Brazil: Inflation risks in focus

Higher-than-expected inflation was the highlight of the economic calendar in recent weeks. Near-term inflation expectations have risen, and the local yield curve steepened further, with some calling for immediate monetary policy reversal by the central bank, i.e. rate hikes. We don’t expect any material hawkish shift by the central bank, however

Monetary policy guidance is under pressure, but it’s far too soon to alter it

Tomorrow’s monetary policy meeting was not supposed to be an especially newsworthy event. But with investors eagerly anticipating material changes in the policy guidance, including a larger-than-50% chance of a 25bp increase in the policy rate at the December policy meeting, from 2.0% now, and about 350bp in accumulated rate hikes by the end of 2021, this meeting could result in material market reaction.

Market prices are clearly at odds with the latest policy guidance by BACEN. Policymakers paused the rate-cutting cycle at its last policy meeting and have yet to close the door to the consideration of additional rate cuts, which should happen this week.

But investor focus should be on the recently introduced forward-guidance language, which explicitly rules out rate hikes in the near term, so long as the fiscal framework remains unaltered and long-term inflation expectations remain anchored.

The apparent discrepancy between the policy rate trajectory indicated by the local yield curve and the central bank’s forward guidance is not as inconsistent as it first appears. This is because BACEN’s guidance is also conditional on a fiscally responsible trajectory for the government’s budget.

And given that the fiscal trajectory should not be taken for granted, as Congress considers weakening the strict constraints on fiscal spending imposed by the “fiscal ceiling”, a fiscal risk premium should be justifiably incorporated into the local yield curve.

But the recent upwards shift in the yield curve has been animated more by the rise in inflation than fiscal risks, which have, arguably, abated somewhat as political chatter about Congressional tinkering with the fiscal framework has grown more subdued.

Price pressures are likely to be considered temporary

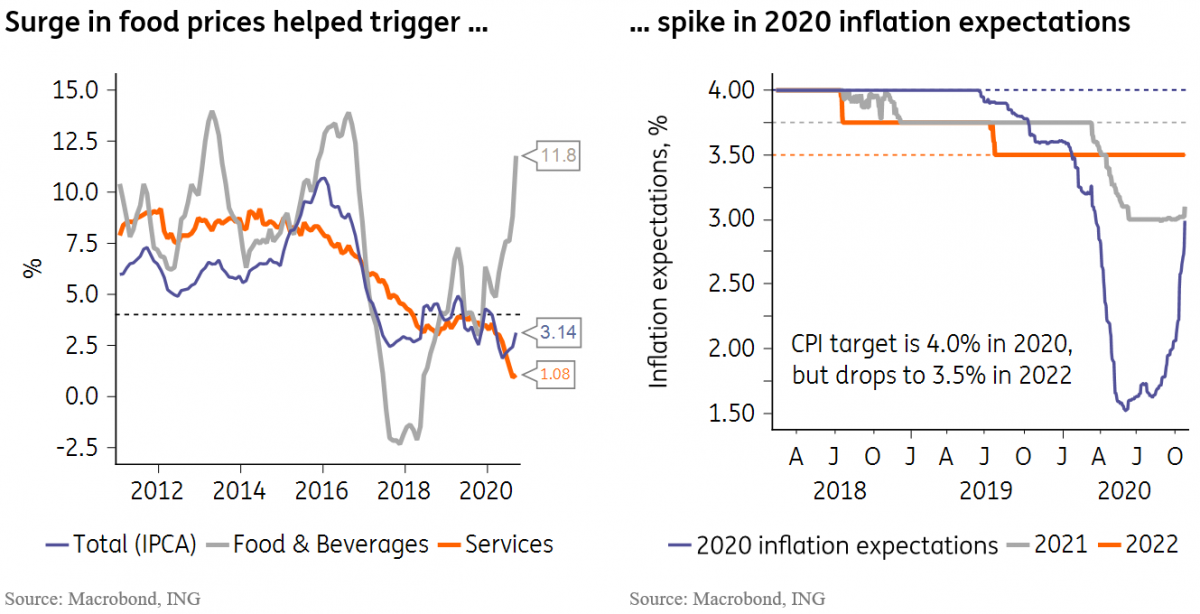

Price pressures have undeniably increased in recent weeks. As seen in the chart below, much of that is due to the ongoing surge in food prices, while prices of some consumer durables are also rising more recently.

