Brexit: Four factors driving the risk of ‘no deal’

A 'no deal' Brexit has undoubtedly become more likely in recent days - the EU is unlikely to offer anything big, and Parliament faces an uphill battle to stop a prime minister set on exiting without a deal. But even so, an election looks highly likely - and facing voters in the early stages of 'no deal' would be very risky for Mr Johnson's Conservative Party

The risk of 'no deal' has increased

‘No deal’ Brexit is becoming more likely

When British MPs return from their summer holidays at the beginning of next month, there will be less than two months until Brexit on 31 October. Markets are becoming increasingly worried that this won’t be enough time for Parliament to block a ‘no deal’ exit – the pound has fallen by 3% against the euro since Mr Johnson became leader.

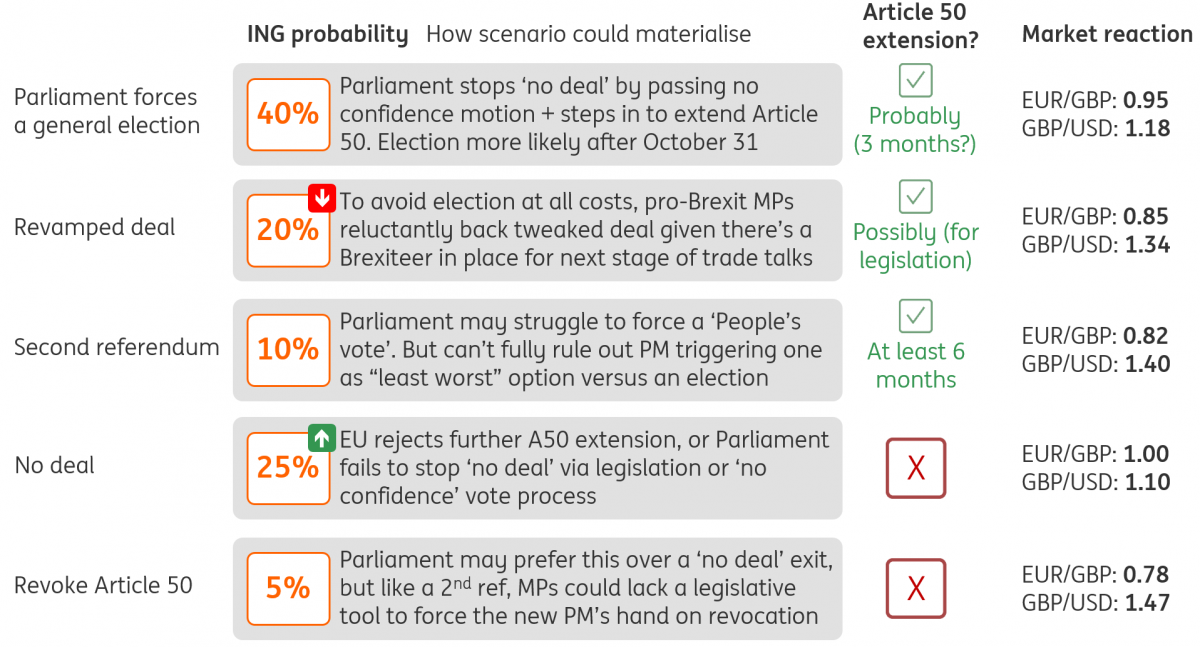

So just how likely is a scenario whereby the UK leaves the EU without a deal? We think the probability has risen in recent days - we'd now put it at 25%, maybe higher - but ultimately it all boils down to how you answer four key questions.

Will the EU offer the UK something new?

The probability of a tweaked deal passing before 31 October is decreasing. While there are a handful of changes to the current deal the EU would be prepared to offer – for instance a longer transition period or a return to the so-called ‘Northern Ireland-only’ backstop – the bar to getting them approved by Parliament is set high.

As we noted in our last piece, a deal could still pass for political reasons – for instance, if pro-Brexit Conservatives calculate that the risk of losing control of Brexit altogether has risen (in other words, that they risk losing an election). This was part of the reason why a number of Brexiteers voted for the withdrawal agreement at the third meaningful vote in March, although as things stand, a repeat scenario looks unlikely to happen again come October.

Can Parliament find a way to legislate against ‘no deal’ - or request another Article 50 extension?

Assuming a different deal doesn't materialise, then the risk of 'no deal' will very much depend on Parliament's actions and other domestic political factors.

The most obvious way of preventing 'no deal' on 31 October would be for MPs to force the government to apply for another Article 50 extension. Several Parliamentary experts think this could be both tricky and time-consuming.

