Brazil: Monetary easing on track

Low inflation, subdued activity and continued fiscal consolidation progress bode well for another 50bp policy rate cut this week. An additional 50bp cut that brings the SELIC rate to 5% in October is also likely, but we expect a mid-cycle pause after that. FX concerns would be a primary reason to pause, to better assess policy implications

We expect another 50bp rate cut this week

Central bank officials concluded their last policy meeting, which re-launched a relatively frontloaded easing cycle, suggesting that “the consolidation of a benign outlook for inflation should allow for additional monetary policy stimulus”.

Authorities moderated that dovish guidance by suggesting that it should not be taken as a pre-commitment to additional cuts. According to the statement, the “evolution of economic activity, of the balance of risks for inflation, inflation forecasts and inflation expectations” could alter that assessment.

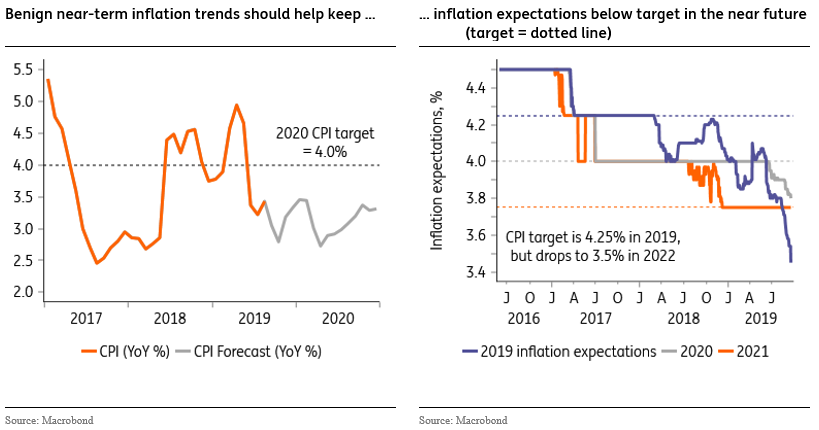

Still, by all means, inflation and activity data released since then, along with inflation and growth expectations, as captured in central bank surveys, suggest that the inflation outlook remains benign, or even improved since that meeting.

In large part that stems from the lower-than-expected inflation prints seen lately. Since that July 31 meeting, two monthly CPI prints were released, which helped bring 2019 inflation expectations down from 3.80% to 3.45% now. 2020 expectations also fell, by a smaller 10bp to 3.80%, but this is significant given that the 50bp cut on July 31 was somewhat larger than consensus. Moreover, we continue to see additional downside for those projections, as they compare with our own forecasts of 3.33% for 2019 and 3.40% for 2020.

Activity data was somewhat more constructive, especially the faster-than-expected expansion in some domestic demand data, which added a slight upside bias to 3Q GDP data, and to our expected 0.9% GDP growth estimate for 2019. But, overall, activity prints remain mixed, and downside risks persist, especially considering the potential for a synchronised global deceleration, amid heightened external trade uncertainties.

Overall, lower-than-expected inflation, subdued activity and continued progress in the fiscal consolidation agenda bode well for an additional 50bp rate cut this Wednesday, to 5.5%.

The policy statement should continue to imply the existence of additional scope for monetary easing, but that guidance should remain conditioned on a benign evolution of inflationary prospects. We still expect another 50bp rate cut next month, which would bring the SELIC rate to 5.0%, but consider that the balance of risks points to a pause after that.

Scope for a sub-5% SELIC rate

As we’ve discussed in our previous report (The (micro-)economic revolution), questions about what is the neutral level for the policy rate have now become a central, but still poorly defined element of the central bank’s reaction function.

Although the central bank does not publicize its estimate for the neutral level of the policy rate, it has historically been considered to be very high, in the 4-5% range in CPI-adjusted terms. This is much higher than the levels prevailing across inflation-targeters in LATAM, generally estimated in the 1-2% range.

There’s growing acknowledgement however that structural changes in the local credit markets that have been implemented since the end of the Dilma Rousseff regime have pushed the neutral rate lower. This debate intensified since the central bank re-launched the easing cycle, and it has already triggered an incipient shift among local analysts, who now expect the central bank to cut the policy rate beyond 5.0%.

As seen in the chart below, the current level for real rates is 2.59%. Bank officials publicly state that they consider this level to be expansionary, i.e. the neutral is likely estimated by them to be at least 3%.

But, in our view, even if we take that assessment at face value, it is hard to classify the current policy stance as more than “modestly” expansionary. More importantly, the current level of real rates seem hardly sufficient to offset the contraction taking place on the fiscal policy side.

As seen in the 2Q GDP report, government consumption has become and is likely to continue be a drag on economic activity in the foreseeable future. Unless Congress decides to weaken the fiscal framework by, for instance, changing the fiscal spending ceiling, which seems unlikely in our view, fiscal policy will add a clear hawkish bias to the policy mix in the coming years.

That drag is heavier when considering the deep contraction taking place in the balance sheets of public sector banks. And, as we discussed here, that reorientation of public bank policies deeply alters the medium-term outlook for monetary policy in Brazil.