The resulting increase in inflation expectations for 2020, seen above, is concerning, as it depicts an unexpected development regarding the outlook for inflation. But, as expectations for 2021-onwards remained largely unaltered, the prevailing assumption appears to be that the rise is likely to be temporary.

This would be consistent with an assessment that surging prices are primarily a result of pandemic-related supply restrictions, external trade disruptions, FX depreciation and the changing consumer behavior during the pandemic. While demand has increased for some segments of the consumer basket, the assumption is that consumption patterns should converge back to its previous norm once the pandemic is mitigated.

We would also highlight the fact that service prices, which have a better track-record for signaling persistent inflation trends, is printing close to 1% YoY, as seen above. This dynamic is not new and is consistent with the very weak labor market backdrop, but we suspect the pandemic’s impact on the service industry may have exacerbated this trend, which calls for caution in extrapolating the trend from current levels.

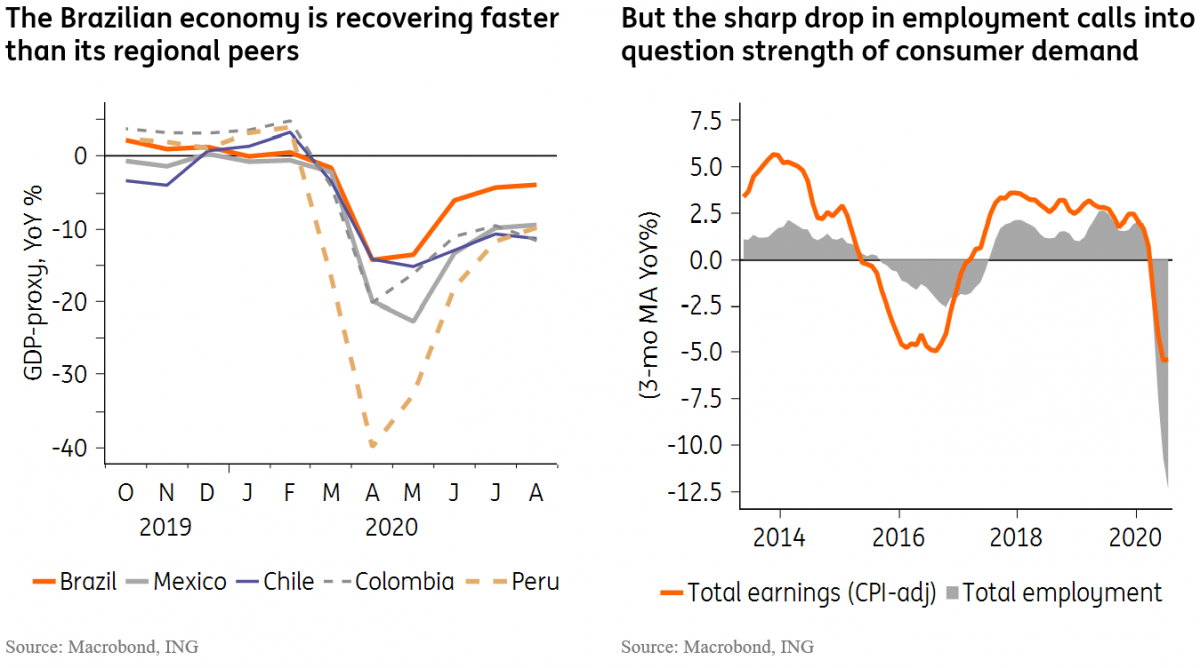

Lastly, Brazil’s economy is recovering at a faster clip than its regional peers (see chart below), but the deep contraction in employment (chart below) and the end of the household fiscal transfers in December suggest that BACEN is unlikely to turn too optimistic on prospects for domestic demand recovery anytime soon.

