Bankruptcies: Another source of eurozone divergence

The petering out of the support measures taken during the Covid crisis is likely to lead to an increase in bankruptcies across eurozone countries. But to what extent? Our analysis shows they'll be another source of divergence across the monetary union

Collateral damage

The economic shock of a "classic" recession will, with some delay, also increase the number of bankruptcies, job losses and therefore unemployment. Having said that, a consensus was established at the very beginning of this crisis to cushion the shock in an unprecedented way through multiple support measures. Now that economies are reopening and the economic recovery is taking shape, the question is how bankruptcies will evolve once support measures are withdrawn.

Looking at past experience and the relationship between the economic cycle and bankruptcies, we have some idea about the worst-case scenario. In this case, a tsunami of bankruptcies and job losses could unfold once the support measures and bankruptcy moratoriums are stopped. Although such a scenario is not the one favoured by the European Central Bank, officials have recently warned that banks could face significant losses from a sharp increase in the number of bankruptcies.

The most optimistic scenario would be that the economic recovery (which would coincide with the end of the support measures) would be so strong as to give companies and their investors enough of a positive outlook that the bankruptcies avoided during the worst of the crisis never materialise.

As is often the case, the reality is probably somewhere between these two extreme scenarios. However, this reality could be very different from country to country and within each country from sector to sector. The case study of The Netherlands leads to the conclusion that the number of bankruptcies expected as a result of the Covid crisis should remain limited and lower than what was experienced during and after the global financial crisis.

Can this conclusion be extrapolated to all eurozone countries? Probably not for all member states. In this article, we try to identify the countries most vulnerable to a strong increase in bankruptcies.

This time, it’s different

The widespread lockdown in the second quarter of 2020 brought a significant part of the economy to a halt. The fall in activity was unprecedented. As a result, the gap between the peak of the economic cycle and the trough of activity was much larger than in previous crises. During the financial crisis, this gap for the eurozone as a whole was 5% of GDP compared to almost 15% (Chart 2) during the pandemic. The depth of the crisis would therefore suggest that the economic consequences of the shock, particularly in terms of business failures, would be greater than during the financial crisis.

That said, while economies contracted very quickly, they have also rebounded relatively quickly. The current situation has therefore improved significantly compared to the low point in the second quarter of 2020. In the eurozone, the loss of activity from the peak of the cycle is now approaching 5%, which is precisely the size of the shock of the financial crisis. Better still, the next few quarters should see a more vigorous recovery as economies reopen. With a reopening widely anticipated, the level of economic sentiment has already exceeded its long-term average (100) barely 14 months after the initial shock. During the financial crisis, it took almost twice as long for confidence to return (Chart 1). The Covid crisis was therefore very deep, but based on current knowledge, it is not likely to be extremely long. According to our own forecasts, the eurozone economy will have returned to its pre-crisis level in 1Q 2022, seven quarters after the trough of the crisis and 17 quarters earlier than after the financial crisis (marked by a double dip…). Therefore, even if the Covid crisis was deep, this argues for a limited effect on the number of bankruptcies. While the number of bankruptcies increased by 35% after the financial crisis in many developed countries, the dynamics of the current crisis argue for a smaller effect.

Within the eurozone, there are significant differences between countries. The Netherlands, Finland and Ireland are already close to their pre-crisis level and at this stage of the cycle (i.e. five quarters after the peak of the cycle), the loss of activity is less than that incurred during the same period in the financial crisis.

In contrast, the situation appears to be particularly difficult in Spain, Portugal and Greece, where the loss of activity in relation to the peak of the cycle is still around 9%. More importantly, this shortfall in activity is almost double that experienced over the same period during the financial crisis. It is difficult to imagine that, all other things equal, bankruptcies would not be more numerous in these countries.

Confidence in the eurozone (ESI) has recovered much faster than after the financial crisis

Top of cycle (month #1) is March 2008 in the case of the GFC and February 2020 in the case of the Covid crisis

The 2Q 2020 lockdown had induced an exceptional contraction of GDP

Peak-to-trough loss of activity, in % of pre-crisis GDP level

Government encountered the biggest loss of income during the crisis

Loss of Gross Disposable Income during the first four quarters of the crisis (in % of previous year GDP)

Government intervention

As said before, massive intervention of governments to compensate for the effects of the loss of activity linked to containment measures is likely to limit the future number of bankruptcies. To obtain a consistent comparison across countries, this argument can be captured by using sector accounts and measuring the loss of disposable income for the three main sectors of the economy (households, business and government)[1].

At the level of the eurozone as a whole, Chart 3 is unequivocal: while the loss of disposable income for businesses is, as a percentage of GDP, broadly the same in the financial crisis and the Covid crisis (which will be decisive in terms of bankruptcies), it is indeed the general government that has suffered the greatest loss of income, which is both an illustration of lower tax revenues, but also transfers to other sectors of the economy as part of the support measures.

