Brazil: The hawks are getting louder

The Brazilian central bank is likely to move the policy guidance needle decidedly in a hawkish direction at this week’s monetary policy meeting, but we don’t expect a rate hike or a pre-commitment to a hike in March. A first hike is more likely in 2Q, when 2022 becomes the targeted calendar year in a policy-relevant horizon

A clear hawkish shift in the policy guidance

This week’s monetary policy meeting in Brazil, on Wednesday, was not supposed to be particularly controversial.

The current policy stance suggests that the central bank is unlikely to change the policy rate anytime soon. But this guidance contrasts with the ominous language used in the local market to describe recent inflation prints and the country’s inflation outlook.

A reluctance by the central bank to tighten Brazil’s monetary policy stance is justifiable by the fact the bank considers that ongoing price pressures are likely to be temporary. Moreover, inflation expectations for 2021-22 are anchored and the economy is still demanding an extraordinary level of monetary policy stimulus.

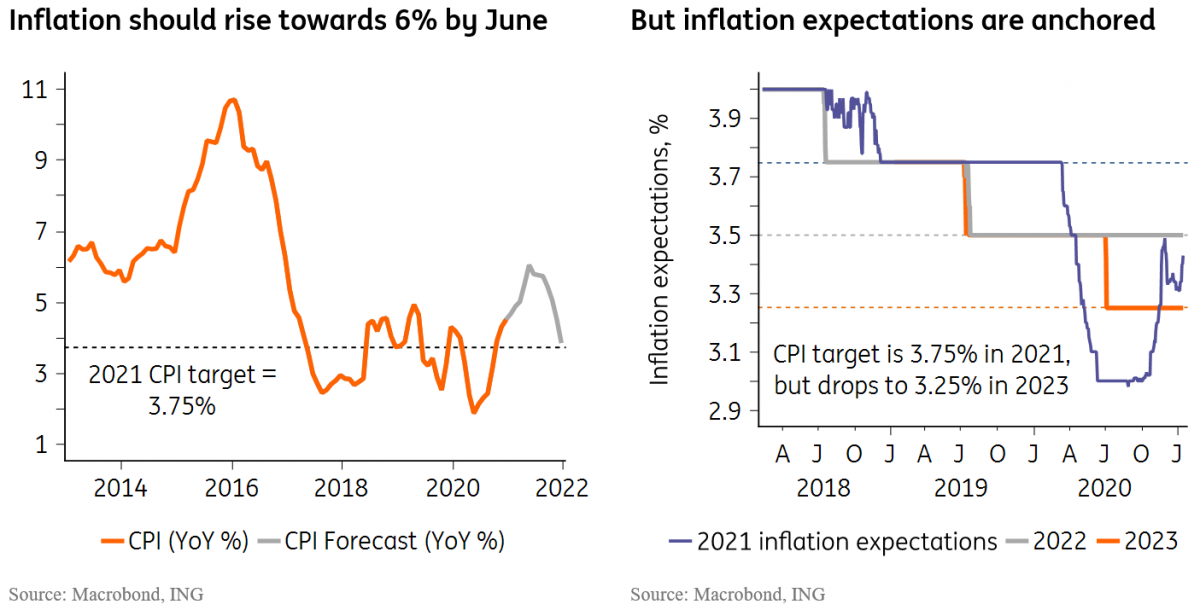

Having said that, higher-than-expected inflation prints and the expected rise in the yearly inflation print throughout 1H, which could reach 6% by June, should make it increasingly difficult for the central bank to resist rate hikes.

The pledge not to hike rates has outlived its usefulness

This week’s meeting will serve to align the policy guidance with this new inflation reality. In practice, this will mean officially abandoning the forward guidance that was introduced in August 2020.

At the time, the forward guidance was seen as a worthy experiment, the apparent next step once the SELIC policy rate had reached what many considered its effective lower bound, at 2.0%.

It’s not clear, however, to what extent the announcement was successful at shaping inflation expectations or flattening the local yield curve, which has remained remarkably steep in recent quarters.