Overall, despite the apparent investor pressure for the central bank to alter it's monetary policy forward guidance towards a more hawkish stance, we think that well-behaved core and service price estimates along with still fully-anchored inflation expectations should allow policymakers to “look-through” the inflationary spike, characterizing the bulk of the surge as “temporary”.

Disconnect between market prices and policy guidance should persist

BACEN’s inflation assessment is likely to be, potentially, the most controversial and attention-grabbing element of tomorrow’s policy meeting. If we are right, COPOM’s assessment regarding inflation risk should be considered more dovish than currently priced in the yield curve.

We suspect the impact of a “dovish surprise” on the curve may be limited, however, as a dovish assessment of the inflation outlook may be seen as unconvincing by some investors.

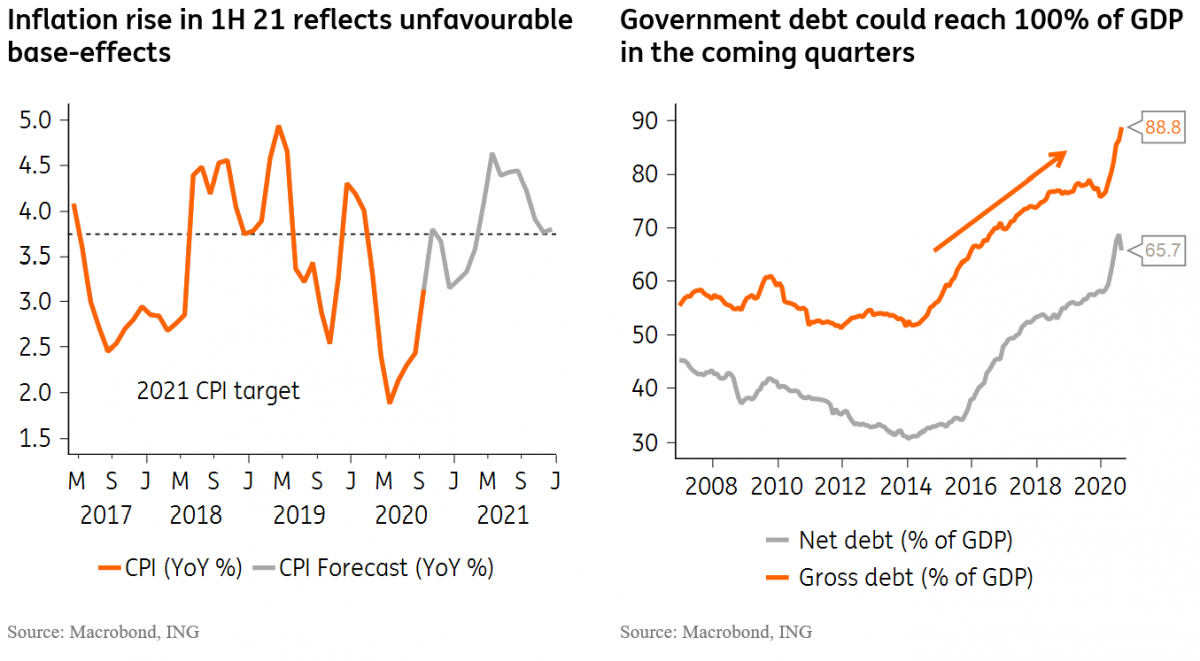

This reflects the facts that 1) inflation will spend much of 2021 above the target, before ending the year on-target (see chart below), and that 2) fiscal risks are unlikely to disappear, as government debt indicators continue to surge in the coming months (see chart below). Both of these trajectories suggest that investors will continue to question BACEN’s resolve to keep the policy rate steady, as currently signaled.

Overall, we expect fiscal uncertainties to remain elevated in the foreseeable future, helping justify a large risk premium in the longer-end of the local yield curve, and a weak BRL.

We are much less certain about the shelf-life of the inflation risks that have been used to justify the aggressive market shift towards rate hikes, which have affected the shorter-end of the curve. Even though this risk is unlikely to dissipate, we expect BACEN to maintain a broadly benign inflation outlook, with the policy statement likely surprising some investors as dovish.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article