Brazil: A deeper monetary stimulus

Lackluster growth and low inflation should allow the central bank to lower the policy rate to 5.0% next week and to keep the door open for additional rate cuts that could bring the SELIC rate to 4.0% by 1Q 2020. The deeper monetary easing adds a weakening bias for the Brazilian Real but other BRL-supportive factors imply a more balanced currency outlook

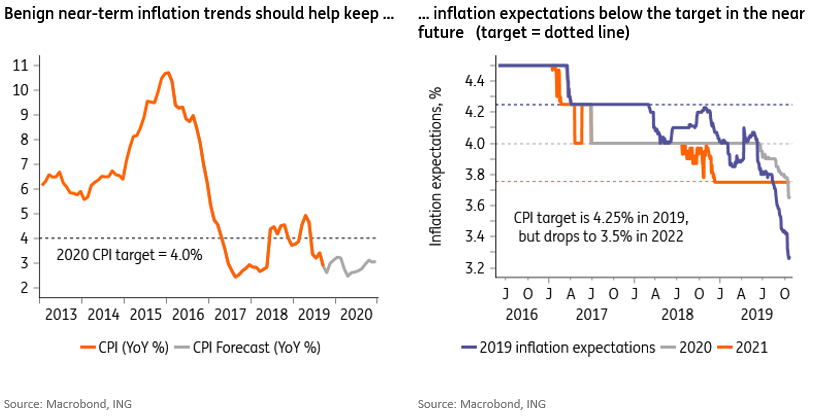

Inflation to trend close to 3% in the foreseeable future

The latest inflation prints have continued to surprise to the downside, and now suggest a forward trajectory that is close to 3% until the end of 2020, ie, far lower than the target, as seen in the chart below.

Low inflation has, meanwhile, helped bring inflation expectations down further and, as seen in the chart below, they now suggest that inflation will continue to undershoot the target until 2021, when the target drops to 3.75%.

Overall, we can conclude that the data released in recent weeks supports an assessment that the inflation outlook has improved since the last policy meeting. And this should be sufficient to push central bank officials to match calls for a third 50 basis point rate cut next week, bringing the SELIC policy rate to 5.0%, another record-low.

Improved prospects for a 4% SELIC rate

Importantly, this broad-based improvement in the inflation outlook took place in the context of shifting market expectations in favor of a deeper monetary easing cycle than previously expected. And this shift, ie, the fact that the local yield curve is now pricing a terminal rate for the current cycle of less than 4.5%, versus 5.0% on the eve of the last meeting, should also help tip the balance in favor of a post-meeting policy-guidance that keeps the door open to additional cuts, beyond this meeting.

Once again, bank officials should explicitly indicate that they are not pre-committing to additional cuts, but they should maintain the current guidance indicating that “the consolidation of a benign outlook for inflation should allow for additional monetary policy stimulus”.

FX considerations should help solidify this dovish shift. In particular, we suspect that the risk of a destabilizing sell-off in the BRL has been reduced. And, if we are right about this, the risk of the USDBRL breaking above 4.20 has been reduced considerably, improving prospects for a deeper monetary easing cycle, with the SELIC rate dropping to 4.0% by 1Q 2020.

FX risks have become more balanced

This more balanced view regarding BRL risks reflects both external and domestic factors.

Abroad, prospects for a deeper-than-expected monetary easing by the US Fed along with the de-escalation of the US/China trade-war rhetoric and the reduction of the risk of a no-deal Brexit should all help extend the relative weakness in the USD seen in recent weeks, and that would help support the BRL’s performance.

Additional domestic developments also suggest a more BRL-supportive environment toward year-end. These include the final approval of the social security reform that took place in the Senate this week, and favorable prospects for large FX inflows in the coming months as a result of the oil auctions scheduled for early in November.

Those auctions, one for a transfer of drilling rights of already-discovered oil and another for the 6th round of oil exploration rights for the pre-salt area, could result in a considerable surge in FX inflows, which could total more than US$20bn, in the coming months.

The actual level of oil-related FX inflows remains uncertain however, as it should depend, among other things, on 1) the auction results, 2) the definition of the compensation the auction winners will pay Petrobras for the investment already done in the rights-transfer area, and 3) Petrobras’s debt-management decisions, which should result in a substantial deleveraging of the company’s external debt profile.

Despite these BRL-supportive developments, additional interest rate cuts and the negative yearend seasonality typically seen for the BRL should continue to incentivize FX outflows, and prevent significant currency appreciation.

These outflows reflect debt-management operations by local corporates that are taking advantage of newly-available cheap local funding to pay down FX-denominated debt. By their nature, these developments are long-term positive for the BRL, as they reduce the stock of FX liabilities by locals, but they are BRL-negative in the short-term, when the outflows take place.

Overall, our view is that the 4.0-4.20 range will continue to be a strong reference range for the USDBRL. We still consider these levels to be higher than equilibrium for the pair, but the consolidation of a sub-4.0 level for the currency may take a while to materialize. In our view, that would depend chiefly on a faster recovery of economic activity, which remains a pre-condition for Brazil to firmly re-anchor its fiscal accounts, improve its credit rating and, as a result, solidify prospects for FX inflows.