Initially, the apparent lack of credibility in the central bank’s pledge not to raise the policy rate from 2.0% could be blamed on the rise in fiscal uncertainties, amid the threat of potentially disruptive legislative decisions at the end of 2020, which did not materialize.

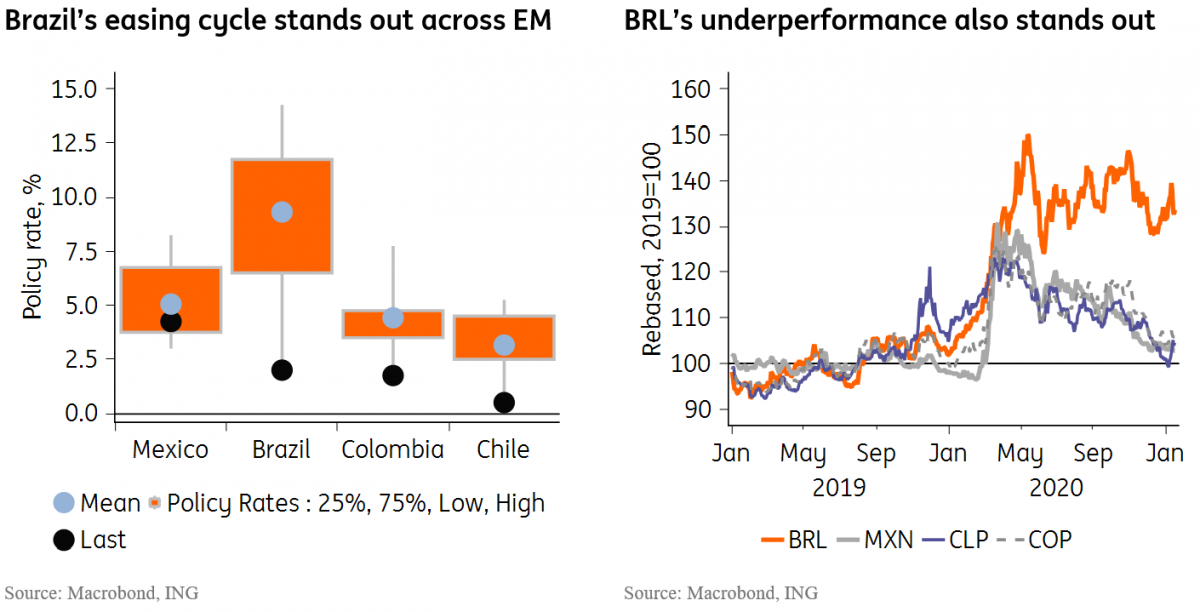

But many also questioned the bank’s decision to cut the policy rate so dramatically below its previous historical low, in what was probably the deepest easing cycle across EM majors. This altered incentives in local markets and triggered major adjustments, especially in FX markets.

The Brazilian Real’s underperformance, which, to a large extent, has been driven by the sharp decline in the policy rate seen since mid-2019, has also become a growing source of concern and, possibly, another important catalyst for policy decisions.

We see a rate hike in 2Q as the most likely scenario

These longstanding questions regarding the monetary policy stance gained sway in recent months, as inflation rose, which some saw as vindication of their views that BACEN had adopted an excessively dovish stance that proved to be disruptive and, ultimately, unsustainable.

In any case, exiting the forward guidance this Wednesday will require savvy rhetorical skills by monetary authorities. We suspect officials will try to introduce a hawkish tilt without generating market expectations of a frontloaded and extended tightening cycle.

In practice, that calibration should be done by signaling a first rate hike for the May 5 meeting, instead of March 17. The post-meeting statement should indicate that the end of the forward guidance does not “mechanically imply interest rate hikes”. But, in our view, the main justification for the delay would be the fact that it is in 2Q that the bank will start weighing 2022 as the most relevant calendar year in a policy-relevant horizon.

