Brazil: A momentous reform

The positive momentum favouring the imminent passage of the Social Security Reform continues, with the goal to conclude the Lower House approval by the weekend. Such an impressive result should trigger a BRL rally, but the rally would be limited by the central bank’s willingness to cut rates, by as much as 150bp, which has reduced the currency's appeal

We are nearly there

After years of negotiations, and much political turmoil, it finally appears that we are days away from the approval of the social security reform by the Brazilian Congress. The pro-reform momentum improved sharply last week, with the approval of the reform by a wide margin in the Lower House’s Special Committee, and with Speaker Rodrigo Maia standing out for his leadership and savvy command of the House.

In fact, congressional leaders aim to fast-track the debate and have the reform fully approved by the Lower House, which requires a 3/5 majority support in two rounds of the vote, by the weekend. Such an impressive result would consolidate Maia’s reputation and would bode well for the ambitious post-reform agenda advocated by the Speaker, which is broadly consistent with the agenda of the Bolsonaro administration, and includes the tax reform and the formal independence of the central bank.

There remains some uncertainty about the timing and the content of the draft that the House should eventually approve. Passage of the proposal already approved by the Special Committee last week would be a favourable outcome.

But the text could be improved with an amendment to, at least, facilitate the extension of the reform to states and municipalities, or it could worsen with, for instance, the easing of the retirement rules for police workers, as advocated by Bolsonaro.

As it stands, the reform could generate savings of about BRL 0.9-1 trillion in 10 years, which is far higher than initial investor expectations and reflects a very mild dilution in the fiscal savings initially proposed by the Bolsonaro administration (BRL 1.1 trillion).

This result would go a long way towards ensuring the long-term sustainability of Brazil’s fiscal accounts and should be enough to prompt a reassessment of the near-term credit ratings trajectory for Brazil. But actual upgrades may take a while longer and should depend, in our view, on the evidence of a stronger recovery in economic activity, which is expected to pick up pace in the second half of the year.

Reform approval would green-light the monetary easing process

The approval of the reform should have an invigorating impact on the outlook for economic activity, but the reform should also have a benign impact on the inflation outlook. As a result, the reform’s approval should not prevent the central bank from adding to the monetary stimulus that is already in place.

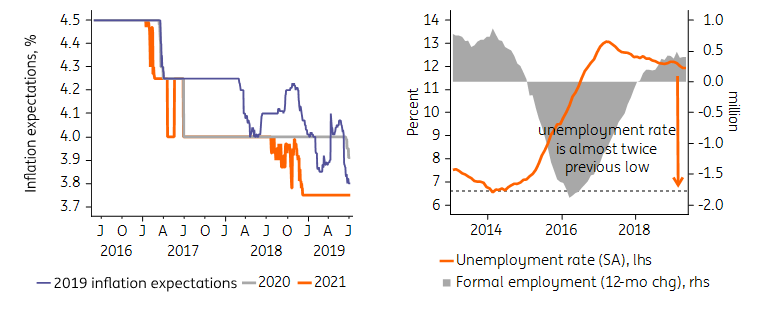

In fact, given the (1) ongoing improvement in current inflation trends, as illustrated by falling and fully-anchored inflation expectations, (2) the expected post-reform appreciating bias for the BRL and (3) the dovish shift seen in central banks across the world, we believe the balance of risks favours a larger, more frontloaded and more lasting cycle than currently priced in the local curve.

The balance of risks favours a larger, more frontloaded and more lasting rate-cutting cycle than currently priced in the local curve

Central bank officials have been on the defensive in their effort to justify their reluctance to ease monetary policy, despite the poor economic activity data and high unemployment. Inaction was generally justified by the lingering uncertainties regarding the passage of the social security reform. But with the reform approved and the yearly rate trending considerably below-target, at around 3-3.5% throughout 2H19, the central bank’s ability to justify inaction should weaken materially.

Fully anchored inflation expectations and ample spare capacity

The BRL could lag other local assets

With the reform approved, political uncertainties related to the sustainability of fiscal accounts should ease materially and prompt an improvement in the outlook for economic activity and for local assets in general.

The Brazilian Real should also rally, but the extent of that rally should be limited by the central bank’s willingness to cut rates (by as much as 150bp), which should reduce the currency’s appeal. Lower rates should also incentivize the use of the USDBRL as a (relatively cheap) hedge to external risks, such as trade wars, as other local assets such as equities and rates are seen as more appealing.

In addition, as indicated by central bank officials recently, the lower cost of financing in BRLs has also reduced the inflow of USDs in Brazil this year. And this shift could intensify post-reform, as the SELIC policy rate is further reduced and the local debt capital markets deepen further. As a result, we now believe that the post-reform trajectory for the USDBRL may bottom at a higher level, closer to 3.6 than 3.4.

The USDBRL may bottom at a higher level, closer to 3.6 than 3.4

In any case, with the reform approved this week or next, we would expect the Brazilian central bank to be able to launch the easing cycle in its 31 July meeting, possibly with a 50bp cut. This would bring the SELIC rate to a fresh record-low of 6.0%, from 6.5% now. Consecutive 50bp cuts would bring the SELIC rate to 5.0% by the end of October, but a shallower or less-frontloaded cycle should not be ruled out.

Consecutive 50bp cuts would bring the SELIC rate to 5.0% by the end of October, from 6.5% now

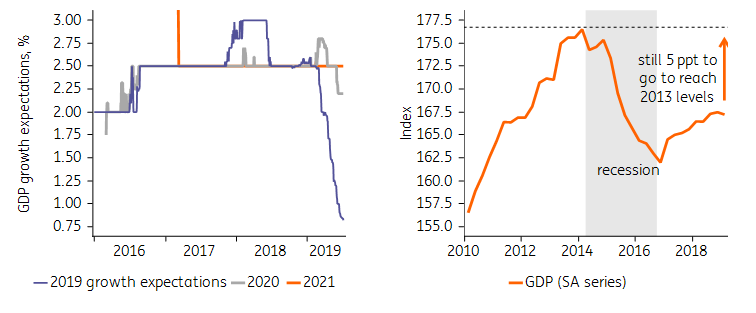

A more frontloaded cycle would be amply justified as a catch-up measure needed to help address the paralysis in economic activity seen in recent quarters. The central bank’s own projection for 2019 GDP growth collapsed recently, moving from 2.0% as of the end of 1Q19 to just 0.8% as of the end of 2Q. And, as the chart below illustrates, Brazil’s GDP remains 5.5ppts below the peak seen in 2013.

Disappointing economic activity and a long way to go to full recovery

Download

Download article

9 July 2019

In case you missed it: Powell to the rescue This bundle contains 12 Articles"THINK Outside" is a collection of specially commissioned content from third-party sources, such as economic think-tanks and academic institutions, that ING deems reliable and from non-research departments within ING. ING Bank N.V. ("ING") uses these sources to expand the range of opinions you can find on the THINK website. Some of these sources are not the property of or managed by ING, and therefore ING cannot always guarantee the correctness, completeness, actuality and quality of such sources, nor the availability at any given time of the data and information provided, and ING cannot accept any liability in this respect, insofar as this is permissible pursuant to the applicable laws and regulations.

This publication does not necessarily reflect the ING house view. This publication has been prepared solely for information purposes without regard to any particular user's investment objectives, financial situation, or means. The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete. ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated, any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this publication comes should inform themselves about, and observe, such restrictions.

Copyright and database rights protection exists in this report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register no. 33031431 Amsterdam).