A “healthier” but also a slower recovery

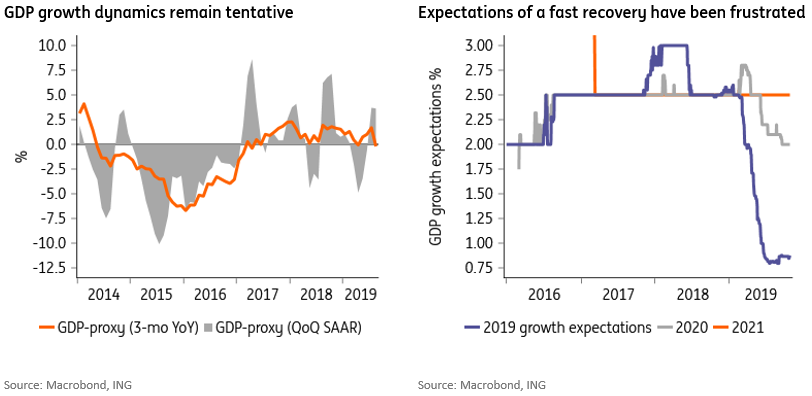

Economic activity data remains generally lackluster and even though investor expectations for GDP growth have stabilized, the expected acceleration in economic activity remains unremarkable.

Recent activity data suggests that fears of a recession have been overstated and that GDP likely expanded in 3Q, which should support our expected 0.9% GDP growth estimate for 2019. But, overall, activity prints remain mixed, and downside risks persist, especially considering the potential for a synchronized global deceleration.

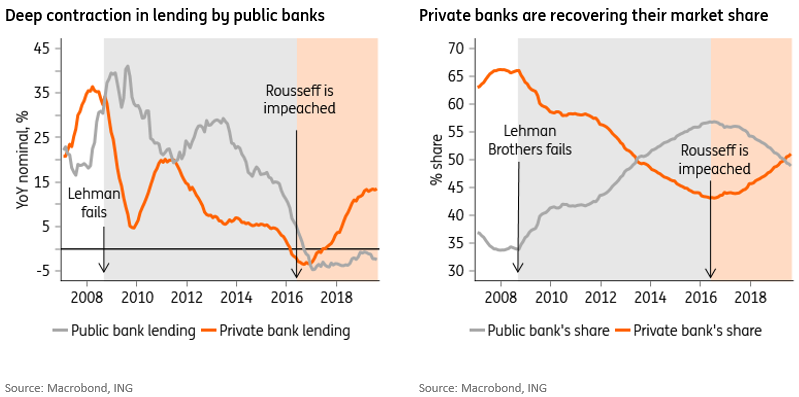

On the domestic front, the persistent fiscal contraction has, to a large extent, helped justify the monetary policy stimulus, without hurting market credibility in the inflation-targeting regime. But the sharp retrenchment of the state presence in the economy, especially evident in the sharp drop in lending by state banks (see chart below), has become a considerable drag on near-term growth, and that drag has yet to be fully offset by the private sector.

Economy Minister Paulo Guedes celebrated this week the fact that the share of private sector lending is once again larger than the share of public sector lending (as seen in the chart above), highlighting the deep policy reversal that is taking in Brazil since Dilma Rousseff left office.

The minister also stated that he is not in a rush to grow and that it’s better to grow in a “healthy” way, without deploying fiscal “short-cuts”. The reason why Brazil can’t deploy those “short-cuts” right now goes beyond the minister’s policy preferences, however, and reflect the deep fiscal constraints resulting from years of fiscal profligacy.

The reality is that fiscal stimulus would probably be the most effective tool to kick-start the recovery, but fiscal constraints impede the administration from conducting any type of counter-cyclical fiscal policy.

In any case, despite the glass-half-full assessment by Minister Guedes, a certain degree of anxiety and frustration still marks the local market assessment of Brazil’s growth dynamics in recent quarters.

The ongoing recovery in (private) bank lending and, especially, the strong upside represented by other funding alternatives in both the fixed income and equity spaces, stimulated by the sharp drop in yields in local Treasury assets, suggest a strong foundation for a surge in (cheaper) funding.

But, up until now, investor reaction has been marked by caution. Perhaps the final passage of the social security reform, successful oil auctions in two weeks and the expected yearend boost in consumption from the approved withdraw of funds from workers’ unemployment savings accounts (FGTS), should help initiate a period of self-sustained faster recovery. But our level of conviction remains low at this stage.

And should activity and labour market trends disappoint for too long, the risk is that the government, or Congress, loses confidence in the pro-market agenda advocated by Minister Guedes, and start experimenting with fiscal stimulus.

Argentina stands as an important cautionary tale for local businesses, as it highlights the risk of a return of a leftist administration should pro-market reforms fail. We don’t think the comparison is pertinent in this case, but the fact that it has taken hold is testament to the depth of the prevailing scepticism, and suggests that business sentiment could take longer to recover, delaying an investment-led recovery.

Overall, even though we remain optimistic about Brazil’s longer term trajectory, the risk is that the strong headwinds represented by the global slowdown and the administration’s inability to execute a fiscal stimulus package result in a recovery that is maybe “healthier”, but it should also be slower than past recovery episodes, with its pace heavily dependent on the private sector’s “animal spirits”.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article