To succeed, Parliament will need to make its wishes legally binding. And to do that, MPs will need to secure time in the Parliamentary agenda to force through legislation – something that’s ordinarily controlled by the government.

A recent report from the Institute for Government goes into the nitty-gritty of how this time could be secured, but the simple message is that getting control over the agenda could be hard. It would also rely heavily on the flexibility of House of Commons Speaker, John Bercow.

Will the House of Commons back a no-confidence vote in the government, and if so, is that enough to stop ‘no deal’?

If 'Plan A' above fails, then it is almost inevitable that the opposition Labour Party will put forward a motion of no-confidence in the government. But unless such a motion passes on 3 September, the day when MPs return from recess, the rules mean there won’t be enough time to hold an election before the Brexit date.

Importantly, there may not be enough backing for a 'no confidence' motion at this relatively early stage. The government's official aim is still formally to seek a revised deal with the EU, and many lawmakers may only be prepared to go down the no-confidence route if 'no deal' seems inevitable. Pro-EU Conservatives will probably also want to exhaust all legislative options before taking an action that could throw their own party out of power.

There may not be enough backing for a 'no confidence' motion in early September

But ultimately Parliament doesn't want a 'no deal' Brexit, so if Mr Johnson's government continues to talk up the possibility as we move closer to the deadline, the numbers could easily begin to stack-up in favour of a no-confidence motion - particularly given the government's wafer-thin working majority.

The problem is that by then there will probably be too little time to hold an election before October 31, so lawmakers will still need to find a way to request an Article 50 extension from the EU.

Only the prime minister of the day has that power, so lawmakers may have little choice but to try and appoint a temporary Government of National Unity, with the sole purpose of asking the EU for an extension and calling a snap election.

But this comes with potential challenges. Firstly, it's not clear whether Mr Johnson would be obliged to resign, even if the House of Commons back an alternative caretaker prime minister. Could the Queen be forced to intervene? The jury is still out on that one.

There is also plenty of disagreement over who might fill the role of a temporary prime minister - Labour are adamant it must be their leader Jeremy Corbyn, but many Lib Dem and moderate Conservative MPs have signalled they would be reluctant to back him.

If 'no deal' does happen, a failure to appoint an alternative caretaker government and therefore ask for another Brexit delay, seems like a plausible trigger.

Is a post-Brexit election really in Mr Johnson’s best strategic interests?

Put simply then, there’s no guarantee that either legislation or a vote of no confidence will be enough to stop Mr Johnson in his tracks if he is set on pursuing ‘no deal’.

We have notched up our 'no deal' probability from 20% to 25%, and even that may be a little low. In the end, it may well come down to election strategy.

Assuming an election is more-or-less inevitable, then conventional wisdom suggests Mr Johnson would fare best if Britain goes to the polls after the UK has left the EU. The theory goes that it would give him the best chance of limiting the surge of the Brexit Party at a national vote. Some Conservatives may also conclude that a 'no deal' Brexit is worth the risk if it prevents a Labour-led government and the possible break-up of their own party.

We have notched up our 'no deal' probability from 20% to 25%, and even that may be a little low

That may all be true, but an election in the initial days or weeks of a 'no deal' Brexit could be incredibly challenging for Mr Johnson's Conservative Party, given the likelihood of supply chain disruption and financial market volatility, amongst other things.

Fighting an election having left the EU with a deal could be equally challenging. The EU is unlikely to offer meaningful changes to the current withdrawal agreement, leaving Mr Johnson vulnerable to criticism from the Brexit Party in a general election campaign.

So should the government try and call an election before Brexit has happened, to capitalise on the Conservative's current lead in the polls? Don't forget that this strategy backfired for former prime minister Theresa May back in 2017, and it could leave Mr Johnson open to accusations of failing to live up to his promise of leaving Europe by 31 October.

Perhaps then, the best strategic outcome for Mr Johnson would actually be if Parliament forces an election and Article 50 extension upon him. This would allow him to campaign on a tough Brexit stance, without risking the economic impact of a pre-election ‘no deal’. It would also allow him to tell voters that he didn’t want this election or delay, and attack the opposition that for trying block Brexit from happening.

Our conclusion

Of course, there's plenty of uncertainty surrounding all of this and we suspect we'll be revisiting our probabilities frequently over coming weeks. But for the time being, we think the most likely scenario is one where Parliament back a no-confidence motion and force an Article 50 extension at some point in October, setting the scene for a general election in late November or December. We’d put a 40% probability on a general election taking place, coupled with a further Brexit delay.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

14 August 2019

In case you missed it: Fear factor returns This bundle contains 9 Articles