There is, in fact, a double argument here. By supporting household income in a context where it was not possible to consume, governments have increased the capacity of households to consume when economies reopen, which should boost the economic recovery and support the sectors most affected by the confinement measures, and therefore most at risk of bankruptcy. And by supporting corporate income, this is likely to have had a direct impact on the financial health of companies and also argues for a limited impact on bankruptcies, or at most similar to what was observed during the financial crisis.

In all countries in our sample, the government bore the largest share of the overall loss of disposable income. That said, the measures taken have not been able to compensate for all the effects of the crisis everywhere. We observe a loss of household income in 2020 in Greece (very limited), Spain, Italy and Austria. In these countries, a consumption-led recovery could be weakened and thus increase the bankruptcy rate in sectors related to household consumption, despite the economic reopening. The loss of corporate disposable income appears to be particularly significant (more than two GDP points) in Spain, Greece and France, which means that companies have suffered more in these three countries, increasing the risk of bankruptcies.

How could those countries encounter such a loss in corporate disposable income? The loss of operating surplus (the money a company earns from its core activity) was indeed the greatest in these countries (Chart 5), but once the effect of net capital income and transfers paid and received (including aid received in the context of the crisis) is added, the loss of disposable income remains significant. The cases of Portugal and Belgium are interesting in this respect: the loss of operating surplus also exceeds two percentage points of GDP, but once the corrections are applied, the drop in disposable income is much smaller. It seems that in these cases, the measures taken by the governments have made it possible to better absorb the shock.

Considering the cumulative effect of household and corporate income losses on the risk of bankruptcy, Spain, Greece and Italy appear to be the most fragile economies, while the Netherlands, Finland, Ireland and to a lesser extent Austria are apparently in a more comfortable situation.

[1] The disposable income of a sector is composed of its so-called primary income (activity and net capital income) and secondary income. The latter is the difference between transfers received (social benefits, subsidies, etc.) and transfers paid (taxes, social contributions, etc.).

Divergent impact on households and corporates across eurozone countries

Evolution of 2020 Gross Disposable Income[1] compared to 2019, in % of 2019 GDP

[1] GDI of households is the sum of compensation of employees, mixed income (self-employed), net capital income and net transfers. GDP of corporates equal the sum of operating surplus, mixed income, net capital income and net transfers.

The loss of operating surplus could not be compensated for by other net income

2020 loss of corporates operating surplus and gross disposable income, in % of 2019 GDP

Conclusion

In the eurozone, if we disregard the huge shock of the lockdown on economies in the second quarter of 2020, the economic crisis generated by the pandemic is not much deeper than the financial crisis of 2008-2009. The Covid crisis also appears shorter than the GFC, meaning that for some countries, it is even cumulatively less deep than the financial crisis. Economies are also benefiting from stronger-than-usual recovery prospects thanks to the forthcoming reopening of all activities as well as the major stimulus plans put in place.

So what should we expect? First of all, it should be remembered that the measures taken during the crisis artificially reduced the number of bankruptcies by 25% in the euro area. However, once the support measures come to an end, it is very likely that we will see a rapid return to the trend observed in 2019, which will result in a sharp increase in the number of bankruptcies. Moreover, we expect the number of bankruptcies to exceed the past trend by 10% to 20%, particularly in view of the loss of income that it has caused for businesses. Structural changes driven or accelerated by the crisis are also likely to insert more upward pressure on bankruptcies. Nevertheless, this increase in bankruptcies would still be lower than what was observed in most developed economies after the financial crisis.

That said, the situation in the euro area masks significant differences between countries, due to the shock suffered and the capacity of the aid granted to compensate for it. Spain, Greece and Italy are the most at risk.

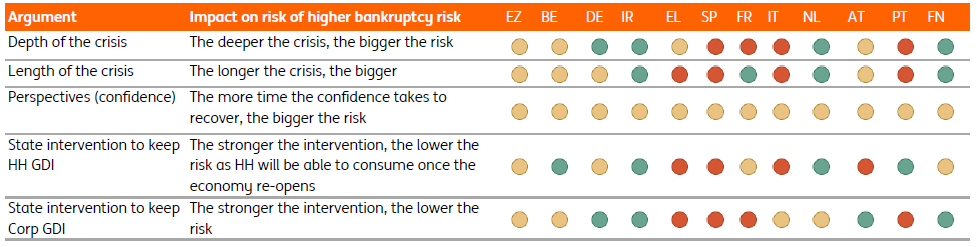

Summary of national strengths and weaknesses

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

10 June 2021

ING Monthly Update: Looking for freedom This bundle contains 14 Articles