Brazil: Fiscal and inflation risks escalate

Stronger-than-expected activity indicators and the growing investor focus on inflation and fiscal risks are among the factors that have helped consolidate the view that, even though Brazil’s central bank did not close the door to additional rate cuts, the policy rate should remain stable at 2% in the foreseeable future

Brazil’s faster-than-expected post-lockdown recovery stands out in LATAM

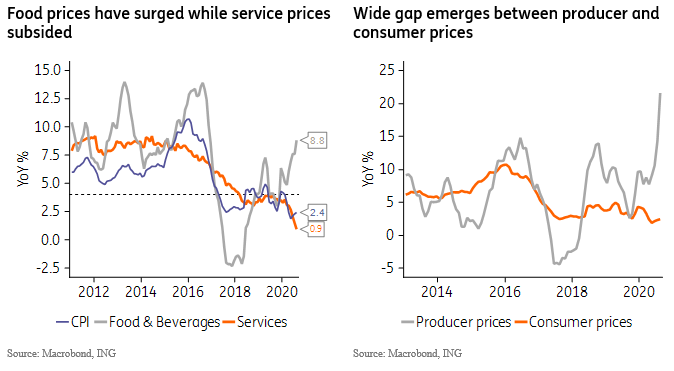

Among the most notable developments over the past month in Brazil we include the strong evidence of a faster-than-expected post-pandemic economic recovery and, on the inflation front, concerns regarding the widening gap between producer and consumer prices and, especially, the fast rise in food prices.

2Q GDP data, and preliminary data for 3Q such as the July/August results for retail sales, construction, industrial production and workplace mobility data, point to a very sharp expansion in 3Q that could nearly offset the 2Q drop.

Congress also enacted a partial extension of the household income-transfer program until December, while Covid-19 remains an impediment for full normalization. This should also contribute to support consumer demand beyond 3Q, and point to a relatively shallower recession in 2020, along with a strongly positive carryover effect into 2021.

As seen in the chart below, retail and industrial activities are on-track to fully recover from the March/April collapse but service activities have lagged and remain about 13% below pre-pandemic levels, while still presenting less certain recovery prospects.

Headwinds abound for 2021, however. A contractionary fiscal policy, still depressed labor markets and the end of the household income transfers suggest that the recovery will depend much more on the effectiveness of monetary stimulus transmission channels, including credit supply/demand conditions, along with investor/consumer confidence.

Despite these uncertainties, we now expect GDP to contract 4.8% in 2020, followed by a 3.9% recovery next year. This compares with consensus estimates of -5.3% and +3.5% respectively.

Inflation pressures rise, but from a very low base

Headline inflation remains low (2.4% year on year), but its composition has exacerbated concerns as food prices have surged (8.8%), adding a negative newsflow/political dimension to the inflation outlook that had been absent until recently.

In our view, inflation risks are narrow-based and do not alter our largely benign outlook for inflation in Brazil. Current price pressures generally reflect supply shocks, strong global demand for foodstuff or FX pass-through that are likely to be temporary in nature.

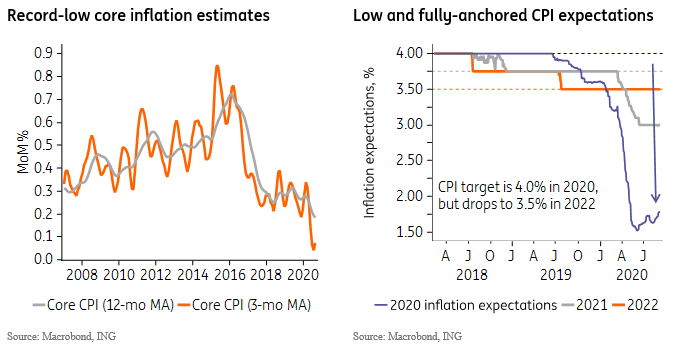

This benign assessment is consistent with estimates for core inflation that continue to trend near record-lows (2.0%) and estimates for service sector inflation (0.9%), which tend to be especially persistent.

Anchored and below-target inflation expectations together with the pronounced price indexation and wide output gap (notably in services) also suggests that, despite current concerns over wholesale and food prices, Brazil’s inflation outlook should remain largely benign in the foreseeable future.

Our forecast is that inflation will end 2020 at 1.9% and 2021 at 2.9%, both in line with consensus estimates.

Monetary policy on hold

At this week’s policy meeting, on Wednesday, we expect the Brazilian central bank to match expectations and keep the policy rate steady at 2.0%. In that case, this would be the first time since mid-2019, when the SELIC rate stood at 6.5%, that a policy meeting ends without authorities lowering the policy rate.

BACEN did not close the door for additional rate cuts but the bank also called into question the existence of much scope to ease further. And, as discussed above, stronger activity indicators and the growing investor focus on the rise of inflation risks should be among the factors that would favor interrupting the easing cycle.

