run, Bulgaria’s lengthy catching-up process will -undoubtedly in our view- trigger price pressures which will be difficult to contain within the Maastricht criteria.

For Croatia, the main weakness in our view is in its relatively high debt-to-GDP ratio which we estimate to reach 86% in 2020 after years of efforts which brought it close to 70% in 2019. To some extent, the government will also need to reinforce the hard-gained credibility regarding the budget deficit, after the probable overshoot in 2020 for which we estimate a 8.0% of GDP deficit. The recent ruling coalition victory in parliamentary elections implies policy continuity, but swiftly bringing the deficit back below 3.0% of GDP could prove quite difficult, especially given the tentative fiscal relaxation plans for 2021.

In our view, Croatia looks unlikely to reduce the debt-to-GDP level below 60% before five years, however, this should not be a showstopper, or in the ECB’s own words “Member States with government debt ratios to GDP in excess of 60% are expected to bring them down towards the reference level at a satisfactory pace”.

In essence, this means that if every other criteria is fulfilled and the debt-to-GDP is credibly decreasing, the euro adoption will not be blocked.

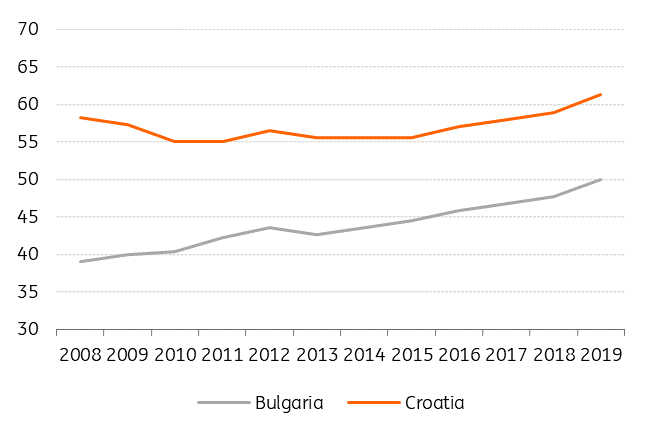

GDP per capita in PPS (% versus EU-19)

Covid-19 placed rating upgrades on ice but ERM II brings them back

ERM II entry will definitely bring rating upgrades back on the agenda.

All rating agencies consider euro adoption process as a positive (as an anchor for reforms and fiscal prudence) and euro adoption itself (notably due to the euro’s reserve currency status and with all euro-denominated debt becoming local currency debt).

Indeed, both countries have been upgrade stories in recent years thanks to healthy external balance sheets, supportive fiscal policies and structural reforms, with Croatia (Ba2 positive/BBB- stable/BBB- stable) having reached investment-grade status last year. Meanwhile, Bulgaria (Baa2 positive/BBB stable/BBB stable) had all hopes up given three positive outlooks earlier this year, but the Covid-19 outbreak dashed all hopes.

We believe that ERM II brings rating upgrades back on the cards, most likely at Moody’s given the positive outlooks and Fitch which has outlined a more formal approach:

- Moody’s is the only rating agency that has kept Bulgaria (Baa2) and Croatia (Ba2) on a positive outlook. The rating agency still expected ERM II entry to be pushed back to 2021 due to the ongoing crisis. The green light would therefore likely result in an upgrade. More positives could eventually come from the planned EU recovery fund (the initial proposal indicated c.EUR12bn and EUR10bn for Bulgaria and Croatia, respectively).

- S&P looks less likely to upgrade which has moved the outlook on Bulgaria’s BBB rating back to stable at the end of May. For both Bulgaria and Croatia, S&P needs to see an improving growth outlook or, in the case of Bulgaria, a strong external performance. We note that S&P applies a heavy penalty for Bulgaria’s monetary assessment given the currency board regime while ERM II is seen as strengthening monetary credibility over time. As a result, we could see positive outlooks coming back, with review dates on 18 September and 27 November for Croatia and Bulgaria, respectively.

- Fitch has outlined a process for the rating implications of the euro adoption process in August 2019, expecting an upgrade if a country is formally admitted into ERM II (and if it is short and euro adoption is credible), followed by another upgrade once a country gets the green light to formally adopt the euro. In the case of Croatia, Fitch has voiced some concerns on fulfilling the euro-convergence criteria, notably on high public debt. This makes an upgrade of Bulgaria more likely while there is a chance that Croatia’s BBB- rating only moves to a positive outlook.

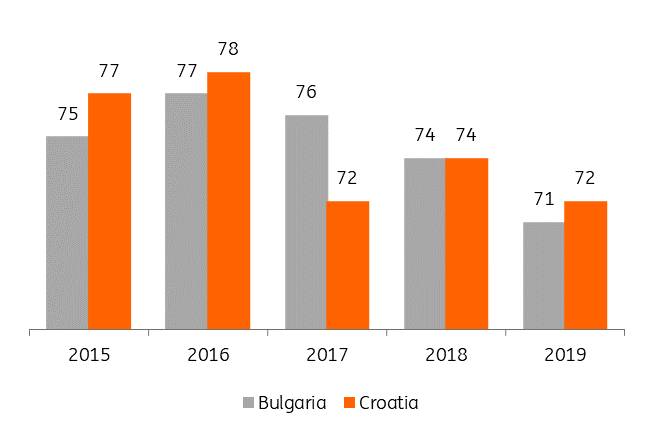

Percentage of respondents saying that the country is not ready for the euro

Seen by many as one last checkpoint before joining the eurozone, the reality is that successfully completing the ERM-II ticks only one out of the several boxes which need to be checked before adopting the euro.

We believe that both Bulgaria and Croatia will find it easier to meet ERM-II requirements than other criteria like price stability in the case of Bulgaria or budget deficit/debt sustainability for Croatia.

In the end, as with most decisions taken at EU level (e.g. Schengen area entrance, EU funds distribution/accession etc.), the final decision will inevitably be a political one and will likely take into account other aspects not specifically written down in the euro adoption blueprint, such as the rule of law, institutional strength or legislative predictability.

We, therefore, believe that the road to euro adoption for both countries will go well beyond the earliest possible adoption date - which is 1 January 2023.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: How green is your recovery?

- This bundle contains 10 Articles