Bank Pulse: A softer performance in subordinated bank bonds on rising inflation expectations

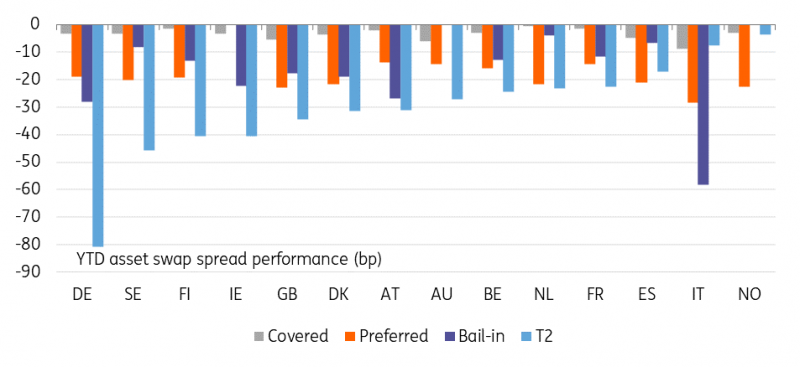

Bank bond spreads show a mixed response to the rising inflation expectations. T2 bonds have recently seen some spread widening, while covered and preferred senior bonds grinded mildly tighter on the rise in underlying yields. Performance prospects will likely remain somewhat softer for junior bank bonds

Persistency of inflation concerns: a crucial driver to performance

With energy prices soaring and headline inflation at the highest level in a decade, the debate on the transitory nature of the rise in Eurozone inflation remains pretty much alive. ECB President Christine Lagarde reiterated this week that the inflation upswing should largely be viewed as temporary, and that support measures should not be withdrawn too early, while ECB member Klaas Knot expressed his concerns that inflation could rise faster than expected. In our view, market concerns for inflation to be more permanent than initially thought and, more importantly, the ECB’s response to that, is probably one of the most crucial drivers to performance into next year for bank bonds.

T2 paper has recently already seen some pressure on spreads

The somewhat mixed performance picture we have seen so far this month across the liability structure, already gives a first taste of what to expect if convincing evidence on the temporary nature of inflation doesn’t present itself. Further down the liability structure, we have seen bank T2 spreads come under a bit of widening pressure in the past two weeks, with bail-in senior following suit in the last few days. Instead, covered bond and preferred senior unsecured spreads have been stable or tightened slightly, with the rise in underlying yield levels freeing up space for tighter bonds to perform.

Secured bank bonds shower better performance resilience

This, in our view, underscores the different performance impacts of increased inflation expectations, the related rise in underlying yield levels and the potential effect these may have on economic growth and monetary policy accommodation. Bank bonds further down the liability structure will continue to see the softest performance if the rise in inflation proves more persistent than initially thought, particularly if it starts impacting economic growth. Safer bank bond products such as covered bonds and preferred senior will show better performance resilience. Market technicalities, such as net supply differences, should in this case only play second fiddle where it comes to performance.

Capital cushions may decline as dividend payments are resumed

Besides, there are broader bank fundamental aspects that plea for a somewhat softer performance of more junior bank bonds going forward. The results published by the ECB yesterday on the macroprudential stress test for European banks for 2021-2023, confirm that even in the baseline scenario the systemwide transitional CET1 ratio will fall from 15.5% in 2020 to its pre-pandemic level of 14.4%, on the back of an expansion of bank assets and resumption of dividend payments by the banks. This implies a somewhat lower capital cushion, particularly for more junior bank bonds.

Subordinated bank bonds have broadly outperformed this year

Performance and supply charts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article