Brexit: Four scenarios for trade talks and UK markets

We still narrowly expect the UK and EU to sign a free-trade agreement this year, albeit a basic one. But the chances of an extension to the transition period beyond 2020, which could have given businesses more time to prepare, looks unlikely. Expect some initial disruption to supply chains at the start of 2021 as Britain formally leaves the single market

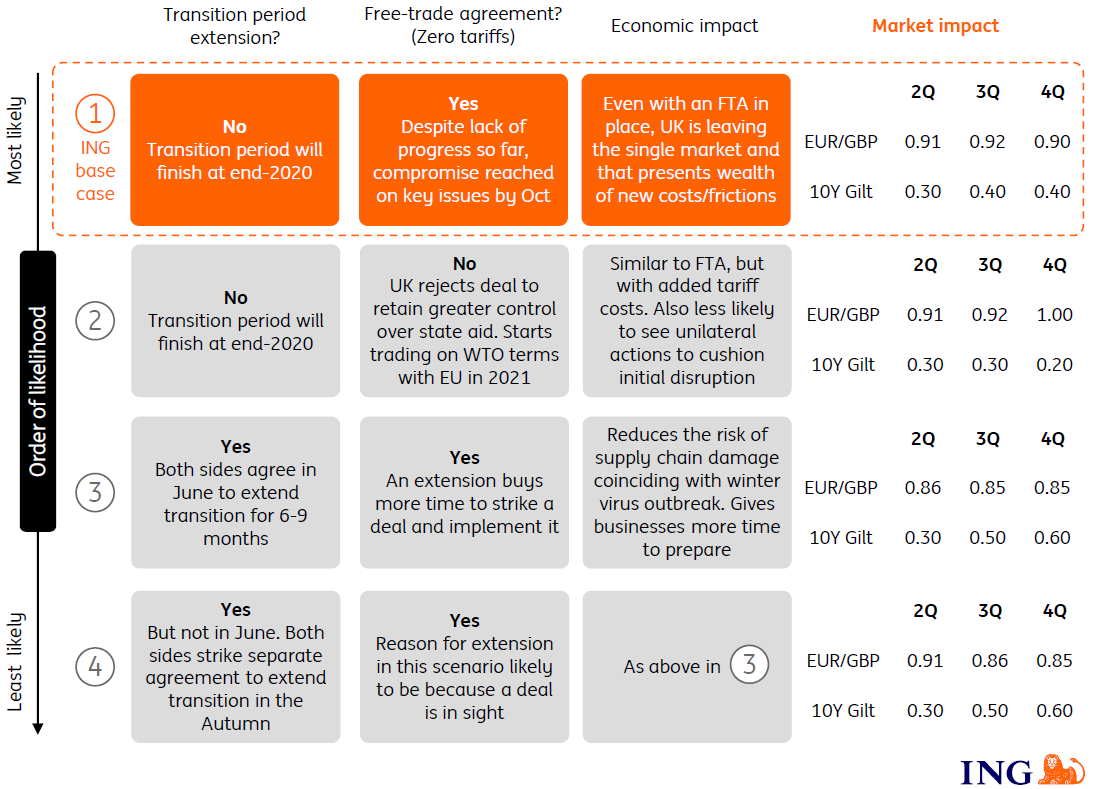

Four scenarios for UK-EU talks

Base case: Transition period not extended, but free-trade agreement signed this year

Time was already looking tight for a UK-EU free-trade agreement to be signed this year, and the coronavirus health pandemic has only added further strain. But while an extension to the post-Brexit transition period could offer negotiators and businesses more breathing space, it’s looking unlikely. Both sides have until the end of June to agree with such a delay, but the UK is adamant it won’t ask for extra time.

One way or another, that means the way the UK trades with Europe will change dramatically at the start of 2021. A trade deal could still feasibly be struck, albeit one that is pretty basic. And with scope for compromise in some areas - notably fishing - we’re still narrowly inclined to say an agreement will be signed. The conclusion of the withdrawal agreement agreed last October showed how movement can come late in the day.

The prospect of initial disruption to supply chains, owing to possible delays at ports, suggests the UK is at a higher risk of slipping into a so-called ‘W shape’ recovery, whereby growth is hit for a second time at the start of 2021

Perhaps that will prove to be optimistic, but ultimately for the economy, it matters fairly little. With or without a deal, the UK is leaving the single market, adding an array of new barriers for services. Meanwhile, even with zero tariffs, goods producers will still have to contend with plenty of new paperwork to prove where the product was made - rules of origin.

The prospect of initial disruption to supply chains, owing to possible delays at ports, suggests the UK is at a higher risk of slipping into a so-called ‘W shape’ recovery, whereby growth is hit for a second time at the start of 2021. With businesses unlikely to have the capacity to fully prepare for the changes amidst the current disruption, all of this potentially could further slow the recovery in investment and hiring from the Covid-19 shock.

No transition extension and no trade deal agreed this year

If negotiations break down, it’s likely to be over state aid.

Brussels wants the UK to maintain some alignment on EU state aid rules in exchange for tariff-free access to the European market. Britain wants full-scope to support industries in the post-virus recovery. There’s also reportedly a view in Westminster that the costs of 'no deal' have already been registered over recent weeks, and that the economic damage would be hidden by the wider Covid-19 shock.

Economically, 'no trade deal’ doesn’t look substantially different from the scenario above, given that both would see a substantial decrease in market access. Tariffs will raise additional costs in some specific industries but for the bulk of goods, the real costs come from customs clearance and the potential delays, which also exist under a free-trade agreement.

Politically though, there are some differences. A broad free-trade deal could be coupled with unilateral measures to cushion the blow at the start of 2021. That’s unlikely to happen if talks break down and an agreement isn’t reached. In the longer term, trading on WTO terms is unlikely to prove sustainable, but starting from a point of political tension makes it tricky for both sides to return to the table, either for trade or wider cooperation.

Both sides agree this month to extend transition by 6-9 months

It’s looking less and less likely by the day, but there’s still time for both sides to agree to an extension of the transition period.

That would give businesses more time to prepare for the forthcoming changes, and if an extension were to be agreed, that might be how Boris Johnson frames the decision. To be clear though, this is only postponing the inevitable economic hit. But crucially it would reduce the risk of disruption coinciding with another outbreak of Covid-19 over the winter.

Transition not extended this month, but with a deal in sight, both sides agree to a delay later on

This is undoubtedly a wildcard scenario - one that currently looks fairly unlikely. Most EU lawyers are adamant that once June deadline has passed, the opportunity to end the transition period is gone.

But with the UK set to opt against an extension this month, there’s an emerging debate on whether the situation could be fudged later in the autumn if a deal appears to be in sight. The Institute for Government has recently looked into this, and their conclusion is that the decision to extend the transition period would require a whole new agreement, that would be both time-consuming and legally complex to agree. That’s unlikely to be practical given the time available, even if the political will exists.

So as we said above, probably the best outcome we can expect is a collection of unilateral actions designed to help firms adjust initially. Financial services equivalence is a good example, but clearly none of these measures will replicate the current level of access.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

12 June 2020

June Economic Update: Hope returns despite the huge challenge ahead This bundle contains 12 Articles