The fact that 2021 inflation expectations are below the target, i.e. at 3.4% compared to the 3.75% target, is a clear obstacle for the bank to justify moving sooner. Having said that, the case for a first hike in March would strengthen if CPI and FX trends deteriorate much further until then. Concern about the rise in some commodity prices, notably oil and grains, has been highlighted by some officials lately.

The other element of that calibration would be to signal a very gradualist pace for the eventual tightening. We suspect authorities will signal 25bp as the preferred adjustment pace, which contrasts with the larger adjustments priced in the local yield curve.

We expect 3.5% to be the ceiling for the SELIC rate in 2021

If we are right, this means that the SELIC rate trajectory has a ceiling of 3.5% in December 2021, which should increasingly become the consensus among analysts. This compares with the 300bp in hikes, to 5.0%, implied by the local yield curve.

Uncertain recovery calls for a gradual policy tightening

The case for a very gradual rate-hiking cycle should rest on the central bank’s belief that ongoing price pressures should prove to be temporary and the fact that the outlook for the economic recovery remains far from certain, and still require an extraordinary level of monetary stimuli, especially in light of the sharp fiscal contraction that is planned to take place in 2021.

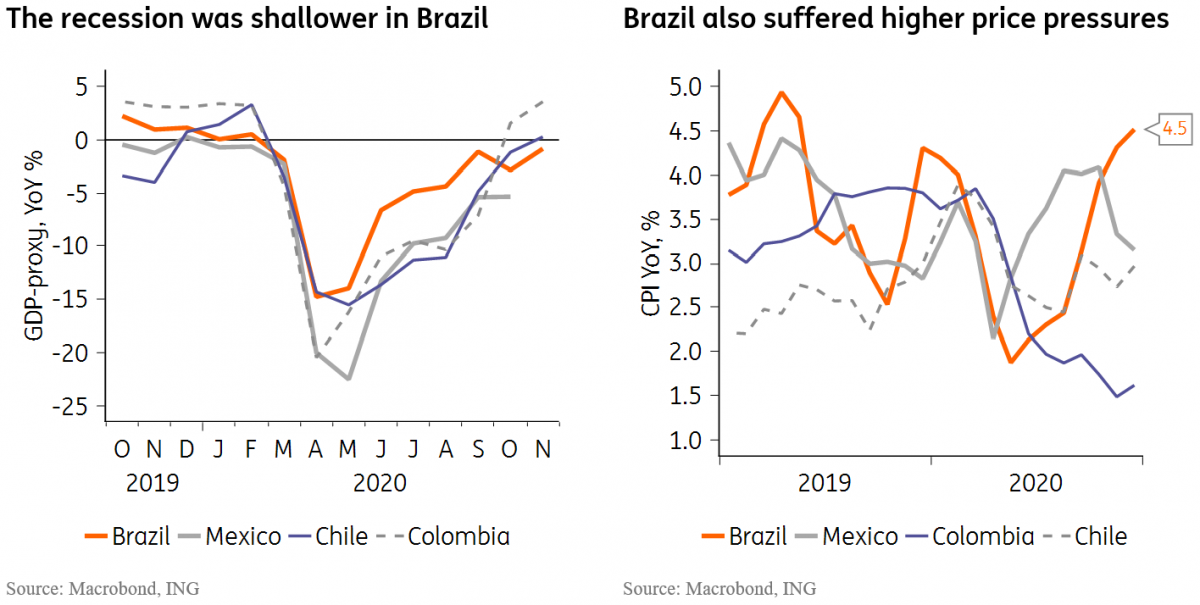

As seen in the charts below, Brazil had a faster recovery and, perhaps not coincidentally, higher inflation than its regional peers. The sharp increase in income transfers, together with Covid-related consumption and supply disruptions, were likely a key driver behind the rise in inflation.

For 2021, Covid-related disruptions should ease as vaccination programs get under way, helping mitigate any Covid-related price pressures. Moreover, the pace of recovery for domestic demand should lose momentum, as fiscal transfers were phased out.

