Bank of Canada cuts for a third time with rates heading towards 3%

The BoC cut rates for a third consecutive meeting, citing easing inflation pressures, rising unemployment and a cooling economy. Further cuts are coming and we are targeting 3% rates for next summer. Our near-term target for USD/CAD is 1.35-1.36

BoC cuts rates again

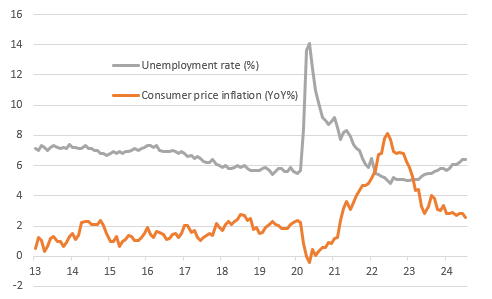

As widely expected the Bank of Canada cut the overnight rate for the third consecutive meeting, leaving the policy interest rates at 4.25%. Unemployment is rising and is likely to hit 6.5% on Friday, up from 4.8% in July 2022 while inflation continues to moderate and at 2.5% is within the BoC’s 1-3% target range. At the same time, economic activity remains lacklustre with the economy expected to grow just 1% this year. These factors were all acknowledged in the BoC’s statement whereby “excess supply in the economy continues to put downward pressure on inflation”.

In terms of the guidance provided by Governor Tiff Macklem, he suggests “if inflation continues to ease broadly in line with our July forecast, it is reasonable to expect further cuts in our policy rate”. He argues that the rise in the unemployment rate is caused by supply of new entrants to the jobs market exceeded demand, but this is helping to depress wage growth, which will keep inflation moderating.

Given this weak growth, rising unemployment, slowing inflation story, the BoC seems set to continue cutting policy to a more neutral level. We essentially see the BoC cutting rates 25bp at each meeting until next summer, by which time the policy rate is expected to be down at 3%.

Canada unemployment & inflation

FX: Fed more important than BoC for USD/CAD

The loonie traded moderately stronger after the BoC rate cut, possibly as some markets didn’t see any hint to faster easing and are therefore pricing out risks of 50bp moves before year-end. Equally, there are few reasons to doubt the BoC will continue easing in October and December, and there is limited upside potential for a hawkish repricing in the CAD curve at this stage.

Ultimately, the Fed’s meeting later this month and – before that – US and Canadian jobs figures on Friday will have a bigger say in USD/CAD short term direction. Our near-term target remains 1.35-1.36 for the pair, but we are retaining a gently downward sloping profile in the longer run as the Fed cutting cycle progresses. CAD remains a lower risk/lower reward currency compared to its peers AUD and NZD, being more shielded from Fed hawkish repricing and/or a Trump victory in November.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article