One reason for that is the fact that the local financial market used to operate essentially as two separate segments: one for borrowers that had access to subsidized state-bank funding, including through the now-retired TJLP rate, and one for the rest of the economy.

This distorted the central bank’s policy rate decisions. In particular, given that a large chunk of Brazil’s credit market had access to subsidized rates at state-banks and was, therefore, largely unaffected by monetary policy changes, the SELIC rate has, historically, had to be set at higher levels, to offset state-bank subsidies.

That has all changed now and, as a result of those changes, 1) monetary policy is considerably more effective, as a much larger share of the local financial system is sensitive to the policy rate, and 2) historical estimates of the neutral level for the policy rate are likely biased to the upside.

The second point is particularly pertinent now that the SELIC rate is reaching record-low levels and authorities try to assess the appropriate level of monetary stimulus to deploy.

Unknown FX consequences is a reason for policy caution

Even though the sections above suggest that there are strong arguments for the central bank to consider a more aggressive monetary easing path than currently priced by the market, we suspect officials will prefer to err on the side of caution after the policy rate reaches 5%.

Some hard-to-gauge consequences of record-low rates, especially over the FX market, suggests that, even if officials believe there’s room for additional easing, a temporary pause could be appropriate.

As seen in recent days, the flurry of announcements of pre-payment of external debt securities issued by local corporates, in the context of newly-available cheap domestic funding, show no sign of abating. And, as central bank officials have highlighted, this should continue to exacerbate FX outflows and add a persistent weakening bias for the BRL in the foreseeable future.

In particular, this should prevent the USD/BRL from consolidating below 4.0 in the nearer term.

Apart from the press releases announcing the pre-payment of external corporate debt, central bank data also shows that local corporates have practically ceased to rollover maturing long-term debt securities in recent months. The 12-month accumulated rollover rate of these securities reached 41% in July, which is the lowest level seen since 2003. Year-to-date, that rollover rate is just 23%, confirming that the shift intensified in recent months.

The reduction of long-term FX liabilities by local corporates is a medium-term positive development for the BRL, but it is disruptive for the currency in the short-term. And, indeed, the BRL has been a clear underperformer among its EM peers in recent quarters.

As seen in the chart below, recent FX underperformance contrasts sharply with developments in the credit/rates space. FX and local yields moved in sync during the worst moments of the 2015-16 Rousseff-crisis years, while now yields are at all-time lows while the BRL underperforms. A similar picture emerges when looking at the spread on Brazil’s 5-year CDS, which trades at levels not seen since 2013, when credit rating agencies rated Brazil 5 notches above its current BB- rating.

Also notice, in the chart above, that FX outflows are now considerably higher than during the 2015-16 crisis. In fact, outflows are the highest since 2000.

Still, regarding monetary policy, despite the considerable 8% weakening in the BRL since the July policy meeting, concerns over the FX pass-through remain muted. This reflects, among other factors, the sizable slack in the economy, which complicates the ability of businesses to pass-on the higher costs, below-target inflation expectations, and lower commodity prices, which help offset the weaker BRL.

The fact that the FX has stabilized more recently, while the currency’s depreciation against the USD is larger than the depreciation seen in the trade-weighted FX rate (given that the currencies of trading-partners also depreciated against the USD), should also contribute to limit that FX pass-through.

Moreover, the central bank has the resources and the willingness to intervene to offset episodes excessive FX volatility, as demonstrated by the bank’s recent decision to intervene by selling USDs in the spot market. The central bank had not sold USDs directly from the bank’s FX reserves since 2009, and this decision shows a greater flexibility by authorities to deploy all the tools it has – namely FX swaps, FX repo lines and spot intervention – to address episodes of FX illiquidity.

That substantive intervention firepower suggests that the instability in FX markets should be seen as temporary, which should also contribute to limit that FX pass-through.

Rate cuts could resume once FX concerns are overcome

In our view, the balance of risks favours a monetary easing cycle that is deeper than what is currently incorporated into the local yield curve. But the risk is that monetary policy officials do not sanction that deeper cycle, towards 4.5-4.0%, right away. The risk is that they interrupt the easing cycle temporarily, at 5%, to better assess the full impact of record-low interest rates.

We believe the Brazilian Real is the primary concern here. This reflects the fact that low rates have contributed to FX instability by incentivizing large-scale FX outflows, as corporates replace external funding with newly available low-cost local funding.

One-off factors such as the expected November auction of oil exploration “transfer-rights” by Petrobras are BRL-supportive. But unless/until foreign investors see consistent signs that a firmer economic recovery took hold, FX inflows should remain insufficient to help offset the outflows seen in recent months.

Having said that, the next policy steps are not set in stone. Inflation is likely to drop to very low levels over the next couple of months, possibly bottoming near 2.8% YoY in October, boosting dovish arguments inside the policy committee. Other factors that could contribute to increase the urgency of a more dovish policy outcome include persistent disappointment with GDP growth dynamics, with, for instance, GDP growth consensus dropping below 0.5% this year.

Lastly, a stronger-than-expected BRL, nearer 3.80, and dovish surprises by developed market central banks, could also contribute to push the central bank over the 5% threshold sooner than we currently expect.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article