We suspect, however, that the primary reason for interrupting the cycle at this moment should be strategic and prudential factors, which authorities have been hinting at for a while now.

These include concerns about exacerbating financial market instability, notably FX market volatility, which would likely rise even further if the SELIC rate drops below its current level. 2% is already very close to what many consider the technical lower bound for the policy rate in Brazil.

Another important factor that has gained traction lately is the heightened fiscal uncertainties resulting from the sharp deterioration in fiscal accounts expected for 2020. As discussed below, uncertainties about the Congressional commitment to fiscal responsibility is unlikely to abate anytime soon, and this is already weighing heavily on local financial assets.

As a result, we suspect authorities will focus more on “forward guidance”, as evidenced by the debates initiated in the latest policy meeting, possibly as an effort to flatten the shorter-end of the yield curve and deepen the expansionary impact of the current monetary policy stance.

Heightened fiscal uncertainties should linger as Congress considers changes to fiscal framework

Brazil’s economic policy response to the pandemic was unusually aggressive by EM standards. The monetary easing was perhaps the most forceful in EM (considering the current level of the policy rate, i.e. 2%, relative to the 10-year historical average of 10%). The persistent FX sell-off has been the primary side-effect of that easing, which is, arguably, a minor concern in the current low-inflation environment.

Much more consequential has been the fiscal stimulus enacted, especially the household income transfers to help offset wage income lost to Covid-19 movement restrictions.

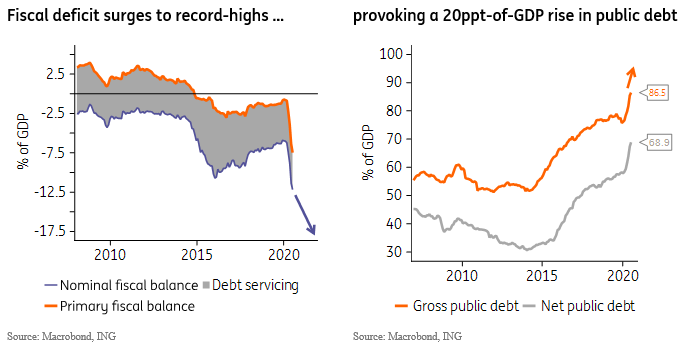

The combined effect of the larger spending and the recession-related drop in tax collection should result in a major fiscal deterioration in 2020. Brazil’s public sector (nominal) deficit should rise towards 18%-of-GDP while (gross) debt-to-GDP is expected to suffer the largest increase across LATAM majors, rising by about 20ppts of GDP, to close to 95%, in 2020.

This sharp deterioration suggests that room for additional fiscal relief is exceedingly narrow. Moreover, additional fiscal stimulus would likely backfire, as it increases fiscal uncertainties, risk premium levels and, eventually, stimulates the dollarization of local portfolios, forcing the central bank to tighten monetary policy too soon, helping offset the fiscal stimulus.

As it stands, the current fiscal framework, centered on the fiscal spending ceiling, would be enough to ensure that the fiscal deterioration is circumscribed to 2020. But there’s intense political pressure to extend the fiscal stimulus into next year.

All eyes on Congress as political brinkmanship intensifies towards year-end

Our base-case scenario is that the existing fiscal framework remains largely unaltered, as advocated by the Finance Ministry, with no changes to the fiscal spending ceiling. But this is a hard call that largely depends on hard-to-predict political negotiations in Congress.

So far, even though Congress has approved some initiatives that worsen next year’s fiscal balance (extending payroll tax exemptions for instance), fiscal responsibility has not been irreversibly compromised. In principle, and judging by the 2021 budget submitted to Congress, there’s still enough leeway to adjust public spending to ensure that long-term fiscal dynamics remain anchored.

But the fact that the flexibilization or even the elimination of the spending ceiling is being considered should be a major source of concern. This suggests that fiscal responsibility should not be taken for granted, and that fiscal risks will remain elevated in Brazil in the foreseeable future.

The approval of legislative initiatives such as a robust “administrative reform”, which would help curb the rise in public sector wages, along with other fiscal initiatives currently under debate in Congress would help reduce concerns over the eventual flexibilization of the fiscal spending ceiling.

But, we suspect, Brazil’s fiscal framework will remain under threat in the coming years, helping to justify a high level of volatility and risk premium for local assets.

On a positive note, fiscal difficulties have also helped spur Congress into action and advance pro-growth initiatives that had been paralyzed until recently. As seen with the approval of the new regulatory framework for natural gas and private sector investment in water/sanitation services, the outlook for crucial infrastructure investment is positive, if fiscal uncertainties abate somewhat.

Sustainable monetary stimulus would also bode well for a continued recovery in domestic demand. But should Congress opt to weaken Brazil’s fiscal stance further, that monetary stimulus is likely to be far too short-lived to sustain the economic recovery in 2021 and beyond.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article