Better late than never, the Bank of England rides to the gilt market’s rescue

In a dramatic policy U-turn, the Bank of England is resuming gilt purchases. This provides a potential exit door to the nascent UK financial crisis, though this may require the Bank to go even further. Nevertheless, an inter-meeting rate hike remains unlikely despite ongoing concerns about sterling weakness

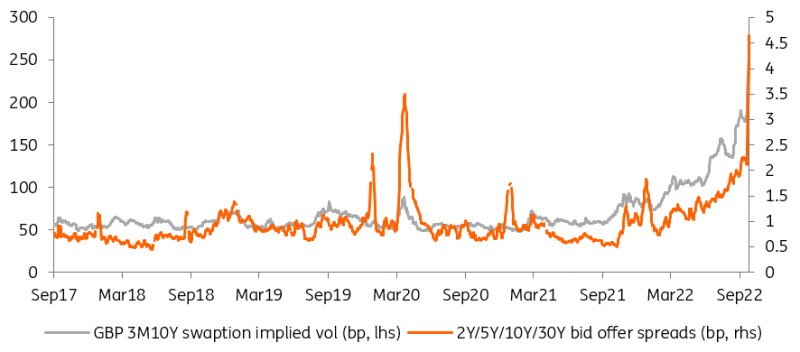

Much needed relief for the gilt market

Better late than never. The Bank of England (BoE) has acknowledged the distressed trading conditions in the gilt market and announced it will carry out gilt purchases over the next two weeks, starting today. If this sounds like a U-turn, that's because it is. As we have repeated ad nauseum in recent weeks, the BoE’s quantitative tightening (QT – reducing the size of its bond portfolio and so requiring private investors to stump up even more cash to buy gilts) is adding to the stress in sterling markets. The BoE’s announcement is only a temporary delay of QT, however, and gilt sales are planned to start on 31 October.

The BoE has acknowledged the distressed trading conditions in the gilt market

In our view, this is unlikely. There is clearly a financial stability aspect to the BoE’s decision, but also a funding one. The BoE likely won’t say it explicitly but the mini-budget has added £62bn of gilt issuance this fiscal year, and the BoE increasing its stock of gilts goes a long way towards easing the gilt markets’ funding angst. Once QT restarts, these fears will resurface. It would arguably be much better if the BoE committed to purchasing bonds for a longer period than the two weeks announced, and to suspend QT for even longer.

Distressed gilt trading conditions pushed the BoE into action

Too timid action but this is a start

Of course, a lot of questions remain unanswered. First, will markets see this as a contradiction to the BoE’s inflation-fighting objective? We don’t think so (see next section). If anything, by preventing a market meltdown, the purchases allow the BoE to keep increasing interest rates without adding fuel to the fire. The second worry is fiscal dominance, where monetary policy is effectively dictated by the Treasury. This is clearly a worry and the Treasury issued a statement saying that it remains committed to the BoE’s independence. This second point is only a concern in case of effective debt monetisation, from which today’s actions are a far cry.

We think purchases should and will last longer than the initial two weeks

So what’s next for gilt markets? They anxiously await more detail on the size of the BoE’s intervention. We think purchases should and will last longer than the initial two weeks. This would restore market confidence, and provide cover for investors to return to the market, sowing the seeds for the end of this crisis.

Nevertheless, a lot still hinges on the Treasury and investors will be looking for a credible plan to get debt under control. Today's decision from the BoE only buys time.

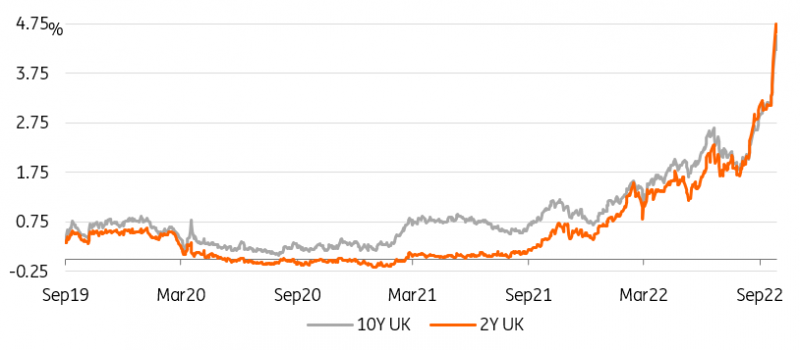

Gilt yields are still well above 4%, more purchases might be needed

Inter-meeting rate hikes still unlikely

Markets are now pricing a terminal rate above 6% next year, and while we can debate whether this is a reliable gauge of expectations with this level of market stress, it’s no doubt true that investors are positioning for a sizable reaction. That leaves the Bank facing an unpalatable decision. If it meets expectations for big rate hikes, it risks prompting serious damage to the housing market. If nothing else, a sharp rise in mortgage rates will prompt homeowners to cut spending elsewhere, increasing the risk of a wider economic downturn this winter. Similar pressure could emerge in the corporate borrowing space too.

If the Bank doesn’t meet expectations, it risks further pressure on the pound, adding to the risk that core inflation stays above the target in the medium-term. The Bank is already worried, given the government’s fiscal plans and the tightness in the jobs market.

It’s an unenviable position, but the second option seems more palatable. Not least because hiking aggressively to protect the pound has no guarantee of success. The fact that the Bank hiked by ‘only’ 50 basis points last week gives us a clue that policymakers are more inclined to think this way too.

Nevertheless, the existing pressure on sterling means the Bank has little choice now but to hike more aggressively in November – a 75bp or perhaps even 100bp move seems likely. But we still feel the kinds of rate hikes being priced into financial markets over the coming months look overdone. We still suspect the bar to an inter-meeting hike is also set fairly high, and that also seemed to be the message from both official Bank of England statements and chief economist Huw Pill’s comments yesterday.

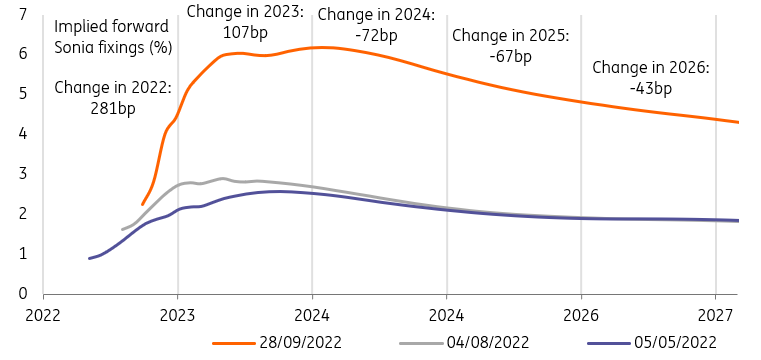

Sonia swaps still imply a sizeable amount of hikes by the BoE

GBP: Mixed news for the pound

BoE gilt intervention is being seen as mixed news for sterling. The positive is that the BoE has taken action to address financial stability concerns at the long end of the gilt market. Given that the sell-off in gilts since early August had been a big factor driving sterling weakness, today’s intervention will be welcomed by some.

Die-hard sterling bears will remain so, citing ‘fiscal dominance’ in that the BoE has suspended its planned QT, and by buying gilts the BoE effectively provides room for the government to continue with its aggressive fiscal programme. That is why we have seen HM Treasury make every effort to reassure BoE independence.

Overall, we would favour a little more sterling stability on today’s bond market intervention. But market conditions remain febrile (one week traded volatility still at 23%). Both the strong dollar and doubts about UK debt sustainability will mean that GBP/USD will struggle to hold rallies to the 1.08/1.09 area.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article