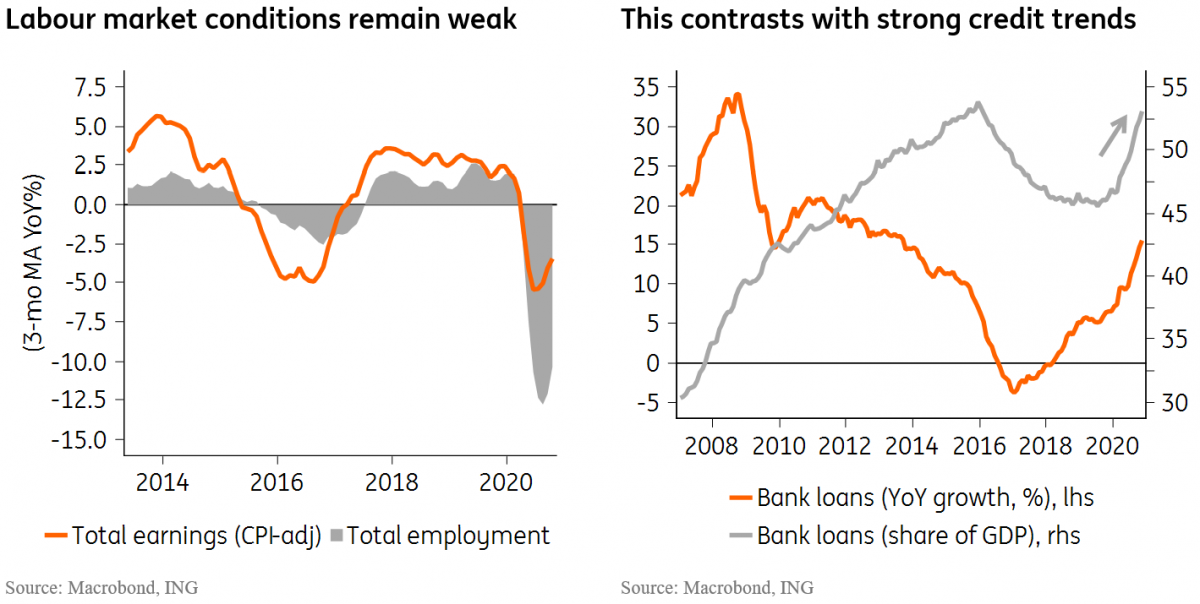

But perhaps the strongest argument for maintaining a benign inflation outlook rests on the grim labor market conditions and on the low inflation seen in the service/non-tradable segments of the economy, which are more relevant for monetary policy.

Headwinds abound for 2021’s growth outlook

The recovery has, so far, been driven by two key factors: the gradual normalization of mobility indicators, which has been particularly strong in Brazil, and the sizable fiscal income transfers that lasted from March to December 2020.

During the first half of 2021, the end of the fiscal transfers should dampen domestic demand and the continued threat that Covid-19 represents will continue to harm certain economic activities, preventing a full recovery until a critical part of the population has been vaccinated.

Our bias for GDP growth in 2021 remains generally constructive, however, with reasonable scope for positive surprises to our call for a 3.9% GDP recovery in 2021, after dropping 4.1% in 2020.

In our view, the two key drivers for the recovery going forward are: 1) the pace of vaccination, and the subsequent normalization of activities that remain affected, such as services, and 2) the monetary stimulus that should help foment a credit-fueled recovery, but that depends on continued commitment to fiscal responsibility.

The pace of vaccination is perhaps the most critical uncertainty. The government’s success in securing the importation or production of the amounts needed to immunize the population remains hard to ascertain. So far, less than 2% of vaccines needed to immunize the population have been made available to states.

The key risk here, which is not our base-case scenario, would be if failure or delay in the vaccination campaign triggers political pressure to re-enact another round of fiscal stimulus. Additional strain in fiscal accounts would hamper investor confidence, increase market volatility and push monetary authorities to tighten the policy rate in a more front-loaded fashion.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article